|

| source: National Broadband Plan |

If U.K. trends in high speed access are an indicator of what is happening in the United States, cable operators are providing a disproportionate share of the fastest connections.

Average telco ADSL speeds were 6.7 Mbps in November 2013 compared to 5.9 Mbps in May 2013, according to Ofcom.

In the U.K. market, the average download speed of residential cable broadband connections was 40.2 Mbps in November 2013 compared to 34.9 Mbps in May 2013, an increase of 5.3Mbps over six months.

But U.K. buyers of 120 Mbps cable access services got peak-time speeds of 108 Mbps.

Buyers of 60 Mbps cable connections got 58.4 Mbps at peak hours. Buyers of 30 Mbps cable access services got peak-hour speeds of 30.2 Mbps.

In other words, cable connections were markedly faster, “on average,” than all-copper connections, and also faster than optical fiber connections, in the United Kingdom.

In November 2013, the average actual download speed over optical access connections in urban areas was 46.8 Mbps, according to Ofcom, the U.K. communications regulator.

So it matters whether one buys a cable TV high speed access service, or a telco fiber connection or a telco all-copper access service.

“We consider the increased take-up of superfast connections to be a key factor driving the increase in average actual speeds across all connections,” Ofcom says. In other words, a disproportionate share of the speed growth comes from connections at the high end.

The issue is whether this also is happening in the U.S. market. The longer term issue is whether the pattern will continue, as Google Fiber enters more markets and telcos including AT&T respond in kind.

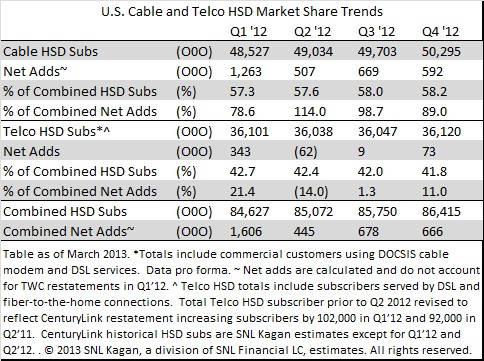

In the United States, cable TV providers of high speed access already have about 58 percent share of the installed base, but also are getting at least 82 percent of the net new additions in that market.

Some might argue cable is getting as much as 100 percent of net new additions.

Already dominant, the cable industry is growing much faster in high speed market share than telcos are growing.

Also at least for the moment, U.S. cable providers have a higher share of the faster access connections. That was not always the case.

In 2004 the mean advertised download peak speeds of cable and telco high speed access services were similar, and the maximum and minimum advertised peak speeds were identical.

By 2009, the average (“mean”) advertised cable speed was about 2.5 times higher than DSL, while the maximum peak advertised speed was three times higher than DSL, though the minimum advertised peak speeds remained identical.

The past is no solid predictor of what might happen in the future, though. Google Fiber is having a dramatic impact on speeds and prices, in some markets, resetting market prices to a level of a gigabit per second symmetrical service for $70 a month.

|

| source: Infinera |

Though Verizon’s major optical access infrastructure is largely completed, AT&T is making new commitments to boost speeds across the board, and spot deploying gigabit access services where it faces Google Fiber.

Still, at the moment, cable seems to have the clear upper hand where it comes to top speeds, in most markets, the exceptions being markets where Google Fiber operates. In areas where Verizon FiOS is available, Verizon might have an edge.

What also is clear is that the strategic value of high speed access for a cable operator arguably is higher than for AT&T and Verizon. Virtually 100 percent of cable TV revenue comes from services provided over the fixed network. That would not change much, even if cable operators launch mobile services using a Wi-Fi-first model.

AT&T and Verizon, on the other hand, earn less than half their total revenue from the fixed network, and almost none of the revenue growth.

That tends to affect supplier thinking about when and where to invest in faster speeds, one might argue. So far, cable arguably has had higher incentives, and enjoyed lower costs, to upgrade access networks.

|

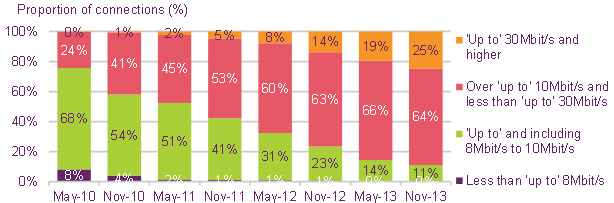

| UK residential broadband connections, by headline speed Source: Ofcom |