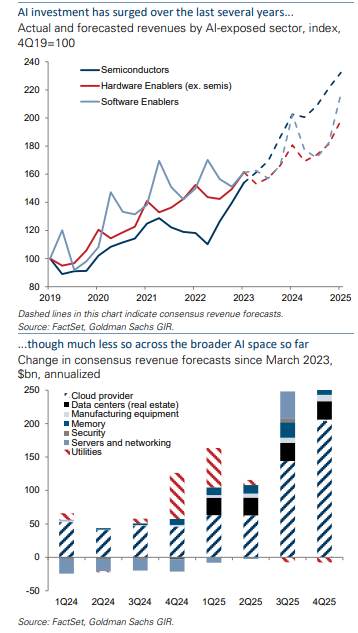

Most of us would likely agree that artificial intelligence benefits are going to take a while to be seen almost anywhere except the financial results of infrastructure providers, who clearly will benefit. Nor would that ever be unusual when an important new technology--not to mention a possible new general-purpose technology--first emerges.

Indeed, analysts at Goldman Sachs say “leading tech giants, other companies, and utilities to spend an estimated $1 trillion on capex in coming years, including significant investments in data centers, chips, other AI infrastructure, and the power grid.”

Still, “this spending has little to show for it so far.” Nor would one realistically expect to see quantifiable results so early. The pattern with general-purpose technologies is that the platforms and infrastructure must be built first, before use cases and apps can be developed.

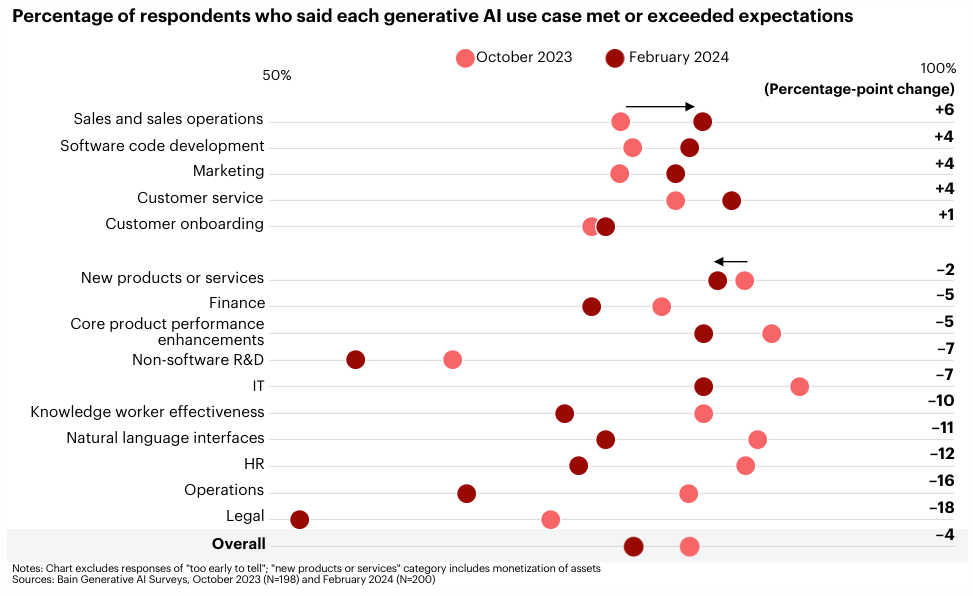

Also, some functions are more susceptible to generative AI impact, for example, than others.

Most of us would be willing to concede that customer service is one area where generative AI, for example, should produce results. Functions with many repeatable elements are commonly thought to be susceptible to AI automation.

In a survey conducted for Bain, enterprise executives reported that better results were seen in sales; software development; marketing; customer service and customer onboarding, for example. Between October 2023 and February 2024, though, most other use cases seemed to produce less favorable outcomes than expected.

Generative AI thrives on well-defined patterns and processes, so jobs involving repetitive tasks with clear rules and minimal ambiguity are likely candidates for early change.

But lots of functions and tasks are not routine or well structured; not simple but complex, so the range of use cases that can benefit near term is arguably limited.

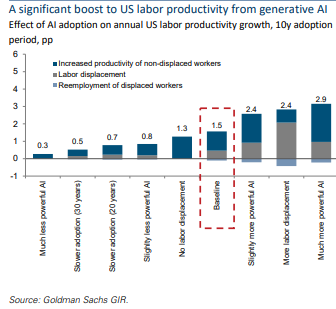

As the report notes, Daron Acemoglu, Institute Professor at MIT, estimates that only a quarter of AI-exposed tasks will be cost-effective to automate within the next 10 years, implying that AI will impact less than five percent of all tasks.

Most of us would be willing to concede that customer service is one area where generative AI, for example, should produce results. Functions with many repeatable elements are commonly thought to be susceptible to AI automation. Generative AI thrives on well-defined patterns and processes. Jobs involving repetitive tasks with clear rules and minimal ambiguity.

All that noted, the first quantifiable results will be seen among suppliers of infrastructure, as apps cannot be built until the infrastructure is in place.

That noted, it also could be said that there has been overinvestment--at some point--in infrastructure for past general-purpose and new technologies. It also might be noted that application and device over-investment also occurs, early in the adoption of a new technology.

But there is a difference between “over-investment” and the proliferation of would-be competitors in a new market. It always is normal to see more startups in any area of new information technology than there are surviving firms once the market is mature.

The difference between over-investment and normal competition in a new market can be subtle. What might not be subtle is the lag time between capex investments and revenue realization, for firms not in the "picks and shovels" part of the ecosystem.

Infra suppliers already have profited.