Australia's minimum prices for new spectrum to be auctioned are too high, and some bidders already are saying they won't be bidding bidding.

The Australian Communications and Media Authority has set the reserve price for 700 MHz spectrum at $1.36 per megahertz (MHz) per population.

Vodafone and Telstra say they won't bid at those prices. Optus says the minimum price is too high.

3G

Auctions held recently in the Netherlands saw prices higher than anticipated, which as service providers worried a ruinous bidding war could result. That was a near-disaster when the same thing happened during 3G auctions.

European mobile phone companies spent $129 billion six years ago to buy 3G licenses that were expected to trigger new revenue-generating services. As recently as 2006, though, that had not proven to be the case.

Service providers cannot afford to make that mistake again.

Sunday, December 16, 2012

What If They Hold a 4G Auction and Nobody Bids?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, December 15, 2012

The 3% Rule for Pricing Broadband Access Services, Anywhere

Why are broadband access prices so different, around the world? There's a simple answer, actually: retail prices are directly related to cost of construction in each market, and also substantially directly related to median household income.

You might think "things cost what they cost," and that is true, but what things cost varies from place to place

Recent studies published by ITU reveal that broadband penetration is directly related to its cost, relative to an average family income, as well as to the availability of products and services that accommodate the general population’s purchasing ability.

That also explains why high speed access costs vary rather broadly from country to country. Areas where it costs more to create the infrastructure will tend to be more expensive, at the retail level. Areas where it costs less to create networks will correlate with lower retail costs.

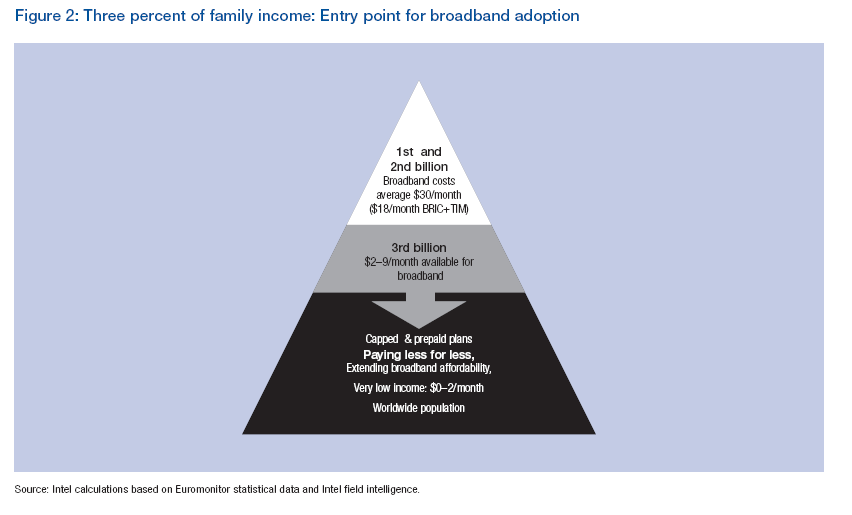

For example, as the annual cost of broadband drops below three percent of a family’s annual income, broadband usage begins to increase dramatically.

For developed countries, this relative cost has already been achieved, but for at least 34 countries worldwide, the cost of broadband remains higher than the average annual family income, the ITU says.

But that’s an important bit of retail pricing advice for would-be ISPs in developing regions: set monthly prices no higher than three percent of median household income.

And prices are falling, globally.Between 2008 and 2009, 125 countries saw reductions in access prices, some by as much as 80 percent, the ITU says. Between 2009 and 2011, for example, prices for fixed broadband have dropped by 52.2 percent on average and mobile broadband prices by 22 percent, globally.

Affordable broadband programs are starting to emerge in countries such as Sri Lanka and India, with service providers offering connectivity solutions starting as low as US$2 per month.

And while it is natural for a seller to want higher prices, for Internet access providers, less is more, in the sense of keeping at or below the “three percent of median household income” rule for retail pricing.

The trade-off is lower average revenue per user, but many more users. So where median high speed access costs in developed regions might run about $30 a month, in the BRIC+TIM areas costs might be $18 a month.

Somewhere between $2 and $9 a month would reach another billion or so households in a number of regions and countries. In the poorest nations, prepaid plans costing less than $2 a month will be needed.

Brazil, Russia, India, China, Turkey, Indonesia, and Mexico (BRIC+TIM countries), for example, could grow their available market by 860 million people by reducing the cost of entry for broadband by about 50 percent..

In 2011, the price of fixed broadband access cost less than two percent of average monthly income in 49 economies in the world, mostly in the industrialized world.

Meanwhile, broadband access cost more than half of average national income in 30 economies. In 19 of the lesser developed countries, the price of broadband exceeds average monthly income.

By 2011, there were 48 developing economies where entry-level broadband access cost less than five percent of average monthly income, up from just 35 countries the year before.

To take the example of Kenya, family income levels mean that only about seven percent of the population can afford a service that offers uncapped monthly broadband access for US$20 per month. A prepaid broadband access service capped at 200 MB of data for US$5, however, could be within the reach of more than 60 percent of the Kenyan population.

Safaricom, the largest Internet service provider in Kenya, launched a segmented prepaid broadband offer in the end of 2009 targeted at different income levels.

There were 589 million fixed broadband subscriptions by the end of 2011 (most of which were located in the developed world), but nearly twice as many mobile broadband subscriptions at 1.09 billion, the ITU says.

Beyond that, since trenches, ducts and dark fiber represent as much as 70 percent of total cost to build a broadband network, the wisdom of using wireless is obvious. Wireless attacks that part of the effort consuming up to 70 percent of capital investment.

You might think "things cost what they cost," and that is true, but what things cost varies from place to place

Recent studies published by ITU reveal that broadband penetration is directly related to its cost, relative to an average family income, as well as to the availability of products and services that accommodate the general population’s purchasing ability.

