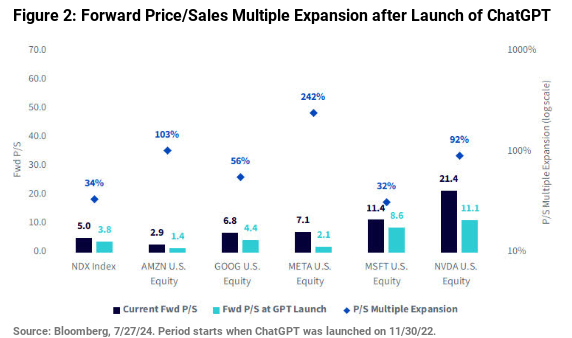

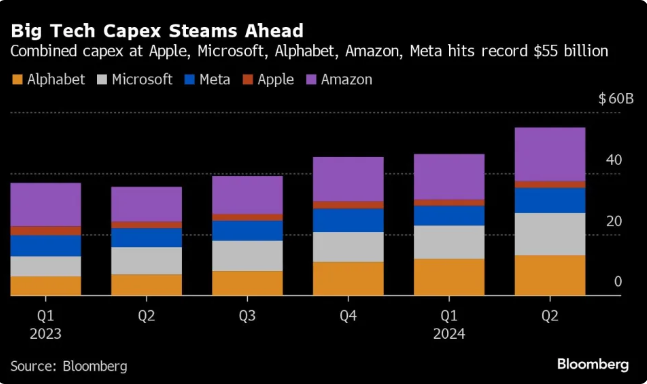

Capital investment at Alphabet, Microsoft, Apple, Amazon and Meta is up, reaching about $55 billion in the second quarter of 2024, with the expansion largely driven by investments in artificial intelligence capabilities.

Some of that investment comes as the firms create their own generative artificial intelligence models and train them; other costs to adapt models to the existing core firm products. So the effort initially involves some mix of creating general-purpose models other enterprises can use and applying GenAI to existing products and processes.

Alphabet and Meta have been most active creating general-purpose models others can use. But all the hyperscalers are adding GenAI to their core revenue-driving products.

For Alphabet that means grafting AI onto search, Pixel phones and the Android operating system. Microsoft initially focused on AI-enabling its productivity suite. Virtually all the firms are creating AI assistants.

Meta is AI-enabling its social media and communication apps. Apple largely is AI-enhancing its iPhone apps and functions, while enhancing Siri.

Amazon is applying GenAI to its shopping experience while hosting a number of leading models on Amazon Web Services.

There already are clear examples of use cases across core shopping, social media, search, recommendations engine and communications and productivity suite use cases. But much more is expected.

Still, it is worth noting that “the things that will drive the most results in 2025 and 2026 are…the ways that AI is shaping the existing products,” said Mark Zuckerberg, Meta CEO. That noted, the Meta chief also said that “we don't expect our Gen AI products to be a meaningful driver of revenue in 2024.”

Much of the value of recommendations across media consumption and shopping for example, hinges on the value (accuracy, relevance) of the recommendations, as well as the ease of interacting with the apps.

“Over time I'd like to see us move towards a single unified recommendation system that powers all of the content including things like people you may know, across all of our surfaces,” said Zuckerberg.

For advertising use cases, AI should automate nearly the entire process. “Over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we're going to go do the rest for them,” said Zuckerberg.

In other cases, where general-purpose models are created, the effort is “enabling lots of people to create their own AIs,” said Zuckerberg.

For the most part, all the AI efforts include creating ways to add AI features and functions to all existing products.