Though it might seem counter-intuitive, connectivity service provider revenue might not change all that much because of the Covid-19 pandemic, and a revenue rebound might be quite swift, in some markets.Some product lines and some geographies might not fare that well, but there are historical reasons to believe any dip will be shallow and short lived.

By way of comparison, that is what happened to telecom service provider revenue in the wake of the global Great Recession of 2008.

To be sure, some believe global telecom revenue will fall by 3.4 percent in 2020 compared to 2019, before returning to growth (0.8 percent) in 2021, according to Analysys Mason. Analysys Mason had previously forecast growth of 0.7 percent in 2020 and 0.8 percent in 2021.

International Data Corp., on the other hand, predicts that global telecommunications and subscription TV services revenue will dip less than one percent in 2020. Most observers might agree that a dip of some size will happen. What is likely more contentious is the size of such a dip, or its duration.

With all the talk about a new normal caused by the Covid-19 pandemic, where life in many ways will be permanently altered, it is worth keeping in mind that past traumatic events such as the Great Recession of 2008 can be very hard to detect in time series data where it is possible to track trends over time.

So even if it seems too optimistic, the IDC prediction is well within historical expectations. The Great Recession of 2008 caused a momentary flattening of revenue growth, with the prior pattern asserting itself quickly afterwards. A modest dip would not be without precedent, even if we fear greater damage.

And though it is reasonable to expect a dip in business customer spending (with economies shut down and significant bankruptcies expected), consumer spending on telecom services might well increase, as it did in the United States in the aftermath of the 2008 Great Recession.

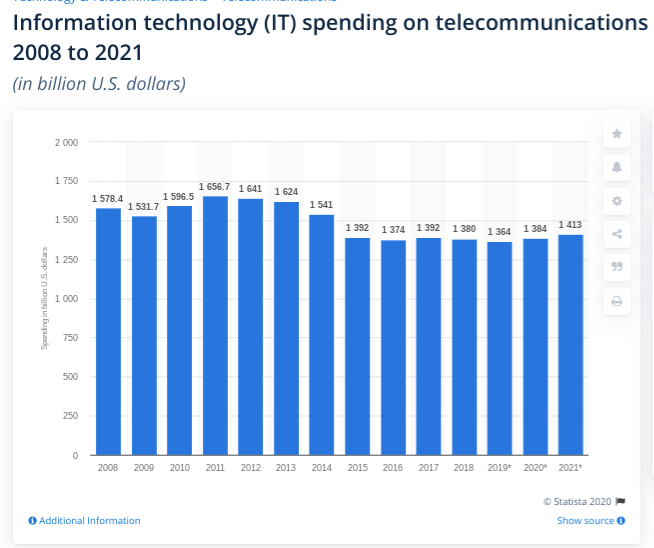

IDC estimates global service provider revenue at nearly $1.6 trillion in 2020, a decrease of 0.8 percent compared to 2019. IDC expects the decline to continue in 2021, but at a somewhat lower degree.

The mobile segment, the largest segment of the market, will post a slight decline in 2020 due to lower revenues from roaming charges, less mobile data overages due to the stay-at-home situation, and slower net additions, especially in the consumer segment, IDC argues.

Fixed data services spending will increase by 2.9 percent in 2020. Spending on fixed voice services will continue to decline.

Subscription video services will be boosted by the lockdown, but also affected by the economic downturn, so the spending in this category is expected to decline slightly, says IDC.

The Americas market will see a tiny decline of 0.04 percent. Europe, the Middle East, and Africa (EMEA) and Asia/Pacific (including Japan) will dip more. Growth is not expected in EMEA or Asia/Pacific before 2022 as the users in emerging markets are expected to remain cautious about spending for some time, IDC estimates.