While consumers are beginning to embrace digital financial management, they remain hesitant to dive in completely, taking a "hybrid" approach.

More consumers receive their statements online than through the mail, but more than 25 percent of consumers "double dip," receiving both paper and electronic statements, Javelin Strategy & Research says.

That sort of behavior is typical when major new technologies start to displace older ways of doing things. When steam engines began to displace sails as the propulsion for ships, ship owners outfitted sailing vessels with boilers, in part because, early on, the economics of steam power were not as good as sails.

Most fixed communication networks use a hybrid of older copper media, with an overlay of optical fiber media, and a mix of digital signaling and IP transmission.

In a similar way, people now use a mix of bank visits, ATM machines, PCs, tablets and smart phones to check balances or conduct transactions. That "hybrid" behavior will continue for some time, as behaviors shift and more users are able to use newer methods for seeking information and conducting transactions.

Some 40 percent of mobile-device owners will tote a tablet by end of 2012. About 72 percent of U.S. adults with mobile devices will tote a smartphone, up from 45 percent in 2011. More than half of mobile-device owners (111 million) will use mobile banking on an annual basis, up from 30 percent in 2011, Javelin predicts.

Sunday, May 27, 2012

"Hybrid" Behavior in Consumer Use of Digital Financial Management

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

PayPal Adds 15 U.S. National Retailers for Retail Payments

PayPal has announced 15 new national retailer partners who are adding PayPal’s offline payment and shopping solutions. The key phrase there is "offline."

These include: Abercrombie & Fitch, Advance Auto Parts, Aéropostale, American Eagle Outfitters, Barnes & Noble, Foot Locker, Guitar Center, Jamba Juice, JC Penney, Jos. A. Bank Clothiers, Nine West, Office Depot, Rooms To Go, Tiger Direct and Toys “R” Us, PayPal says.

Though PayPal is a player in "mobile payments," its arguably bigger strategic move is into the offline payment process, namely retailer transactions. Those efforts include a mobile component, but also feature use of the PayPal credit card.

The other notable point is that PayPal, like many other contestants, sees "payment" as part of a larger range of shopping activities where mobile devices can change the experience and add value.

These include: Abercrombie & Fitch, Advance Auto Parts, Aéropostale, American Eagle Outfitters, Barnes & Noble, Foot Locker, Guitar Center, Jamba Juice, JC Penney, Jos. A. Bank Clothiers, Nine West, Office Depot, Rooms To Go, Tiger Direct and Toys “R” Us, PayPal says.

Though PayPal is a player in "mobile payments," its arguably bigger strategic move is into the offline payment process, namely retailer transactions. Those efforts include a mobile component, but also feature use of the PayPal credit card.

The other notable point is that PayPal, like many other contestants, sees "payment" as part of a larger range of shopping activities where mobile devices can change the experience and add value.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, May 26, 2012

Telecom Now is a Multi-Product Business

Vodafone gets 14.5 percent of its £43 billion service revenue from mobile data, despite the fact that it represents the majority of traffic carried.

That points out one important new challenge for service providers operating multi-product businesses, where each service might have a different profit margin and revenue contribution.

You might even say that, at the moment, the highest-margin products are narrowband, representing a small percentage of total traffic.

Some products might represent high volume but low profit, while other services might represent low volume but high profit, with most services likely someplace in between those extremes.

One of the truisms about virtually every business is that 80 percent of the profits will tend to come from about 20 percent of the activities people at those businesses conduct. That “Pareto” distribution can apply for a business as a whole, as well as for each constituent product a company sells.

So it now is quite necessary to understand, in detail, what profit margin every single product delivers, as well as what the cost of each discrete service might be.

That points out one important new challenge for service providers operating multi-product businesses, where each service might have a different profit margin and revenue contribution.

You might even say that, at the moment, the highest-margin products are narrowband, representing a small percentage of total traffic.

Some products might represent high volume but low profit, while other services might represent low volume but high profit, with most services likely someplace in between those extremes.

One of the truisms about virtually every business is that 80 percent of the profits will tend to come from about 20 percent of the activities people at those businesses conduct. That “Pareto” distribution can apply for a business as a whole, as well as for each constituent product a company sells.

So it now is quite necessary to understand, in detail, what profit margin every single product delivers, as well as what the cost of each discrete service might be.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What, and How Big, is the M2M Market?

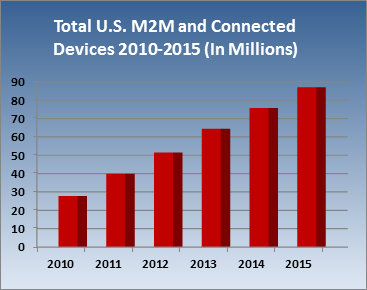

The “machine to machine” communications business is among a handful of truly-significant new revenue categories for mobile service providers. But figuring out how big that opportunity is, and how fast it is growing, is complicated.

