Customers who activate a new smartphone or upgrade to a smartphone on a "More Everything" plan from Verizon Wireless will receive an extra gigabyte of shareable data.

Customers must buy a data plan with at least 1GB of data to get the extra gigabyte, and they’ll get that gigabyte each month for two years, as long as the smartphone remains active, Verizon Wireless says.

Verizon Wireless tends not to discount much, as its position in the market is "highest price, but also best network." But not even Verizon can avoid some promotional activity as the U.S. mobile market has gotten more competitive recently, not only because of T-Mobile US attacks, but now also Sprint's long-awaited assault on value-price relationships in the U.S. mobile market.

Tuesday, August 19, 2014

Verizon Gives Extra Free Gig for New or Upgraded Accounts on "More Everything"

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobile Data Speed Gap Between Verizon and Sprint is Shocking

We can debate the significance of consumer satisfaction and network performance rankings conducted on 100-point scales, when scores are very similar. Sometimes, though, scores are not similar.

That appears to be the case for the "speed index" ranking of the four largest U.S. mobile service providers, where the range between the best performance by Verizon, at about 76, is significant, compared to the worst performance, by Sprint, at 54.

On most other measures, though Verizon generally leads, followed closely by AT&T, there is a gap between T-Mobile US and Sprint, according to RootMetrics.

Overall, there still is a sizable gap between Verizon, at about 82, with AT&T at about 80, and T-Mobile US at about 72 and Sprint at 70.

One might argue a 10-point gap in any single market or industry is significant. Customer satisfaction rankings of Verizon and Time Warner video subscription services are a case in point, where there is abou a nine-point gap, on a 100-point scale.

Typically, differences in measured customer satisfaction feature less dynamic range between the best and worst scores. A 20-point gap is virtually unheard of.

All the four national carriers score most evenly in the area of text messaging, where the gap is just a couple of points between high and low. On most other measures, the performance gap between Verizon and AT&T on one hand, and T-Mobile US and Sprint, on the other hand, matches with the market share positions.

At some level, customer experience with Verizon and AT&T seems to correlate with market share held by each of the four carriers.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, August 18, 2014

Canby Telecom Gigabit Service for $20 a Month Increment Over Prior "Fastest Speed" of 60 Mbps

That Canby Telcom, which has been planning to offer 1 Gigabit symmetrical Internet service to its customers in Canby, Oregon, since early 2014, has done so, is not surprising. Perhaps the most interesting angle is how the new top-end gigabit service will lead Canby to readjust prices for slower speed options.

Canby sells stand-alone gigabit access at about $100 a month (10 cents per Mbps), without promotional discounts.

The 60-Mbps offer costs $80 a month ($1.33 per Mbps), without promotional discounts. A 30-Mbps offer costs $60 a month ($2 per Mbps), without promotional discounts. A 10-Mbps service costs $50 a month ($5 per Mbps), without promotional discounts. The most-affordable 5-Mbps plan costs $40 a month ($8 per Mbps).

So the issue really is value. All the plans of 60 Mbps or less offer “per Mbps pricing” between $8 per Mbps to $1.33 per Mbps.

The gigabit access plan offers each Mbps at about 10 cents, or two orders of magnitude less, per Mbps.

You might argue that consumers will pay only so much for Internet access, as they only will pay so much for video entertainment or voice.

But those consumer value propositions have changed over the years. Once upon a time, consumers would willingly pay about $20 a month for a dial-up service at 56 kbps, an implied per-Mbps price of about $357 or so.

Clearly, the absolute price mattered more than any esoteric “per-Mbps” considerations, and many would argue that will remain the issue, even when gigabit services are offered.

The issue will come at the margin, where a buyer of the $60 a month or $80 a month plans evaluates the value of a $100 a month plan what offers 17 times the speed for a price difference for a price about 25 percent percent higher, or 33 times the speed for a price delta of about 60 percent.

One might argue a single-user household will be hard to convince. But a multi-uer household, especially where there is lots of video streaming going on, with significant work at home happening, is quite another matter.

In that case, even a price increase of 60 percent, to gain 33 times the speed, might be quite attractive.

Canby had begun installing fiber to the home backhaul facilities in 2008 and began installation of drops in 2009.

By the end of 2009, Canby Telcom had wired about 1,000 homes.

By about 2010, the new Fiber Optic Zone (FOz) service offered three speed tiers, the lowest operating at 20/10 Mbps; the intermediate tier running at 40/20 Mbps; and the fastest tier offering 60/30 Mbps.

