Cable execs keep stressing they are communications companies--and arguably leading companies--rather than video entertainment distributors. But it might be hard to do that, long term, without a key position in mobility, which drives the bulk of revenue in the U.S. communications business, unless an alternative international growth strategy is the alternative.

The Sky purchase, though increasing Comcast exposure to video distribution, might suggest the early focus.

The issue for Comcast, as for some other firms, is whether a “fixed network only” or “mobile only” strategy is sustainable.

To be sure, cable companies are positioned to take market share in business services and consumer broadband. In fact, the whole growth story for cable companies in communications is “taking market share” from telcos faster than video revenue is lost.

But the bucket is leaking. Cable has to add new revenues simply to replace lost video revenues. Net growth beyond that replacement is the issue.

SNL Kagan forecasts residential cable industry revenues will rise from $108.38 billion in 2016 to $117.7 billion in 2026, a $9.32 billion increase over the 10-year period, even as video revenues shrink.

Commercial services revenues will push total industry revenue from $130.57 billion to $140.99 billion, a $10.42 billion increase, SNL Kagan suggests.

That forecast assumes consumer broadband subscriptions grow by more than eight million over the next 10 years, largely by market share gains at the expense of telcos. That is why fixed wireless and 5G mobile substitution are such a big potential change for telcos. If 5G reduces share losses to cable TV, the consumer revenue growth estimate for cable is too high.

The SNL Kagan forecast also is sensitive to the rate of linear video subscription losses. Basic video subscriptions are projected to drop by an annual compounded growth (CAGR) rate of 1.5 percent to 45.4 million by 2026. Accelerated losses, which most likely expect, will damage the overall growth forecast as well.

SNL Kagan anticipates total revenues generated from residential video services to fall at a CAGR of -0.5 percent over the next 10 years, totalling $55 billion annually in 2026. Again, that could be overly optimistic.

Advertising revenue is expected to grow at a 4.3% CAGR through 2026 to reach $6.3 billion, but is not a big enough contributor to offset bigger losses in the core services areas.

So the strategic issue is whether the cable industry can sustain a position at the top of service provider rankings without serious mobile revenues and profits, even if taking market share in enterprise and business markets will help.

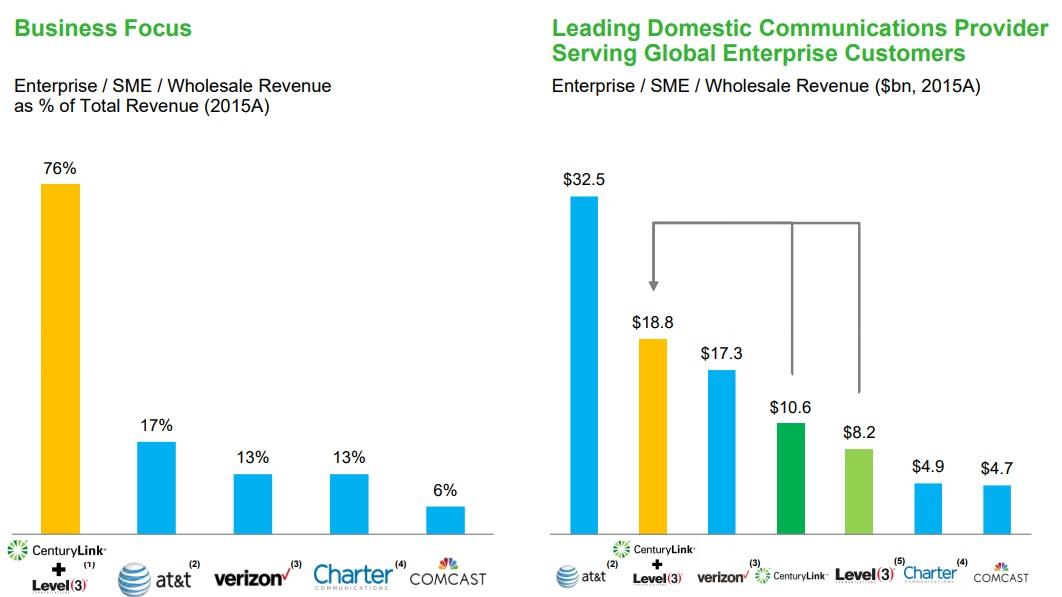

That might be likened to the position CenturyLink finds itself in: it already earns more than 76 percent of total revenues from enterprise customers on its global networks and metro enterprise services.

Its entire national footprint of mass market customers is essentially a drag on company profitability.

Mobile remains the growth engine globally, but the relative scale and importance of the mobile, fixed broadband, and entertainment TV markets varies hugely by country and region. In 2021, the mobile market will generate 87 percent of total connectivity and video revenues in Africa and 70 percent in the Middle East, compared to 50 percent in North America and 49 percent in Western Europe, according to Informa Ovum. The differences stem largely from revenues generated from fixed networks.

Cable dominates consumer broadband, has a strong, if declining video business and is growing its share of commercial revenues. But the other leading incumbents are fighting for their lives as well, and will not easily yield market share in voice and data, least of all AT&T and Verizon, which appear to be holding their own in consumer internet access share, for example, while most of the telco industry losses come from smaller providers relying mostly on digital subscriber line for internet access.

Almost without exception, such providers also have no mobile exposure. How long such firms can compete against cable, which arguably offers better value for consumers, is an open question.

Conversely, cable can compete against weaker telcos without mobile assets quite well. Whether cable can challenge AT&T and Verizon, though, is a bigger question at the moment, so long as no clear mobile strategy at scale.

{kind=link}