Arbitrage, the exploitation of price gaps between products in markets, or prices between markets, always has been an important strategy in the telecommunications market.

One might argue that VoIP represented Internet arbitrage of the public switched telephone network.

Some free conference calling services likewise are built on arbitrate of access prices in some rural U.S. areas.

And though it is possible to argue that price arbitrate is not sustainable over the long term, it can be an important underpinning of business strategy, at least in the short term, allowing competitors to get a foothold in a market before transitioning to a more-sustainable model.

That, in fact, was the hope some held for local exchange carriers allowed to compete for the first time in the U.S. local telephone business as a result of the Telecommunications Act of 1996.

The thinking was that competitors would rapidly enter markets using resold connections, but then transition to facilities-based networks. For the most part, it did not work out that way, as it was the facilities-based cable TV operators that were able to build sustainable businesses, once wholesale tariffs were raised.

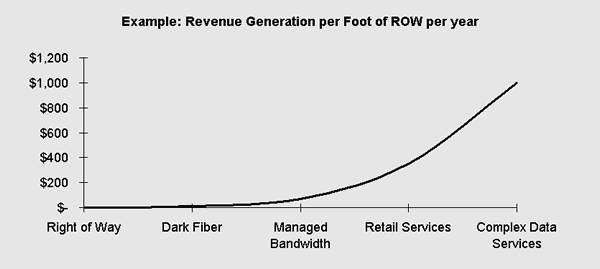

Something similar tends to happen in the wholesale capacity business as well, where most suppliers refuse to sell dark fiber, preferring the high gross revenue and profit margin of selling “lit” services.

But there almost always is customer demand for dark fiber, despite the general reluctance to sell the product. In some markets, the opportunity for arbitrage might not be so great, some argue.

“At some point, the cost of leased capacity and dark fiber is the same,” says Rozaimy Rahman, Telekom Malaysia EVP. That probably refers to total cost of ownership. But the point about arbitrage remains.

Some large enterprises, and certainly many carriers, will conclude that, at least in some instances, they will operate at lower costs when they are able to buy dark fiber and turn up their own networks.

By refusing to sell dark fiber, service providers might be creating a market opportunity for suppliers willing to do so.

In the long run, Rahman is likely correct: total cost of ownership, for an end user, might over the long term be nearly equivalent, for leased capacity or dark fiber approaches.

But arbitrage works because there are exploitable price differences in the short term. And Rahman is correct: the difference between dark fiber and managed bandwidth services, has at times past, n some markets, not been so great.