That also explains why high speed access costs vary rather broadly from country to country. Areas where it costs more to create the infrastructure will tend to be more expensive, at the retail level. Areas where it costs less to create networks will correlate with lower retail costs.

For example, as the annual cost of broadband drops below three percent of a family’s annual income, broadband usage begins to increase dramatically.

For developed countries, this relative cost has already been achieved, but for at least 34 countries worldwide, the cost of broadband remains higher than the average annual family income, the ITU says.

But that’s an important bit of retail pricing advice for would-be ISPs in developing regions: set monthly prices no higher than three percent of median household income.

And prices are falling, globally.Between 2008 and 2009, 125 countries saw reductions in access prices, some by as much as 80 percent, the ITU says. Between 2009 and 2011, for example, prices for fixed broadband have dropped by 52.2 percent on average and mobile broadband prices by 22 percent, globally.

Affordable broadband programs are starting to emerge in countries such as Sri Lanka and India, with service providers offering connectivity solutions starting as low as US$2 per month.

And while it is natural for a seller to want higher prices, for Internet access providers, less is more, in the sense of keeping at or below the “three percent of median household income” rule for retail pricing.

The trade-off is lower average revenue per user, but many more users. So where median high speed access costs in developed regions might run about $30 a month, in the BRIC+TIM areas costs might be $18 a month.

Somewhere between $2 and $9 a month would reach another billion or so households in a number of regions and countries. In the poorest nations, prepaid plans costing less than $2 a month will be needed.

Brazil, Russia, India, China, Turkey, Indonesia, and Mexico (BRIC+TIM countries), for example, could grow their available market by 860 million people by reducing the cost of entry for broadband by about 50 percent..

In 2011, the price of fixed broadband access cost less than two percent of average monthly income in 49 economies in the world, mostly in the industrialized world.

Meanwhile, broadband access cost more than half of average national income in 30 economies. In 19 of the lesser developed countries, the price of broadband exceeds average monthly income.

By 2011, there were 48 developing economies where entry-level broadband access cost less than five percent of average monthly income, up from just 35 countries the year before.

To take the example of Kenya, family income levels mean that only about seven percent of the population can afford a service that offers uncapped monthly broadband access for US$20 per month. A prepaid broadband access service capped at 200 MB of data for US$5, however, could be within the reach of more than 60 percent of the Kenyan population.

Safaricom, the largest Internet service provider in Kenya, launched a segmented prepaid broadband offer in the end of 2009 targeted at different income levels.

There were 589 million fixed broadband subscriptions by the end of 2011 (most of which were located in the developed world), but nearly twice as many mobile broadband subscriptions at 1.09 billion, the ITU says.

Beyond that, since trenches, ducts and dark fiber represent as much as 70 percent of total cost to build a broadband network, the wisdom of using wireless is obvious. Wireless attacks that part of the effort consuming up to 70 percent of capital investment.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

How Many Voice Lines in Use by 2018?

The Federal Communications Commission Technology Advisory Council thinks U.S. time division multiplex fixed consumer access lines could dip to perhaps 20 million units by about 2018.

The Federal Communications Commission Technology Advisory Council thinks U.S. time division multiplex fixed consumer access lines could dip to perhaps 20 million units by about 2018. Others, such as Kent Larsen, CHR Solutions SVP, think lines overall could dip to about 50 million over the next five years, then to about 40 million on a long term and somewhat stable basis.

The TAC forecast might be tempered by its omission of business lines or perhaps voice lines provided over broadband connections. But the general direction, if not magnitude, are hard to argue with.

Access lines in use are declining. A peak seems to have occurred sometime between 1999 and 2001, in the U.S. market. Mobile lines grabbed leadership, in terms of lines in use, shortly thereafter.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Even if You Want To, Can You Price Apps by Gigabyte?

It seems a virtual certainty that investors will change the way they evaluate telecom access provider assets in the future, as they have done in the past. The reason is that the older metrics provide less value in assessing service provider prospects.

Once upon a time, access lines were a predictable indicator of telco performance, globally. With no competition and set prices, the primary variable was the number of access lines in service.

Once upon a time, basic video subscriptions likewise were a reliable indicator of how well a cable TV provider was doing or was expected to do.

That began to change with the advent of IP-based services, competition and multiple product lines. Because of competition, no provider formerly used to having 70 percent to 95 percent take rates could make those assumptions any longer. Instead, business plans had to be based on take rates as low as 20 percent to 30 percent, for any single product.

Also, with multiple products being sold, revenue per unit, or revenue per account, became more relevant than sheer numbers of accounts in service. Overall, “lines” or “subscribers” have become less meaningful measures.

At some point, especially as the IP transition continues, it is likely that newer metrics will start to emerge. Specific services, such as voice or messaging, might, or might not, be “revenue” sources in the same way.

When “bandwidth” begins to be an underpinning for all the other applications and services, it might be desirable, or necessary, to devise new metrics that correlate use of the network with revenue.

Some might argue that is a mere application of value based pricing to communications products, where retail prices are set based on customer perception of the value, not the cost of creating the products or the historical prices paid for those products.

Value-based pricing is predicated upon an understanding of customer value, a concept that will not be especially common for telecom executives, who for legacy reasons have set prices based on “cost.” In the monopoly period of industry operations, carriers made profits based on a cost-plus basis, so that made sense.

These days, matters are more complex. “Today, everything is about pricing, not cost,” says CHR Solutions SVP Kent Larsen. What he means is that “customer experience” now underpins the ability to price and sell products. One reason triple play offers work is that consumers rightly consider that they are getting a discount.

In other cases, offering free features is an obvious way to boost perceived value, even if, in fact, there is full cost recovery overall. But costs are an issue.

Here’s a really scary way of looking at how mobile and fixed network operating metrics might have to change: “costs per gigabyte must decrease by 90 percent every three to four years” just to keep service provider revenues and costs in the same relationship as they are now, according to Norman Fekrat, former IBM Global Business Services partner and VP.