One reason is that definitions of what constitutes an “M2M” service vary quite significantly. Some service providers consider mobile broadband connections to “non-voice” devices, such as tablets, to be “M2M” connections. Some would say that those are examples of “connected devices,” but not truly “M2M.”

Others define M2M as business-to-business telemetry and other apps where a human being is not the user of either devices on the ends of a connection. In other words, a wireless meter reader or heart monitor would be an example of M2M, but a connected iPad would not be an instance of M2M.

“Much confusion exists around what makes up M2M,” says James Brehm, Compass Intelligence senior strategist. “In defining the market, the GSMA includes devices like connected iPads and other media tablets, some tier-one mobile network operators include connected consumer electronics like picture frames, personal navigation devices, and the like, while others look solely to B2B applications,” says Brehm.

Those definitions matter for any observer trying to track the growth of M2M revenues. Some observers would say M2M in the “B2B” sense is more important than connected tablets and photo frames as it represents an entirely new category of mobile services, where connected tablets are an extension of today’s PC dongle business.

Some might prefer to track all non-phone revenues in a separate category than “phone” revenues for reasons of impact on average revenue per user. Most use cases within the broader M2M revenue category will involve connections with far less ARPU than phone connections generally represent.

But the caution is that using the broader definition, as the GSM does, inevitably will provide one view of how big the M2M business is. Using the narrower definitions will provide a different sense of market growth.

For the moment, it appears observers will have to guess at the revenue contributions made by tablet subscriptions, GPS devices and e-readers, as one category, from M2M revenue generated solely by telemetry and other B2b applications that many consider the core of the M2M revenue opportunity.

Of course, some might argue there is a clear “political” reason why the GSM and others choose the broader definition of M2M. It is easier to show revenue and category growth when using the broader definition. Executives will be anxious to demonstrate that they are gaining significant new revenue from M2M, which is among a handful of big growth opportunities for mobile service providers.

New market data from Berg Insight likewise shows strong momentum for M2M so far in 2012, showing year-over-year growth rates around 15 percent to 30 percent, Berg Insight says. Keep in mind that those estimates are made using the broader GSM definitions.

Among the mobile operators that officially report M2M subscriber statistics on a quarterly basis, AT&T reported the highest figure in the first quarter of 2012 of 13.3 million, up 25 percent year-on-year.

Vodafone reported 7.8 million M2M subscribers at the end of the financial year ending March 2012, up 47 percent from the previous year.

Japanese operators NTT DoCoMo, KDDI and Softbank recorded year-on-year growth rates in the range 20–35 percent and reported between 1.9 million and 2.4 million M2M subscribers each.

Many of the leading global mobile operators do not report M2M subscribers separately. Among these Berg Insight estimates that China Mobile has the largest installed base of around 15 million, followed by Verizon Wireless, T-Mobile and Telefónica at around 7–9 million.

T-Mobile USA is the only entity in the Deutsche Telekom group disclosing M2M subscriber data, reporting 2.7 million at the end of the first quarter of 2012. Other major M2M communication providers in Europe and North America include Orange, Telenor and Sprint, which had approximately three million to four million M2M subscribers each.

New categories seem continually to be added to the M2M device mix, as well. According to Berg Insight, the number of shipped consumer M2M devices with cellular connectivity grew to 7.1 million worldwide in 2011, up from 6.4 million in the previous year.

This relatively new breed of connected devices – neither classified as handsets, PCs, tablets nor traditional M2M devices, includes E-readers and personal navigation devices.

Handheld gaming consoles, personal tracking devices and wellness devices are promising categories as well, Berg Insight says.

the next five years, shipments of consumer M2M devices will grow at a compound annual growth rate (CAGR) of 39.8 percent to reach 37.9 million devices in 2016.

One way or the other, using a broader "connected non-phone devices" or a narrower "sensor" definition of M2M, the category is important. But current broad definitions will obscure progress made on the sensor communications business.

One reason is that definitions of what constitutes an “M2M” service vary quite significantly. Some service providers consider mobile broadband connections to “non-voice” devices, such as tablets, to be “M2M” connections. Some would say that those are examples of “connected devices,” but not truly “M2M.”

Others define M2M as business-to-business telemetry and other apps where a human being is not the user of either devices on the ends of a connection. In other words, a wireless meter reader or heart monitor would be an example of M2M, but a connected iPad would not be an instance of M2M.

“Much confusion exists around what makes up M2M,” says James Brehm, Compass Intelligence senior strategist. “In defining the market, the GSMA includes devices like connected iPads and other media tablets, some tier-one mobile network operators include connected consumer electronics like picture frames, personal navigation devices, and the like, while others look solely to B2B applications,” says Brehm.