Canby Telcom provides information, communication and entertainment services to more than 7,000 customers over an 84-square-mile foot print in the northern Willamette Valley of Oregon.

Canby Telcom will be able to offer gigabit services to more than 2,500 local residents and businesses already wired with fiber to the home.

Speed

|

Monthly Pricing

|

5 Mbps

|

Everyday Price: $39.95

Special Offer:

$19.95 / month

|

10 Mbps

|

Everyday Price: $49.95

Special Offer:

$24.95 / month

|

30 Mbps

|

Everyday Price: $59.95

Special Offer:

$29.95 / month

|

FOz 60 Mbps

|

Everyday Price: $79.95

Special Offer:

$39.95 / month

|

FOz 1 Gbps

|

Everyday Price: $99.95

Special Offer:

$49.95 / month

|

The point is that the advent of gigabit services will eventually cause an adjustment of user expectations of what a reasonable value-price offer is for high speed access, with the greatest discontinuity at the top of historic ranges, where a $20 monthly price difference provides 17 times the bandwidth.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

"Unified Communications" Has Become a Fuzzy Concept

“Unified communications” has been an evolving issue for business and consumer users for some time, as the number of devices and media types has grown from the original “phone messages” to include email, text, social and other content and information types; PCs, tablets and smartphones.

Project Cascade represents one more way that “unified communications” might provide value in a consumer context, but also an illustration of how imprecise “unified communications” has become, as a category.

Beyond phone numbers, email addresses or social identities, there are growing needs to extend a single identity to multiple devices, if not to merge identities of various types on a number of devices.

Cloud apps, which eliminate the need for active synchronization, play a part. So do various unified communications systems, devices and apps.

AT&T's Foundry innovation center also is working on Project Cascade, which links AT&T voice and messaging services to any secondary device.

As new classes of devices get connected to the AT&T network, Cascade will allow users to access their AT&T services seamlessly across their personal network of devices.

At first, Cascade will allow users to send and receive calls and messages from any of your devices, including wearables and connected cars, without Bluetooth pairing.

In principle, shared identity and access for voice and messaging is only the first step towards making new and existing services available to any device seamlessly.

That might primarily be seen as a development of primary value to consumer end users. But that also is part of a trend, where many consumer apps perform functions once associated with business phone systems.

That is one reason why the term “collaboration” has joined “unified communications” as a term of art. “Collaboration” speaks directly to people engaged in common work-related tasks.

“Unified communications” might apply to any number of apps and features provided by communication or social apps, devices and access services. That is one reason why many observers essentially lump IP telephony and unified communications into a single category.

Project Cascade represents one more way that “unified communications” might provide value in a consumer context, but also an illustration of how imprecise “unified communications” has become, as a category.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, August 17, 2014