And the bad news, says Fekrat, is that, at the moment, service provider costs are “increasing when it needs to decrease.”

“The cost structures need to be reduced significantly,” not incrementally, he says. And that will not be easy, Fekrat argues.

He thinks service providers will have to move to an alternative notion of “profit per gigabyte per service type,” where the actual cost of delivering a service is matched to the bandwidth consumed, for example.

That will be challenging. Consider the problem of pricing for consumption of video entertainment, the most bandwidth-intensive service. Though a two-hour movie might consume 3.8 Gbytes, the consumer might expect to pay about $5 for a viewing, or about $1.31 per gigabyte of revenue.

On the other hand, a month’s worth of voice might consume only hundreds of megabytes. Even if a user talks on the phone for 24 hours per day, every day for a month, using a high-quality codec, it would consume about a gigabyte each day, or perhaps 45 Mbytes for an hour.

If a user talks for an hour a day, that might represent consumption of about 1.35 Gbytes a month. On a flat rate $30 a month voice plan, that would work out to revenue of about $22 per gigabyte.

Messaging consumes almost no bandwidth, and could represent revenue of $800 a gigabyte.

That shows only one aspect of value-based pricing. Some of the applications have high value, but consume little bandwidth. Other apps consume lots of bandwidth, but have only moderate value.

Simple pricing based on bandwidth consumed will not work, in a value-based scenario. As logical as it might be to charge for apps based on "network resources consumed," that will meet huge consumer resistance, if one compares video entertainment to voice or messaging.

Once upon a time, access lines were a predictable indicator of telco performance, globally. With no competition and set prices, the primary variable was the number of access lines in service.

Once upon a time, basic video subscriptions likewise were a reliable indicator of how well a cable TV provider was doing or was expected to do.

That began to change with the advent of IP-based services, competition and multiple product lines. Because of competition, no provider formerly used to having 70 percent to 95 percent take rates could make those assumptions any longer. Instead, business plans had to be based on take rates as low as 20 percent to 30 percent, for any single product.

Also, with multiple products being sold, revenue per unit, or revenue per account, became more relevant than sheer numbers of accounts in service. Overall, “lines” or “subscribers” have become less meaningful measures.

At some point, especially as the IP transition continues, it is likely that newer metrics will start to emerge. Specific services, such as voice or messaging, might, or might not, be “revenue” sources in the same way.

When “bandwidth” begins to be an underpinning for all the other applications and services, it might be desirable, or necessary, to devise new metrics that correlate use of the network with revenue.

Some might argue that is a mere application of value based pricing to communications products, where retail prices are set based on customer perception of the value, not the cost of creating the products or the historical prices paid for those products.

Value-based pricing is predicated upon an understanding of customer value, a concept that will not be especially common for telecom executives, who for legacy reasons have set prices based on “cost.” In the monopoly period of industry operations, carriers made profits based on a cost-plus basis, so that made sense.

These days, matters are more complex. “Today, everything is about pricing, not cost,” says CHR Solutions SVP Kent Larsen. What he means is that “customer experience” now underpins the ability to price and sell products. One reason triple play offers work is that consumers rightly consider that they are getting a discount.

In other cases, offering free features is an obvious way to boost perceived value, even if, in fact, there is full cost recovery overall. But costs are an issue.

Here’s a really scary way of looking at how mobile and fixed network operating metrics might have to change: “costs per gigabyte must decrease by 90 percent every three to four years” just to keep service provider revenues and costs in the same relationship as they are now, according to Norman Fekrat, former IBM Global Business Services partner and VP.

And the bad news, says Fekrat, is that, at the moment, service provider costs are “increasing when it needs to decrease.”

“The cost structures need to be reduced significantly,” not incrementally, he says. And that will not be easy, Fekrat argues.

He thinks service providers will have to move to an alternative notion of “profit per gigabyte per service type,” where the actual cost of delivering a service is matched to the bandwidth consumed, for example.

That will be challenging. Consider the problem of pricing for consumption of video entertainment, the most bandwidth-intensive service. Though a two-hour movie might consume 3.8 Gbytes, the consumer might expect to pay about $5 for a viewing, or about $1.31 per gigabyte of revenue.

On the other hand, a month’s worth of voice might consume only hundreds of megabytes. Even if a user talks on the phone for 24 hours per day, every day for a month, using a high-quality codec, it would consume about a gigabyte each day, or perhaps 45 Mbytes for an hour.

If a user talks for an hour a day, that might represent consumption of about 1.35 Gbytes a month. On a flat rate $30 a month voice plan, that would work out to revenue of about $22 per gigabyte.

Messaging consumes almost no bandwidth, and could represent revenue of $800 a gigabyte.

That shows only one aspect of value-based pricing. Some of the applications have high value, but consume little bandwidth. Other apps consume lots of bandwidth, but have only moderate value.

Simple pricing based on bandwidth consumed will not work, in a value-based scenario. As logical as it might be to charge for apps based on "network resources consumed," that will meet huge consumer resistance, if one compares video entertainment to voice or messaging.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Economics Will Drive More Telco Consolidation

Are rural and independent telcos exempt from the “laws of economics?” If you think they are exempt, then consolidation, mergers and even bankruptcies will not happen in the U.S. independent telco business.

If, on the other hand, you believe economics and markets do matter, then it is inevitable that the structure of the U.S. rural and independent telecom business must eventually change. Some, including CHR Solutions SVP Kent Larsen, think that consolidation process will begin by 2014 or 2015.

Here’s the argument, in a nutshell. For starters, “wireless now is the preferred consumer choice” for voice and messaging, and might begin to be a more-logical choice even for broadband access. If nothing else were happening, that would put fixed network service providers at a disadvantage.

