JIn 2008, mobile phone penetration in Myanmar stood at about one percent. Then government officials decided to spur competition by granting new licenses to new operators.

By 2013, adoption had grown to 13 percent, an order of magnitude increase in five years.

The dramatic surge in mobile usage meanwhile was matched by a 10-fold reduction in price.

The price of a subscriber infomation module dropped from $3,000 to about $260. Qatar’s Ooredoo now sells SIM cards for 1,500 kyat ($1.50).

Saturday, August 16, 2014

Myanmar Mobile Usage Grows Order of Magnitude, Prices Drop 10X in 5 Years

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, August 15, 2014

Cable Companies Now are ISPs First, AT&T Might Soon be a Video Provider First

Leichtman Research Group (LRG) says the largest U.S. cable TV operators now have more high speed access customers than they do video customers, according to Bruce Leichtman, LRG president and principal analyst.

And, sometime in 2015, it is possible AT&T will have more fixed network video subscribers than high speed access or voice customers, if its acquisition of DirecTV is approved.

Those two potential facts speak volumes about the new shape of U.S. fixed network communications markets.

The largest U.S. cable TV companies now arguably are Internet service providers with substantial video and voice operations, while AT&T’s fixed networks segment might become a business driven by video entertainment, while it continues to have significant high speed access and voice operations.

In the second quarter of 2014, 17 of the largest cable and telephone providers in the United States, representing about 93 percent of customers in the whole market, acquired nearly 385,000 net additional high-speed Internet subscribers.

Significantly, the top cable companies accounted for 99 percent of the net broadband additions for the quarter, compared to the top telephone companies.

These top broadband providers now account for over 85.9 million subscribers -- with top cable companies having nearly 50.7 million broadband subscribers, and top telephone companies having over 35.2 million subscribers.

For the top cable providers (not including overbuilder WOW), the number of broadband subscribers exceeded the number of cable TV subscribers for the first time ever.

The top cable TV providers had 49,915,000 broadband subscribers at the end of the second quarter of 2014, compared to about 49,910,000 cable TV subscribers.

The top telephone companies added only about 2,000 net broadband subscribers in the second quarter of 2014. In large part, that is because Verizon and AT&T are losing digital subscriber line customers about as fast as they are adding U-verse or FiOS fiber access customers.

AT&T and Verizon added 627,000 FiOS or U-verse subscribers in the second quarter of 2014, with a net loss of 636,000 DSL subscribers,

Broadband Internet

|

Subscribers at End

of 2Q 2014

|

Net Adds in

2Q 2014

|

Cable Companies

| ||

Comcast

|

21,271,000

|

203,000

|

Time Warner*

|

11,965,000

|

86,000

|

Charter

|

4,850,000

|

62,000

|

Cablevision

|

2,779,000

|

(9,000)

|

Suddenlink

|

1,103,300

|

200

|

Mediacom

|

987,000

|

3,000

|

WOW (WideOpenWest)**

|

769,600

|

12,900

|

Cable ONE

|

482,725

|

(1,443)

|

Other Major Private Cable Companies***

|

6,475,000

|

25,000

|

Total Top Cable

|

50,682,625

|

381,657

|

Telephone Companies

| ||

AT&T

|

16,448,000

|

(55,000)

|

Verizon

|

9,077,000

|

46,000

|

CenturyLink

|

6,055,000

|

(2,000)

|

Frontier^

|

1,900,500

|

27,500

|

Windstream

|

1,153,800

|

(16,600)

|

FairPoint

|

333,421

|

1,883

|

Cincinnati Bell

|

270,300

|

300

|

Total Top Telephone Companies

|

35,238,021

|

2,083

|

Total Broadband

|

85,920,646

|

383,740

|

Sources: The Companies and Leichtman Research Group, Inc.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Syracuse Explores Municipal Broadband Network

Syracuse, N.Y. Mayor Stephanie Miner said she is researching the possibility of building a city-owned fiber-optic network to improve access to high-speed Internet service in Syracuse.

Miner said a public network may be the best way to ensure that Syracuse has affordable, high-speed service.

The economics of such a municipal broadband network will be interesting, as it will matter whether Verizon Communications or Time Warner Cable, the current telco and cable TV providers, decide to upgrade their networks beyond 100 Mbps, or possibly up to 1 Gbps, over time.

Assuming Syracuse were to proceed, one might anticipate a reaction by both the other providers.

As always is the case for high speed access markets where there are three leading providers, each of the contestants might reasonably expect to get only about 33 percent take rates, over the long term.

