Municipally-owned U.S. access or telecommunication networks always have been contentious, for obvious reasons: these are instances where tax-supported non-profit institutions compete with private firms.

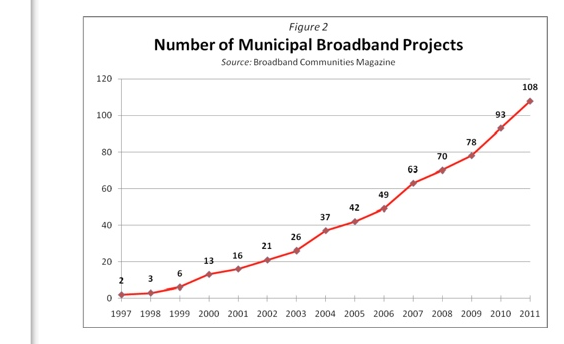

Between 2001 and 2011, the number of such municipal telecommunications initiatives grew from about nine to 108, an order of magnitude expansion in a decade.

Supporters might simply argue that “non-profits” compete with “for-profits” all the time. Museums, hospitals, gas, water and electrical utilities provide examples. Opponents say it is unfair for tax-advantaged entities to compete directly with non-subsidized entities.

The issue is “live” again since Federal Communications Commission Chairman Thomas Wheeler has promised he would stimulate more broadband competition by overriding state laws that presently restrict or ban municipal broadband networks.

The issue remains unsettled, though. Some believe the FCC has no authority to do so, and others think Congress could bar the FCC from taking such action.

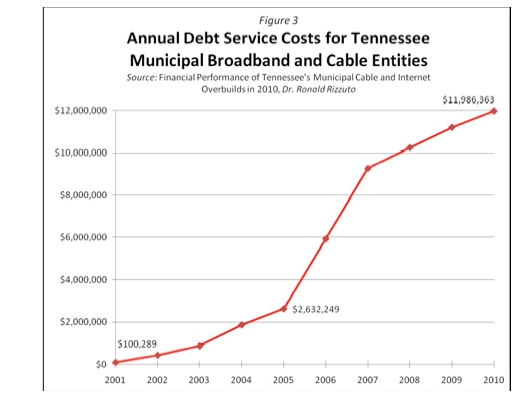

The historical record is mixed: some efforts have succeeded, while others have failed. Even those which have succeeded can leave big debt burdens for taxpayers.

Ignoring the policy issues, the level of risk for gigabit networks has grown, as the risk for fixed networks of all types--private or public--has grown.

There are several reasons. Structurally, markets with multiple competitors inherently mean the cost per customer grows dramatically, increasing risk.

Networks that are built with an expectation of 80 percent to 100 percent customer adoption rates have far lower stranded asset problems than networks where a reasonable assumption is that maximum adoption rates will be in the 30-percent range.

Basically, costs per paying customer are about three times higher in the 30-percent scenario, than in the 100-percent business case. That risk is the same whether the provider is a cable company or telco, a municipal broadband or an upstart ISP, especially if a network must reach all potential customers in a municipality.

Risk is mitigated if suppliers are able to “spot build” only where there is higher demand. That, for example, is why many competitive local exchange carrier operations can survive: they target clusters of business customers, and do not aim for ubiquity.

The triple-play (voice, video entertainment and high speed access) is important for marketing reasons. It also is important for financial reasons. Without the ability to sell three products to a customer, a service provider with 30 percent household adoption would be in grave danger of failure. At 33 percent household adoption, and three products to sell each customer, a service provider mimics the financial results one would expect of a 100-percent take rate for one service.

source: Internet Innovation Alliance