Are there profit margin analogies for generative artificial intelligence as it is applied by software firms? In other words, will generative AI profit margins prove to be equivalent to, or lower than, or higher than, profit margins in other industries that have faced new technology eras?

Generally speaking, media and connectivity firm profit margins have declined in the transition from pre-1990 to post-1990 periods when digital technology replaced analog. The exception, at least so far, is mobile service, which by most measures is more profitable today than in the analog era.

As always, there are multiple possible driving forces, ranging from competition to deregulation to the impact of internet product substitution.

Some might argue that productivity gains--and corresponding impact on profit margins--was at one level for software firms in the mainframe and then personal computing era; perhaps a different level in the cloud computing (software as a service) era and might change again in the AI era of software.

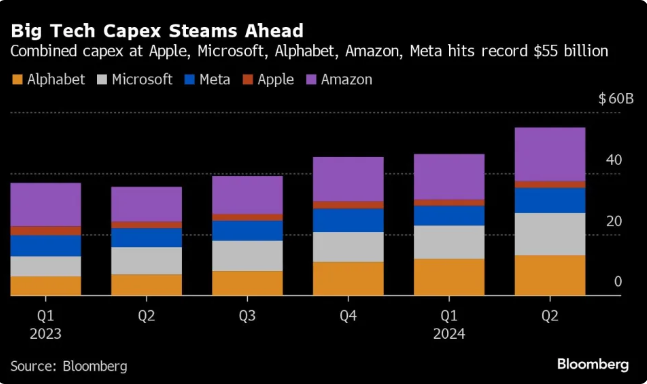

Others are not so sure, but most might agree that hardware margins, which historically have trended downward over time, might continue to see margin erosion over time, particularly as large end users build their own chips for processing acceleration.

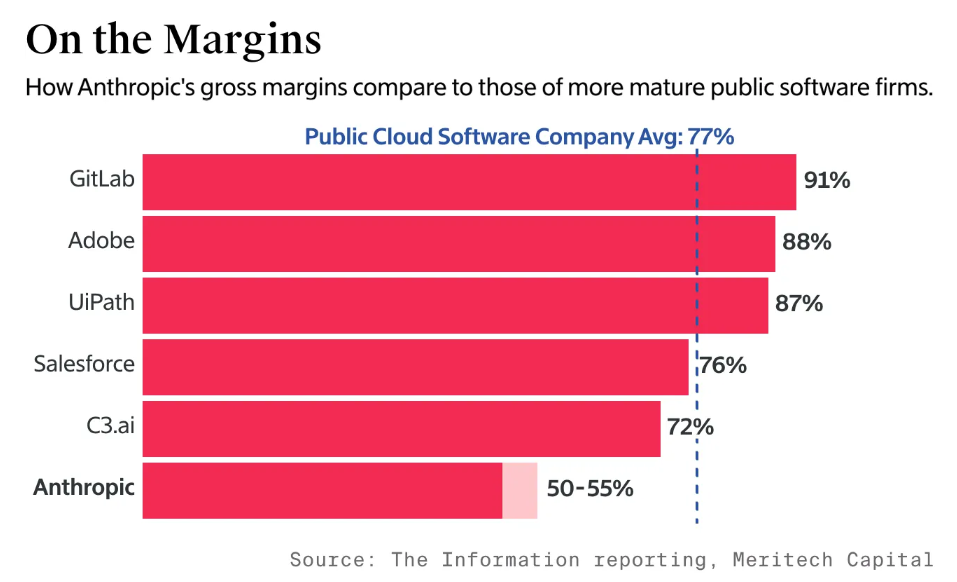

source: MostlyMetrics, The Information, Meritech Capital

But it remains unclear how AI will affect profit margins for software firms, but some would note that margins for both hardware and software have remained relatively unchanged for nearly 40 years.

Right now, the issue might be we have no experience curve for AI operations and value.

Some will argue profit margins for generative AI service providers will fall over time, based largely on large capital investments and scarce evidence yet of robust revenue models. That might be the case, though.

Software margins have been relatively consistent despite the move from mainframe to PC platforms; onboard to cloud processing. We cannot yet say how margins might change with AI, over time.

The issue is whether AI products retain software margin characteristics or eventually resemble margin trends for content, connectivity and computing hardware.

----------------