One immediate consequence is that there is less demand for fixed network voice lines and usage. The corollary is that it is hard to “grow revenues.” Simply, the historic revenue sources are dwindling and the new services (video entertainment and high-speed access) arguably are modestly profitable.

So cash flow is diminishing. That doesn’t mean many rural telcos do not have cash available. They do, says Larsen. But they can’t find suitable places to invest that cash, in the business.

source: CHR

Some will argue they should invest in upgraded networks. But the payback from such initiatives is questionable. The basic problem is that it is hard to make the case that network upgrades generate enough incremental revenue to pay for the investments.

If you wonder why AT&T and Verizon Wireless have concluded that Long Term Evolution makes sense everywhere they cannot afford to invest in fiber to the home, that’s your answer. There simply are places where fiber to the home provides a negative rate of return.

Under the best of circumstances, most rural or independent fixed network service providers would not be able to survive without government subsidies of one sort or another.

But circumstances are far from optimal.

Demography is in many ways destiny. And it simply is a fact that rural areas are losing population, says Larsen. That means fewer future customers. The customers that do remain are older than the U.S. average. That means, sooner or later, those people stop being customers.

And communications remains a highly capital intensive business. That means scale matters, since the lowest-cost provider in the market tends to win, in the end, Larsen notes.

It isn’t that smaller telcos are inefficient. In fact, they probably operate about as efficiently as they can, in terms of operating cost. But that’s part of the problem. “A 3,000-customer company can’t take out much cost,” Larsen adds.

But that is why mergers will have to happen. Unless a firm wants to go bankrupt, sooner or later, firms must combine, which will produce the operating cost advantages combinations of similar firms always provide. Overhead can be cut.

And it even is possible to predict where such mergers will happen: between companies that are in close proximity. The reason also is driven by economics: combining nearby firms will allow elimination of redundant resources. Acquisitions of far-away firms do not provide significant similar advantages.

Historically, a few firms in the independent telco industry have been acquirers. Windstream and Frontier Communications, or Fairpoint, come to mind. But those firms now are concentrating on rationalizing what they already have, so are essentially out of the market for further significant acquisitions.

That leaves only “merger of equals” opportunities on a smaller and local scale.

Nor is consolidation an issue only for rural telcos. Most independent competitive local exchange carriers and wireless ISPs sooner or later will face the same fundamental issues. It’s just the economics of a mature scale business at a time when revenue and cost pressures are rising.

Big or small, consolidation always happens in the communications business, sooner or later.

If, on the other hand, you believe economics and markets do matter, then it is inevitable that the structure of the U.S. rural and independent telecom business must eventually change. Some, including CHR Solutions SVP Kent Larsen, think that consolidation process will begin by 2014 or 2015.

Here’s the argument, in a nutshell. For starters, “wireless now is the preferred consumer choice” for voice and messaging, and might begin to be a more-logical choice even for broadband access. If nothing else were happening, that would put fixed network service providers at a disadvantage.

One immediate consequence is that there is less demand for fixed network voice lines and usage. The corollary is that it is hard to “grow revenues.” Simply, the historic revenue sources are dwindling and the new services (video entertainment and high-speed access) arguably are modestly profitable.

So cash flow is diminishing. That doesn’t mean many rural telcos do not have cash available. They do, says Larsen. But they can’t find suitable places to invest that cash, in the business.

source: CHR

Some will argue they should invest in upgraded networks. But the payback from such initiatives is questionable. The basic problem is that it is hard to make the case that network upgrades generate enough incremental revenue to pay for the investments.

If you wonder why AT&T and Verizon Wireless have concluded that Long Term Evolution makes sense everywhere they cannot afford to invest in fiber to the home, that’s your answer. There simply are places where fiber to the home provides a negative rate of return.

Under the best of circumstances, most rural or independent fixed network service providers would not be able to survive without government subsidies of one sort or another.

But circumstances are far from optimal.

Demography is in many ways destiny. And it simply is a fact that rural areas are losing population, says Larsen. That means fewer future customers. The customers that do remain are older than the U.S. average. That means, sooner or later, those people stop being customers.

And communications remains a highly capital intensive business. That means scale matters, since the lowest-cost provider in the market tends to win, in the end, Larsen notes.

It isn’t that smaller telcos are inefficient. In fact, they probably operate about as efficiently as they can, in terms of operating cost. But that’s part of the problem. “A 3,000-customer company can’t take out much cost,” Larsen adds.

But that is why mergers will have to happen. Unless a firm wants to go bankrupt, sooner or later, firms must combine, which will produce the operating cost advantages combinations of similar firms always provide. Overhead can be cut.

And it even is possible to predict where such mergers will happen: between companies that are in close proximity. The reason also is driven by economics: combining nearby firms will allow elimination of redundant resources. Acquisitions of far-away firms do not provide significant similar advantages.

Historically, a few firms in the independent telco industry have been acquirers. Windstream and Frontier Communications, or Fairpoint, come to mind. But those firms now are concentrating on rationalizing what they already have, so are essentially out of the market for further significant acquisitions.

That leaves only “merger of equals” opportunities on a smaller and local scale.

Nor is consolidation an issue only for rural telcos. Most independent competitive local exchange carriers and wireless ISPs sooner or later will face the same fundamental issues. It’s just the economics of a mature scale business at a time when revenue and cost pressures are rising.

Big or small, consolidation always happens in the communications business, sooner or later.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Netherlands Spectrum Auction Raises "Overpayment" Issue, Again

As you might expect, most of the new 4G spectrum that recently was won in the Netherlands spectrum auction were the biggest mobile service providers in the Netherlands. That happened despite restrictions on how much new spectrum the leading mobile service providers could acquire.

In the auction, two spectrum blocks in the 800 megahertz band and one in the 900 MHz band will be reserved for new entrants. That was the provision that allowed Swedish mobile operator Tele-2 to secure 20 megahertz of spectrum in the 800 MHz band.