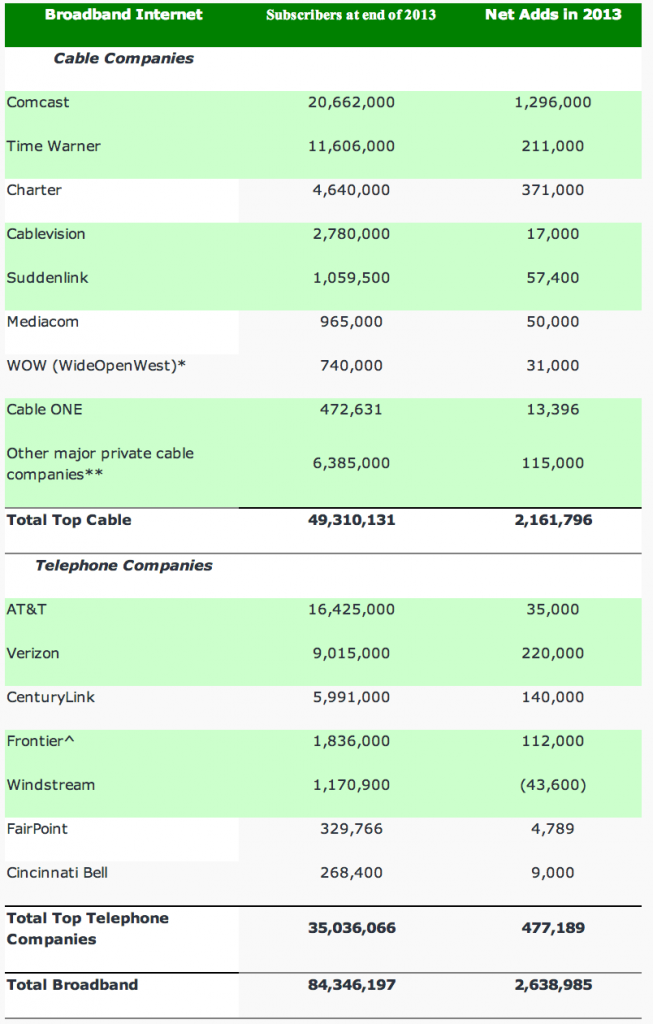

Suddenlink Illustrates Trends for MId-Sized Independent Telcos, Cable Companies

Suddenlink’s second quarter results illustrate several trends in the U.S. largely-rural fixed network service provider market. Revenue growth is lead by high speed access services, not legacy services.

The core product now is a bundle. Bundled residential customers represented 66 percent of total residential customer relationships at June 30, 2014, an increase from 65 percent at June 30, 2013.

Though representing 28 percent of total residential customer relationships at June 30, 2014, versus 26 percent at June 30, 2013, the triple play package of video entertainment, high speed access and voice represents the growth trajectory at Suddenlink.

In a saturated and competitive market, Suddenlink is unlikely to add too many customers based on organic growth. Instead, it largely will have to increase the number of services purchased by each customer.

Second quarter revenues of $579.9 million grew six percent compared to the second quarter of the prior year, highlighted by high speed Internet revenue growth of 15 percent.

High-speed Internet service revenues rose 15 percent, while telephone service revenues grew one percent. And the business context has changed. With the advent of 1-Gbps services, Suddenlink believes it has to compete.

Suddenlink Chairman and CEO Jerry Kent said Suddenlink “will enable one-gigabit speeds” to “retain our competitive advantage in Internet services."

Total residential customer relationships were 1,403,500 at June 30, 2014, an increase of 29,600, or 2.2 percent, from June 30, 2013.

Including commercial services, primary service units (one sale of a high speed access, voice or video service) were 2,903,600, an increase of 110,500, or four percent, over the prior year.

Including commercial services, revenue generating units were 3,785,100, an increase of 145,000, or four percent, from June 30, 2013.

Total average monthly revenue per basic video customer for the second quarter was $163.92, an increase of nine percent compared to the second quarter of the prior year. And that tells the story: revenue per account is growing faster than the number of new accounts.

As is the case for a few of the larger rural telcos or cable companies, commercial revenue (sales to business customers) is an important new revenue source. Commercial revenue grew 11 percent compared to the second quarter 2013, including 18 percent year-over-year growth in commercial high-speed data, telephone and on-net carrier revenue.

Commercial revenue totaled $81.8 million, or 14 percent of total revenue, in the second quarter 2014, representing growth of 11 percent compared to the second quarter 2013.

At June 30, 2014, Suddenlink served approximately 1.4 million residential customers, and Suddenlink`s RGUs were comprised of 1,168,800 basic video, 881,500 digital video, (about two million video units) 1,103,300 residential high-speed Internet, and 534,600 residential telephone customers.

The video business, in terms of units sold, is twice as big as high speed Internet, which in turn is twice as big as the voice business. That is a different profile from the largest U.S. cable companies, where high speed access, in terms of revenue, is as big as the video business.

Approximately 66 percent of Suddenlink`s residential customers subscribe to bundled services, compared to 65 percent a year ago.

Approximately 391,400 of Suddenlink`s residential customers receive video, high-speed Internet, and telephone services as part of a triple play bundle, representing 28 percent of Suddenlink`s total residential customer relationships.

Non-video residential customers of approximately 319,900 at June 30, 2014, represent 23 percent of total residential customer relationships, and grew 20 percent.

Suddenlink`s average revenue per user for the second quarter 2014 was $163.92, an increase of nine percent compared to the second quarter 2013.

Basic video customers decreased by approximately 18,700 customers during the second quarter of 2014, an improvement compared to a loss of 23,100 basic video customers in the second quarter of 2013.

Digital video customers decreased by approximately 6,500 customers during the second quarter of 2014, an improvement compared to a loss of 8,200 digital video customers in the second quarter of 2013.

Residential high-speed Internet customers increased by approximately 200 during the second quarter 2014, an improvement compared to a loss of 8,700 residential high-speed Internet customers in the second quarter of 2013.