Those definitions matter for any observer trying to track the growth of M2M revenues. Some observers would say M2M in the “B2B” sense is more important than connected tablets and photo frames as it represents an entirely new category of mobile services, where connected tablets are an extension of today’s PC dongle business.

Some might prefer to track all non-phone revenues in a separate category than “phone” revenues for reasons of impact on average revenue per user. Most use cases within the broader M2M revenue category will involve connections with far less ARPU than phone connections generally represent.

But the caution is that using the broader definition, as the GSM does, inevitably will provide one view of how big the M2M business is. Using the narrower definitions will provide a different sense of market growth.

For the moment, it appears observers will have to guess at the revenue contributions made by tablet subscriptions, GPS devices and e-readers, as one category, from M2M revenue generated solely by telemetry and other B2b applications that many consider the core of the M2M revenue opportunity.

Of course, some might argue there is a clear “political” reason why the GSM and others choose the broader definition of M2M. It is easier to show revenue and category growth when using the broader definition. Executives will be anxious to demonstrate that they are gaining significant new revenue from M2M, which is among a handful of big growth opportunities for mobile service providers.

New market data from Berg Insight likewise shows strong momentum for M2M so far in 2012, showing year-over-year growth rates around 15 percent to 30 percent, Berg Insight says. Keep in mind that those estimates are made using the broader GSM definitions.

Among the mobile operators that officially report M2M subscriber statistics on a quarterly basis, AT&T reported the highest figure in the first quarter of 2012 of 13.3 million, up 25 percent year-on-year.

Vodafone reported 7.8 million M2M subscribers at the end of the financial year ending March 2012, up 47 percent from the previous year.

Japanese operators NTT DoCoMo, KDDI and Softbank recorded year-on-year growth rates in the range 20–35 percent and reported between 1.9 million and 2.4 million M2M subscribers each.

Many of the leading global mobile operators do not report M2M subscribers separately. Among these Berg Insight estimates that China Mobile has the largest installed base of around 15 million, followed by Verizon Wireless, T-Mobile and Telefónica at around 7–9 million.

T-Mobile USA is the only entity in the Deutsche Telekom group disclosing M2M subscriber data, reporting 2.7 million at the end of the first quarter of 2012. Other major M2M communication providers in Europe and North America include Orange, Telenor and Sprint, which had approximately three million to four million M2M subscribers each.

New categories seem continually to be added to the M2M device mix, as well. According to Berg Insight, the number of shipped consumer M2M devices with cellular connectivity grew to 7.1 million worldwide in 2011, up from 6.4 million in the previous year.

This relatively new breed of connected devices – neither classified as handsets, PCs, tablets nor traditional M2M devices, includes E-readers and personal navigation devices.

Handheld gaming consoles, personal tracking devices and wellness devices are promising categories as well, Berg Insight says.

the next five years, shipments of consumer M2M devices will grow at a compound annual growth rate (CAGR) of 39.8 percent to reach 37.9 million devices in 2016.

One way or the other, using a broader "connected non-phone devices" or a narrower "sensor" definition of M2M, the category is important. But current broad definitions will obscure progress made on the sensor communications business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Consumers use of Smart Phones for Shopping and Recipes Shows Potential of Mobile Commerce

Mobile phone applications quickly are becoming the go-to source for countless daily tasks, including finding grocery deals, according to the NPD Group. That has implications for growth of mobile payments, use of mobiles for coupon delivery and marketing.

Consumers are using the Internet and social media to hunt down recipes, shop for food, and connect with their favorite food brands. That is one obvious linkage to delivery of information and inducements to buy specific brands and products used by various recipes.

Coupon apps are used by about 25 million Americans each month, and this happens most frequently in households with children. The foods these app couponing families consume more often skew towards kid friendly staples like eggs, cold cereal, bacon, sausages, macaroni and cheese, soup, and fruit juice.

More than half of U.S. consumers are aware of Groupon, the localized deal-of-the-day website, and about one in five consumers receives emails regularly from the service.

Consumers are using the Internet and social media to hunt down recipes, shop for food, and connect with their favorite food brands. That is one obvious linkage to delivery of information and inducements to buy specific brands and products used by various recipes.

Coupon apps are used by about 25 million Americans each month, and this happens most frequently in households with children. The foods these app couponing families consume more often skew towards kid friendly staples like eggs, cold cereal, bacon, sausages, macaroni and cheese, soup, and fruit juice.

More than half of U.S. consumers are aware of Groupon, the localized deal-of-the-day website, and about one in five consumers receives emails regularly from the service.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, May 25, 2012

Cisco to End "Cius" Tablet

Cisco will no longer invest in the Cisco Cius tablet form factor, and no further enhancements will be made to the current Cius endpoint beyond what’s available today, Cisco says.