Vodafone and KPN spent the most, with T-Mobile spending about 66 percent of what Vodafone and KPN invested. Tele-2 spent about 12 percent of what Vodafone and KPN spent, but also acquired a modest chunk of the new spectrum.

KPN has about 47 percent market share , while Vodafone has about 29 percent and T-Mobile has about 24 percent. Tele-2, a Swedish operator, also is entering the market.

The 3.8 billion euros ($4.97 billion) proceeds were much higher than observers anticipated, far surpassing the EUR400-500 million the government had expected.

That might have implications for spectrum auctions elsewhere in Europe, In the United Kingdom, 4G spectrum auctions will be available in the first half of 2013, for example.

KPN argues it won “a better package than Vodafone”, having picked up about 30 megahertz more spectrum than Vodafone acquired, the Financial Times reports.

Auction results

Vodafone spent 1,380,800,000 euro (1.381 billion); KPN 1,351,852,000 euros (1.352 billion);

T-Mobile 910,681,000 euro (910.8 million) and Tele2 euro 160,813,000 (160.8 million).

Whether spectrum caps actually work is debatable, though policymakers are fond of the concept as a way to "stimulate competition" in the mobile market. In the recent Netherlands instance, one new operator was enticed to enter the market, but the overwhelming amount of new spectrum was won by the three firms that already lead the Netherlands market.

One might argue that either spectrum caps or set-aside policies to encourage new entrants "work" as a matter of prudent public policy. In other words, "it sounds good." Whether they actually are beneficial in the long run is probably a bigger issue. Over time, market consolidate.

Whether a small spectrum holding ultimately benefits consumers, or only enriches investors in the new firms, is a matter of debate. Some might even argue consumers do not benefit in the short term.

It would be hard to make the argument that spectrum policies aimed at promoting new entrants have done anything to stop concentration in the U.S. mobile industry, for example.

On a more prosaic level, European mobile service provider executives might now start to worry about what new Long Term Evolution spectrum might wind up costing, across the continent. Mobile service providers have been through ruinous spectrum wars before, precisely caused by the bidding for 3G licenses that nearly bankrupted a number of major European service providers.

If the Netherlands prices are replicated elsewhere, that danger is emerging again. If so, we might someday find out that the real "winners" of the upcoming LTE 4G auctions were the firms that "lost" the spectrum auction.

In the auction, two spectrum blocks in the 800 megahertz band and one in the 900 MHz band will be reserved for new entrants. That was the provision that allowed Swedish mobile operator Tele-2 to secure 20 megahertz of spectrum in the 800 MHz band.

Vodafone and KPN spent the most, with T-Mobile spending about 66 percent of what Vodafone and KPN invested. Tele-2 spent about 12 percent of what Vodafone and KPN spent, but also acquired a modest chunk of the new spectrum.

KPN has about 47 percent market share , while Vodafone has about 29 percent and T-Mobile has about 24 percent. Tele-2, a Swedish operator, also is entering the market.

The 3.8 billion euros ($4.97 billion) proceeds were much higher than observers anticipated, far surpassing the EUR400-500 million the government had expected.

That might have implications for spectrum auctions elsewhere in Europe, In the United Kingdom, 4G spectrum auctions will be available in the first half of 2013, for example.

KPN argues it won “a better package than Vodafone”, having picked up about 30 megahertz more spectrum than Vodafone acquired, the Financial Times reports.

Auction results

| Frequency Band | 800 | 900 | 1800 | 2100 | 1900 | 2600 |

| KPN | 2x10 | 2x10 | 2x20 | 2x5 | 30 | |

| Vodafone | 2x10 | 2x10 | 2x20 | 2x5 | ||

| T-Mobile | 2x15 | 2x30 | 4,9+9,7 | 25 | ||

| Tele2 | 2x10 |

Vodafone spent 1,380,800,000 euro (1.381 billion); KPN 1,351,852,000 euros (1.352 billion);

T-Mobile 910,681,000 euro (910.8 million) and Tele2 euro 160,813,000 (160.8 million).

Whether spectrum caps actually work is debatable, though policymakers are fond of the concept as a way to "stimulate competition" in the mobile market. In the recent Netherlands instance, one new operator was enticed to enter the market, but the overwhelming amount of new spectrum was won by the three firms that already lead the Netherlands market.

One might argue that either spectrum caps or set-aside policies to encourage new entrants "work" as a matter of prudent public policy. In other words, "it sounds good." Whether they actually are beneficial in the long run is probably a bigger issue. Over time, market consolidate.

Whether a small spectrum holding ultimately benefits consumers, or only enriches investors in the new firms, is a matter of debate. Some might even argue consumers do not benefit in the short term.

It would be hard to make the argument that spectrum policies aimed at promoting new entrants have done anything to stop concentration in the U.S. mobile industry, for example.

On a more prosaic level, European mobile service provider executives might now start to worry about what new Long Term Evolution spectrum might wind up costing, across the continent. Mobile service providers have been through ruinous spectrum wars before, precisely caused by the bidding for 3G licenses that nearly bankrupted a number of major European service providers.

If the Netherlands prices are replicated elsewhere, that danger is emerging again. If so, we might someday find out that the real "winners" of the upcoming LTE 4G auctions were the firms that "lost" the spectrum auction.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, December 14, 2012

Global Internet Users Doubled in 6 Years

Developing nations will become the focus of broadband growth over the next decade or two, building on a substantial amount of growth since about 2005.

By the end of 2011 2.3 billion people (around a third the world’s population) accessed the internet globally, almost double the 1.2 billion figure recorded in 2006, according to Ofcom.

Over this period growth in internet use was fastest among developing countries, and by 2011 62 percent of Internet users were located in developing countries, an increase from 44 percent in 2006.