Unless the Syracuse high speed access network contemplates also becoming a linear video subscription provider, that will pose tough payback challenges, as the whole cost of the network will have to be earned back from one service.

Miner said a public network may be the best way to ensure that Syracuse has affordable, high-speed service.

The economics of such a municipal broadband network will be interesting, as it will matter whether Verizon Communications or Time Warner Cable, the current telco and cable TV providers, decide to upgrade their networks beyond 100 Mbps, or possibly up to 1 Gbps, over time.

Assuming Syracuse were to proceed, one might anticipate a reaction by both the other providers.

As always is the case for high speed access markets where there are three leading providers, each of the contestants might reasonably expect to get only about 33 percent take rates, over the long term.

Unless the Syracuse high speed access network contemplates also becoming a linear video subscription provider, that will pose tough payback challenges, as the whole cost of the network will have to be earned back from one service.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

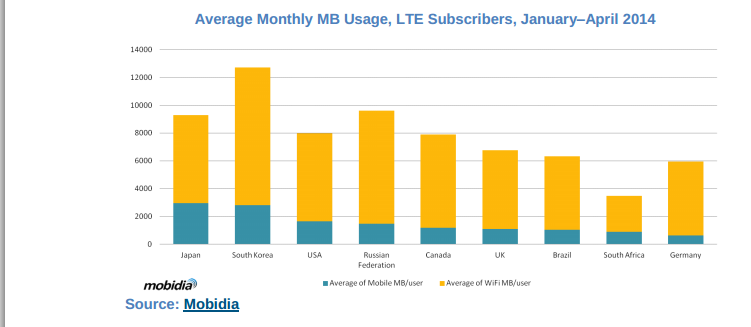

LTE Customers Consume More Data, Still Rely Primarily on Wi-Fi

Observers generally expect that mobile users of Internet access will consume more data on a 4G Long Term Evolution network, compared to a 3G network, and that appears to be the case.

A 2014 Mobidia study found that LTE subscribers consume more data than do customers on 3G networks, but also that Wi-Fi continues to be the primary way most LTE users consume Internet data.

LTE subscribers in Hong Kong, for example, averaged almost 100 percent more data consumption than 3G subscribers in the first four months of 2014.

Other findings from the study are that LTE subscribers in Japan, South Korea and the United States lead the major markets in monthly data usage per subscriber. Subscribers in Japan averaged close to 3GB per month of usage in 2014.

Subscribers in South Korea, meanwhile, averaged over 12GB of mobile data consumed per month when accounting for both cellular and WiFi usage. Subscribers in Japan and Russia averaged slightly less than 10GB of data consumption.

The Mobidia study of Android smartphone and tablet users during the first four months of 2014 in Brazil, Canada, Germany, Hong Kong, Korea, Japan, Russia, South Africa, United Kingdom and the United States

The other issue of interest to mobile service providers is whether LTE access habits also change the way customers use Wi-Fi hotspots, compared to mobile access.

Up to this point, Wi-Fi has been the connectivity of choice among LTE subscribers. According to an earlier study by Mobidia, Wi-Fi accounted for 75 percent to 90 percent of all mobile data consumed in “leading LTE markets” including Canada, Germany, Japan, South Korea, the United Kingdom and the United States.

Across the six markets, average monthly Wi-Fi traffic jumped 36 percent in the eight months between August and March 2013, compared with a one percent increase for mobile access. On average, across the six markets, Wi-Fi accounted for 73 percent of total traffic on Android smartphones in April 2013, up from 67 percent in August 2012.

There is some evidence that faster Long Term Evolution network speeds do convince some users to rely less on Wi-Fi.

Although Wi-Fi accounts for the majority of traffic on both 3G and 4G networks, in August 2012 Wi-Fi took a significantly greater share of traffic on 3G devices than it did on 4G devices, accounting for 69 percent of usage on 3G networks and 60 percent of total traffic on 4G networks.

Mobidia’s findings, on the other hand, contradict findings of survey conducted by EE last year, which suggested LTE availability actually leads users to reduce reliance on Wi-Fi access. The UK’s largest mobile operator said 43 percent of its LTE subscribers are using fewer or no public Wi-Fi hotspots since adopting 4G. EE also found that more and more LTE users were cutting their Wi-Fi usage.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

No Surprise: Amazon Fire Binds Users to Amazon Ecosystem

If you use a Kindle, you'll get the app environment the Amazon Fire represents. The Fire is heavily integrated with Amazon Prime, Apps and Kindle. That's an advantage if that is what you want. But it means the Amazon Fire will not be as useful if what you want is an unbundled experience.