Cisco will no longer invest in the Cisco Cius tablet form factor, and no further enhancements will be made to the current Cius endpoint beyond what’s available today, Cisco says.Cisco might continue to offer Cius "in a limited fashion" to customers with specific needs or use cases.

For a company that is "re-prioritizing" its efforts and ditching product lines that offer slim hopes for market leadership, the abandonment of any single product would not be unusual.

But the move might illustrate in a larger sense how hard it is for large service providers and large application and software firms with an enterprise orientation to create products for consumers or even business customers, in a market where consumer grade hardware is winning the day.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Lawsuits Pose Major Tests of Broadcast TV Business Model

A couple major tests of the business relationship between over-the-air broadcast networks and video distributors have started bubbling through the courts, with direct major consequences for Dish Network, a start-up known as Aereo, and the major broadcast TV networks.

At least in principle, the outcome of those two court cases could reset broadcast network revenue expectations and content carriage costs for for all telco and cable distributions of broadcast TV network programming as well.

SNL Kagan, for example, says that the broadcast networks and local television stations will be pulling in more than $3.6 billion annually in so-called retransmission consent fees from cable and satellite operators by the end of 2017. In 2010, SNL Kagan said retransmission consent generated about $1.14 billion.

None of the cases are unprecedented. Broadcasters and cable companies have sparred for years over the commercial agreements around “retransmission consent,” the ability of a video distributor to re-transmit broadcast network programming.

And lawsuits about the lawfulness of ad-skipping technology, as well as other technologies such as VCRs, have been filed in the past, as well.

In the first set of lawsuits, Dish Network and leading TV networks are suing each other over Dish’s plan to allow automatic skipping of all ads on broadcast network prime time shows.

The second set of lawsuits have been levied by broadcast networks against Aereo, a streaming service that charges $12 a month to stream the local broadcast signals of TV stations over the Web to consumers' iPads or computers. It is currently available only in New York City.

The lawsuits against Dish Network’s “Hopper” set-top and integrated DVR are not the first time networks have sued DVR suppliers over ad-skipping. By my reading it is at least the third time, with lots of skirmishes.

Sonicblue was put out of business, while TiVo simply stopped offering the ad-skipping feature.

Aereo insists what it is doing is legal. In essence, its service includes a dedicated off-air antenna for each customer, much as a homeowner might mount a rooftop antenna. The difference is that Aereo records and stores that video. A consumer has the legal right to do that using a digital video recorder.

The issue, the broadcasters claim, is that Aereo reformats the signals, a traditionally key distinction in broadcast law. By reformatting, Aereo incurs the obligation to get permission from the broadcasters.

But that’s the perpetual issue: is the use of new technology to accomplish older operations an infraction of copyright, or not?

The issue with Hopper is only partly “whether it is legal” for a DVR to skip commercials. It might well be found legal. The issue is whether the broadcast TV business will be disrupted.

At least in principle, the outcome of those two court cases could reset broadcast network revenue expectations and content carriage costs for for all telco and cable distributions of broadcast TV network programming as well.

SNL Kagan, for example, says that the broadcast networks and local television stations will be pulling in more than $3.6 billion annually in so-called retransmission consent fees from cable and satellite operators by the end of 2017. In 2010, SNL Kagan said retransmission consent generated about $1.14 billion.

None of the cases are unprecedented. Broadcasters and cable companies have sparred for years over the commercial agreements around “retransmission consent,” the ability of a video distributor to re-transmit broadcast network programming.

And lawsuits about the lawfulness of ad-skipping technology, as well as other technologies such as VCRs, have been filed in the past, as well.

In the first set of lawsuits, Dish Network and leading TV networks are suing each other over Dish’s plan to allow automatic skipping of all ads on broadcast network prime time shows.

The second set of lawsuits have been levied by broadcast networks against Aereo, a streaming service that charges $12 a month to stream the local broadcast signals of TV stations over the Web to consumers' iPads or computers. It is currently available only in New York City.

The lawsuits against Dish Network’s “Hopper” set-top and integrated DVR are not the first time networks have sued DVR suppliers over ad-skipping. By my reading it is at least the third time, with lots of skirmishes.

Sonicblue was put out of business, while TiVo simply stopped offering the ad-skipping feature.

Aereo insists what it is doing is legal. In essence, its service includes a dedicated off-air antenna for each customer, much as a homeowner might mount a rooftop antenna. The difference is that Aereo records and stores that video. A consumer has the legal right to do that using a digital video recorder.

The issue, the broadcasters claim, is that Aereo reformats the signals, a traditionally key distinction in broadcast law. By reformatting, Aereo incurs the obligation to get permission from the broadcasters.

But that’s the perpetual issue: is the use of new technology to accomplish older operations an infraction of copyright, or not?

The issue with Hopper is only partly “whether it is legal” for a DVR to skip commercials. It might well be found legal. The issue is whether the broadcast TV business will be disrupted.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...