And though Brazil, Russia, India, China and South Africa have been leading economic and communications adoption growth for much of the past decade, it now appears that those nations are reaching maturity, and that growth of communications services will be lead by a new list of nations in the emerging markets.

In significant part, that expansion will be driven by economic growth of middle classes most everywhere in the developing world over the next 15-20 years, according to the National Intelligence Council.

India, China and the rest of Asia provide important examples, as those regions will far outstrip the share of middle class consumption in the United States, Japan and European Union, for example.

India and China are doing this at a scale and pace not seen before: 100 times the people than Britain and yet a doubling of GDP in one tenth the time. By 2030 Asia will be well on its way to returning to being the world’s powerhouse, just as it was before 1500, NIC analysts say.

IDC, for example, predicts that emerging markets will contribute for 53 percent of 2012’s global information and communications technology growth.

And a poll of 675 global IT and business professionals suggests Indonesia, Vietnam, Qatar and Myanmar are the countries to lead that growth. Regionally, Asia-Pacific (exclusive of China and India) was cited by compared to 61 percent of survey respondents as the region most likely to lead revenue growth.

Notably, just five percent of respondents chose Brazil, Russia, India, China or South Africa as among the nations having the strongest growth, though the so-called BRICS nations have been at the top of global growth lists for some years.

In Indonesia, for example, there are around 55 million internet users. But that’s just a tiny fraction (22 percent) of its 245 million population. But growth is going to be rapid. The number of internet users grew 29 percent in the most recent year.

Predictions point to 76 million users by 2015. Perhaps ironically, the majority of Internet users are accessing the web while on the go, and not from a desk. While mobile penetration is at 54 percent, PC penetration is just five percent.

In Vietnam, 2012 information technology spending will have increased by 19 percent, IDC says.

By 2015, about 45 percent of the population will be using the Internet by 2015, up from about 30 percent in 2012.

IDC is expects 15 percent year-over-year growth of information technology and communications spending in Myanmar in 2012. Internet usage is quite low, probably in low single digits, while mobile penetration rates likely are similar.

By the end of 2011 2.3 billion people (around a third the world’s population) accessed the internet globally, almost double the 1.2 billion figure recorded in 2006, according to Ofcom.

Over this period growth in internet use was fastest among developing countries, and by 2011 62 percent of Internet users were located in developing countries, an increase from 44 percent in 2006.

And though Brazil, Russia, India, China and South Africa have been leading economic and communications adoption growth for much of the past decade, it now appears that those nations are reaching maturity, and that growth of communications services will be lead by a new list of nations in the emerging markets.

In significant part, that expansion will be driven by economic growth of middle classes most everywhere in the developing world over the next 15-20 years, according to the National Intelligence Council.

India, China and the rest of Asia provide important examples, as those regions will far outstrip the share of middle class consumption in the United States, Japan and European Union, for example.

Note the dramatic increase in economic growth the Council expects will happen between now and 2030. It took Britain 155 years to double gross domestic product per capita, The United States and Germany took between 30 and 60 years to do so.

India and China are doing this at a scale and pace not seen before: 100 times the people than Britain and yet a doubling of GDP in one tenth the time. By 2030 Asia will be well on its way to returning to being the world’s powerhouse, just as it was before 1500, NIC analysts say.

IDC, for example, predicts that emerging markets will contribute for 53 percent of 2012’s global information and communications technology growth.

And a poll of 675 global IT and business professionals suggests Indonesia, Vietnam, Qatar and Myanmar are the countries to lead that growth. Regionally, Asia-Pacific (exclusive of China and India) was cited by compared to 61 percent of survey respondents as the region most likely to lead revenue growth.

Notably, just five percent of respondents chose Brazil, Russia, India, China or South Africa as among the nations having the strongest growth, though the so-called BRICS nations have been at the top of global growth lists for some years.

In Indonesia, for example, there are around 55 million internet users. But that’s just a tiny fraction (22 percent) of its 245 million population. But growth is going to be rapid. The number of internet users grew 29 percent in the most recent year.

Predictions point to 76 million users by 2015. Perhaps ironically, the majority of Internet users are accessing the web while on the go, and not from a desk. While mobile penetration is at 54 percent, PC penetration is just five percent.

In Vietnam, 2012 information technology spending will have increased by 19 percent, IDC says.

By 2015, about 45 percent of the population will be using the Internet by 2015, up from about 30 percent in 2012.

IDC is expects 15 percent year-over-year growth of information technology and communications spending in Myanmar in 2012. Internet usage is quite low, probably in low single digits, while mobile penetration rates likely are similar.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

"IP Transition:" Turning Off PSTN by Another Name

There is a very-practical reason why discussion of a transition to IP technology, and an end to time division multiplex technology, is accelerating in the U.S. market and policy community.

If you look at services with growing revenue, those services are on networks using Internet Protocol. If you look at services whose revenues are declining or peaking, those services are on the legacy time division multiplex network.

Simply, customers are deserting the older networks in favor of mobile and broadband alternatives that are IP-based. And that means revenues are declining on networks with high fixed costs.

At some point, there will be so few customers left on the older networks that they cannot be supported any longer, especially when all legacy services can be delivered using the new IP networks.

Nor is the IP transition “just” a U.S. problem. Mobile broadband supplied by the mobile IP network now is driving revenue growth, while voice revenues on TDM networks are declining at serious rates in the United Kingdom, France, Germany, Italy, the United States, Canada, Japan, Australia, Spain, the Netherlands, Sweden, Ireland, Poland, Brazil, Russia, India and China in 2011, a study by Ofcom, the United Kingdom communications regulator, finds.

Fixed voice revenues fell, collectively, by an average of 7.3 percent in 2011, compared to a 7.1 percent decrease in 2010.

In contrast, mobile data has seen the fastest growth rate, with a compound annual growth rate of 25.4 percent between 2006 and 2011. That’s one of the newer IP networks.