Amazon Fire was designed to make it easy to spend money with Amazon. For example Firefly, an onboard app, scans objects or listens to songs, then finds them in Amazon’s immense retail and digital content so you can buy them.

The Fire’s biggest drawback, at least for Android fans is lack of access to Google app store products.

All that is by design.

Amazon Fire was designed to make it easy to spend money with Amazon. For example Firefly, an onboard app, scans objects or listens to songs, then finds them in Amazon’s immense retail and digital content so you can buy them.

The Fire’s biggest drawback, at least for Android fans is lack of access to Google app store products.

All that is by design.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

TV Always Has been Disruptive to Media Economics

It has been commonplace to note that "a bit is a bit" when thinking about why Internet Protocol has value for end users and app providers, and why IP turns all single-purpose networks into general purpose networks.

In terms of the protocol, it largely is true that a "bit is a bit," allowing any sort of content or communications to use a single network. For users, a bit is never a bit, however.

People don't really buy "bits," they buy function and value. They want to talk, send a text-based message, watch a video, create a document or share a song, video or article.

And there is an expectation about what each of those things "should" cost. People expect to use email without incremental cost. They might expect to pay a little to send and receive text messages or make and receive phone calls.

They have similar expectations about the cost of using a linear video subscription, over the air TV or radio.

And that is where the business model runs into the physics of media. Some high value apps require relatively little in the way of incremental network resources, once the network is built.

Texting, email and voice are prime examples.

Video entertainment is qualitatively different in its impact on networks than voice or messaging, while the price per bit expectations also are qualitatively different.

Assume a fixed network ISP sells a triple-play package for a $130 a month retail price, where each component--voice, Internet access and entertainment video--is priced equally (an implied price of $43 for each component).

By some estimates, where voice might earn 35 cents per megabyte, revenue per Internet app might generate a few cents per megabyte.

A Netflix subscription generates no direct revenue for an Internet access provider, but could represent network consumption of a few gigabytes or more, depending on image quality.

Revenue arguably is zero dollars per gigabyte.

And that’s the problem with video: much of it does not actually represent revenue for the ISP. But even if it does, what is the revenue and cost per gigabyte?

Even if one assume use of one hour of standard definition video, and that product is owned by the ISP, revenue might be $1 to $2 per gigabyte, or small fractions of a penny per megabyte.

“The truth is all bits are not created equal,” says Nicholas Negroponte of the Massichusetts Institute of Technology Media Lab. “And people don’t appreciate that (the cost ot download) a book, a normal novel, is about a megabyte.”

By way of comparison, “a second of video is more than a megabyte.” Beyond that, there is the value of any app or device, such as a heart pacemaker, consuming only small amounts of data.

The value of those bits, and a consumer’s willingness to pay for the value represented by those bits, is highly disparate. “And so to argue that they’re all equal is crazy,” Negroponte says.

That is why video entertainment that shifts from point-to-multipoint networks (broadcast TV, broadcast radio, satellite TV, cable TV or telco TV) to unicast point-to-point is so disruptive, in a business sense.

There is only so much any consumer is willing to pay to watch video. There likewise is a sense of value, compared to price, for making phone calls or sending text messages or web surfing.

The point is that use of IP networks to deliver entertainment video is highly disruptive of media economics. That applies to content owners as well as network service providers.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Thursday, August 14, 2014

AT&T GigaPower Now Live in Dallas, Fort Worth and Surrounding Cities

AT&T has launched gigabit service in the Dallas area, for residents and small businesses in Highland Park and University Park neighborhoods.

Speeds up to 100 Mbps are available in parts of Dallas, Fort Worth and surrounding cities – Allen, Arlington, Euless, Fairview, Granbury, Irving, McKinney, North Richland Hills, Weatherford and Willow Park.

Customers in these areas will be able to upgrade to speeds up to 1 Gbps by the end of 2014, AT&T says.

The 100 Mbps service costs $90 per month, while the 1 Gbps services costs $120 per month, for residential customers, when customers allow AT&T to track user web browsing, for the purpose of personalizing ads.

Speeds up to 100 Mbps are available in parts of Dallas, Fort Worth and surrounding cities – Allen, Arlington, Euless, Fairview, Granbury, Irving, McKinney, North Richland Hills, Weatherford and Willow Park.

Customers in these areas will be able to upgrade to speeds up to 1 Gbps by the end of 2014, AT&T says.

The 100 Mbps service costs $90 per month, while the 1 Gbps services costs $120 per month, for residential customers, when customers allow AT&T to track user web browsing, for the purpose of personalizing ads.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...