At June 30, 2014, estimated residential high-speed Internet penetration was 36 percent of high-speed Internet capable homes passed.

During the second quarter of 2014, commercial high-speed data customers increased by approximately 1,500. These commercial customers are not included in total RGU counts.

Including these commercial customers, high-speed Internet customers increased 83,800, or eight percent, over the prior year.

Residential telephone customers grew by approximately 7,100 during the second quarter 2014, and 46,900, or 10 percent, during the trailing twelve months.

At June 30, 2014, estimated residential telephone penetration was 21 percent of telephone capable homes passed. During the second quarter of 2014, commercial telephone customers increased by approximately 2,200 customers, and increased by approximately 8,100 over the trailing twelve months, or 29 percent.

These commercial customers purchase 2.8 lines on average and are not included in total RGU counts. Including these commercial customers, our telephone customers increased 55,000, or 11 percent, over the prior year.

Suddenlink operates primarily in rural markets, and is the seventh largest cable operator in the United States.

That makes the company somewhat analogous to Windstream and Frontier Communications, in terms of high speed access markets and customers, or Mediacom and Charter Communications, in terms or video customers and markets.

Suddenlink’s networks pass 3.1 million homes in the United States as of June 30, 2014. Suddenlink serves approximately 1.4 million customers as of June 30, 2014.

The Company's customer base is clustered geographically with approximately 96 percent of its customers located in the ten states of Texas, West Virginia, Louisiana, Arkansas, North Carolina, Oklahoma, Arizona, California, Missouri and Ohio, with 91 percent of customers located within the top 20 primary systems.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, August 16, 2014

Virtual SIMs Could Rapidly Increase Mobile Usage

Movirtu "Virtual SIM" platform enables multiple phone numbers to be active on a single standard subscriber information module, allowing multiple users to use one physical device without the need to manually change the SIM card.

The obvious upside is that using a virtual SIM could allow many more people to use mobile phone service, more affordably.

To use a virtual SIM, a subscriber borrows a phone and enters a short code that tells the network that the phone is now using another number.

The subscriber then can make and receive calls from his own number(at his own expense) on the borrowed phone.

All that’s changed is an entry in the mobile network’s visitor location register.

To return the phone, the subscriber must enter the code again, and all is back to normal, a process akin to logging onto your own email account on a friend's computer.

Likewise, CloudPhone allows non-phone devices to be used as mobile network connected devices. Movirtu CloudPhone allows mobile operators to extend the reach of mobile services to non-SIM devices such as tablets that might have Wi-Fi-only connections.

The obvious upside is that using a virtual SIM could allow many more people to use mobile phone service, more affordably.

To use a virtual SIM, a subscriber borrows a phone and enters a short code that tells the network that the phone is now using another number.

The subscriber then can make and receive calls from his own number(at his own expense) on the borrowed phone.

All that’s changed is an entry in the mobile network’s visitor location register.

To return the phone, the subscriber must enter the code again, and all is back to normal, a process akin to logging onto your own email account on a friend's computer.

Likewise, CloudPhone allows non-phone devices to be used as mobile network connected devices. Movirtu CloudPhone allows mobile operators to extend the reach of mobile services to non-SIM devices such as tablets that might have Wi-Fi-only connections.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tata Docomo Offers Sponsored WhatsApp Access in Mumbai

Tata Docomo in India now offers unlimited and sponsored usage of WhatsApp on some postpaid plans offered to customers in Mumbai.

Separately, Tata Docomo also offers separate plans with access to YouTube at discounted rates. Data plans for the “YouTube Recharge” cost half that of regular data access.

Both types of packages are examples of sponsored access, where an Internet service provider makes available one particular app at no incremental charge, or prices mobile Internet access in ways that offer huge discounts for use of a particular application.

Those examples, one might well argue, show the downside of efforts to constrain the ways ISPs enable Internet access for customers. “Equal treatment of apps,” the way network neutrality supporters now describe efforts to restrict consumer Internet access to “best effort only” modes, also prevents ISPs from providing value to potential users.

The sponsored data approach makes a few highly-popular apps available, either at no incremental cost or for highly-discounted prices, to encourage use of mobile Internet access.

In many countries, network neutrality therefore is an anti-consumer move that limits widespread access to the most-popular apps, and therefore also slows wider adoption of the Internet overall, as people who can see the value of one app likely will come to see the value of other apps.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...