The IP transition for the whole U.S. communications business is getting new attention as the Federal Communications Commission launches a new effort to plan for an end to the time division multiplex “public switched telephone network.”

"The Technology Transitions Policy Task Force will play a critical role in answering the fundamental policy question for communications in the 21st century: In a broadband world, how can we best ensure that our nation's communications policies continue to drive a virtuous cycle of innovation and investment, promote competition, and protect consumers?" said FCC Chairman Julius Genachowski.

The effort will face lots of political pressure from lots of vested interests whose business interests might be helped or harmed in any transition. But the transition has to happen. Voice, the specific service the TDM network was built to deliver, cannot support the network, long term.

Fixed voice still represents 25 percent of total service provider revenue in the 17 countries, Ofcom reports. But only a quarter of total revenues. And those revenues steadily are declining.

Fixed voice revenues fell by 5.2 percent in the United Kingdom during 2011, a higher rate that the 3.3 percent average in the five years to 2011.

Significant declines in voice pricing are largely to blame. The fastest rates of fixed voice pricing decline being found in the BRIC (Brazil, Russia, India, China) countries, with revenues falling by 17.8 percent in China and 15.3 percent in India . Among the non-BRIC countries, the annual falls in revenue were highest in Poland (13.3 percent) and France (13.1 percent).

But consumers also are abandoning use of fixed network voice, as well. The total number of fixed lines among the 17 countries fell by four percent to 767 million in 2011. The number of lines fell in all of these countries (except Brazil and the U.K.), where the number of lines increased by two percent and 0.2 percent respectively.

Fixed voice call volumes also fell in all of the countries for which figures were available in 2011, except France.

The logical response, for any executive facing that sort of revenue erosion would be to “cut costs.” The problem is that some service providers already have cut significantly, and some costs cannot be cut, due to pension obligations, union rules, contracts or government edicts.

At some point, no amount of additional cost cutting will compensate for falling revenues. Shutting down the TDM networks won’t necessarily fix the voice revenue problem. But all the future services will require the IP network, so whatever happens to the voice business, IP can provide it at lower cost.

And lower cost now matters, as most voice and even broadband access are migrating to the mobile networks. That means less potential revenue to support even the IP fixed network.

In fact, so fast are mobile high-speed access revenues growing that, for the first time in 2011, overall mobile data revenues exceeded fixed broadband revenue in the 17 countries.

In fact, the salience of mobility is a relatively new form of pressure. The countries where the highest proportion of calls originated on mobiles in 2011 were China (97 percent), the United States (82 percent) and Poland (81 percent), the Ofcom study reports.

As always, the transition discussions and policies will be contentious and highly political, since many contestants stand to lose or gain a great deal, depending on how and when the transition happens.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Philippines Gmessage a Test of Carrier Instant Messaging Success

Globe Telecom, the second biggest carrier in the Philippines, is about to find out how important network effects are for instant messaging users.

Globe Telecom, the second biggest carrier in the Philippines, is about to find out how important network effects are for instant messaging users. Globe Telecom is launching its own instant messaging service, with one key attribute: messages can be sent to people who do not use Gmessage. The new service has tough competition, including Facebook and Whatsapp, for example.

At least in part, Globe Telecom is responding to declining text messaging usage, and growing use of instant messaging platforms as an alternative.

Instant messaging is quite popular in Asia. But the markets remain fragmented. In China, the top instant messaging applications are Imo.im and Chatroulette. Imo.im reaches 3.7 percent of the users with 6.5 percent of all page views and Chatroulette reaches 1.7 percent of the users with 1.3 percent of all page views.

Line, which has grown to 60 million users, mostly in Asia including at least 29 million in Japan.

Also popular is Kakao Talk with 60 million users, more than half in South Korea where it originates.

Other messenging apps include Nimbuzz, which has amassed 100 million users including 31 million in Asia, and WeChat by China-based Tencent, which is nearing 200 million users.

Globe’s Gmessage is potentially significant for a few reasons. Number one is that mobile messaging services are popular in Asia, and that is hurting text messaging revenue.

In South Korea, KakaoTalk has more than 60 million users, and LINE is enjoying similar popularity in Japan. In China, Weixin – or WeChat, in English – has more than 200 million users.

Alongside WhatsApp, all three are intent on expanding in the Southeast Asian markets. So Globe Telecom is fighting back with an offer of its own.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

U.S., Canada are Least Concentrated Broadband Markets

Many observers complain about the dominance of cable companies and telcos in the fixed network high-speed access market, but a new analysis by Ofcom, the United Kingdom communications regulator, suggest the United States and Canada have the least concentrated markets among 13 examined by Ofcom.

Many observers complain about the dominance of cable companies and telcos in the fixed network high-speed access market, but a new analysis by Ofcom, the United Kingdom communications regulator, suggest the United States and Canada have the least concentrated markets among 13 examined by Ofcom.When the combined retail customer market share of the three largest broadband providers in each country is used as a measure of market concentration, and across the 13 countries for which figures are available, the average share of the largest three providers increased from 64.1 percent to 65.2 percent in 2011.

In the five years to 2011 the change in the combined connection share of the three largest providers in each country ranged from a 20.9 percentage point fall in Poland to a 16.2 percentage point increase in Ireland.

The most concentrated broadband market at the end of 2011 was France (where the largest providers (Orange, Free and SFR/Neuf) accounted for 86 percent of connections), followed by Ireland at 85 percent.

Excluding the United States and Canada (where infrastructure-based competition between local incumbent telecoms providers and cable operators makes the share of the largest three operators a less useful measure of competition) the least concentrated broadband market among our comparator countries was in Poland, where the three largest providers’ combined market share was 57 percent.

That structural difference between North American fixed broadband markets, and those of most other countries, where only a single broadband network exists, also suggests why the U.S. Federal Communications Commission is less concerned than regulators elsewhere about mandatory wholesale access obligations and prices.

While it is far from perfect, robust competition between cable operators and telcos provides a workable level of competition without mandatory access obligations and price control.

The other structural consideration is that, in the continental-sized U.S. market, for example, service providers in both cable and telco industries are prevented from becoming too large. Roughly speaking, no single service provider is allowed to gain more than about 30 percent of total market share.

That necessarily means a larger number of significant providers, on a national level. Still, the Ofcom analysis is significant. Using informal tests of market concentration across more than a dozen nations, the U.S. and Canadian markets are the least concentrated.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Demand and Supply are Issues for 1-Gbps Internet Access

It is easy to criticize big Internet access providers for arguing there is little to no demand for symmetrical 1-Gbps high-speed access services of the type Google Fiber is providing in Kansas City, Mo. and Kansas City, Kan. It comes off as an attempt to downplay the significance of a competitor's offering.

At least in part, such statements often are "jawboning" efforts to shape opinion. But there are other legitimate aspects as well. Consumers in some markets who can buy 50 Mbps, 100 Mbps or faster services, often have shown they are willing to buy slower-speed services.

The other practical problem is that the rest of the Internet is not yet optimized for 1-Gbps speeds. Consider a recent test of Internet service provider access speeds for Netflix video streams.

Without question, Google Fiber was the most consistently fast ISP in America for watching Netflix streamed content, according to Netflix.

But keep it in perspective: Netflix streaming only happens so fast, on a 1-Gbps or much slower connections. In other words, a few consumers might want 1-Gbps like they want other products: for "bragging rights."

In practice, a faster access pipe will always be bound by all the other access pipes, servers and backbone transit routes and equipment in between any two connections. Upgrading just one link doesn't actually provide that much value. It simply shifts the bottleneck elsewhere.

At least in part, such statements often are "jawboning" efforts to shape opinion. But there are other legitimate aspects as well. Consumers in some markets who can buy 50 Mbps, 100 Mbps or faster services, often have shown they are willing to buy slower-speed services.

The other practical problem is that the rest of the Internet is not yet optimized for 1-Gbps speeds. Consider a recent test of Internet service provider access speeds for Netflix video streams.

Without question, Google Fiber was the most consistently fast ISP in America for watching Netflix streamed content, according to Netflix.

But keep it in perspective: Netflix streaming only happens so fast, on a 1-Gbps or much slower connections. In other words, a few consumers might want 1-Gbps like they want other products: for "bragging rights."

In practice, a faster access pipe will always be bound by all the other access pipes, servers and backbone transit routes and equipment in between any two connections. Upgrading just one link doesn't actually provide that much value. It simply shifts the bottleneck elsewhere.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

63% of Mobile Video Consumption Happens at Home

Fully 63 percent of digital video screening on mobile phones does not happen on-the-go, but rather at home, a study conducted on behalf of the Interactive Advertising Bureau (IAB) has found.

Fully 63 percent of digital video screening on mobile phones does not happen on-the-go, but rather at home, a study conducted on behalf of the Interactive Advertising Bureau (IAB) has found. Some 36 percent of these home-based digital video activities happen in a room where a second screen also is present (television, PC or tablet), IAB says.

This is perhaps the inkling of a future shift in the mobile video medium.

Initially, the thinking was that people would watch bits of video in "interstitial" time, between other activities, or while waiting at a bus stop, for example. Also, the general thinking was that people would naturally want to use the biggest available screen.

The IAB findings tend to refute the notion that mobile video is something consumers use haphazardly, at odd times of the day, when they have nothing else going on and no other screen available.

That might suggest users have a preference for the mobile experience even when they are stationary and have other screens available, and that a distinct "fourth screen experience" is developing, with potential attributes different from television, PC and tablet video consumption. In fact, use of a phone to watch video when other screens readily are available suggests there is something about mobile viewing that users see as "better" than viewing on a larger screen, for whatever reason.

Mobile video usage also appears to taking on some of the patterns of traditional television consumption, with a "prime time" period in the evening. About 22 percent of video interactions were purposefully planned, while 18 percent of views were "because I was bored" motivations, and only three percent of mobile viewing happened because no other screen was available.

On the other hand, the study also shows that short form content remains the driver for mobile viewing. The most-frequently-viewed genres in mobile video included music videos (45 percent), movie trailers (42 percent), tutorials/How-To's (41 percent) and funny short video clips (37 percent).

Humorous short clips (66 percent) and music videos (52 percent) are the most likely to be shared. And it is that sharing that is shaping up as a distinctive feature of the mobile video experience.

The findings continue to suggest that short form content is best suited to mobile consumption, or at least that is what consumers choose to do, at the moment. Where people are watching (at home), what they are watching (short form content), when they are watching (prime time) and why they are not using a larger screen are relevant observations.

It remains possible that many mobile viewers do not use a larger screen, even when it is available, for some technology reason (TV doesn't have Internet connection), because others are using the other screens at the moment or simply because they prefer the mobile experience.

Nor does the study shed much light on a related, but different issue, namely whether users would choose to view long-form content on a mobile screen when other screens are available, and whether the type of content to be viewed makes a difference. In other words, it is conceivable a single person watching news would choose to view on a tablet, but that same person might prefer to watch a high-definition movie on the biggest screen, especially when it is a shared experience.

The IAB study does not address those other questions.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, December 13, 2012

Consumer "Media" Preferences are Shifting

If, over the last four years, consumers have consistently spent less time with television, radio and print media, while steadily spending more time consuming media on mobile devices, what would that tell you?

True, we haven't yet seen significant shifts in revenue for video entertainment services, and one might argue that advertising revenues related to media consumption have not yet budged much, either.

But, sooner or later, advertising follows audience attention.

True, we haven't yet seen significant shifts in revenue for video entertainment services, and one might argue that advertising revenues related to media consumption have not yet budged much, either.

But, sooner or later, advertising follows audience attention.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...