The state of the global telecommunications business, even the U.S. telecom market, or any of the industry segments, is hard to explain in a single number, or even a time series.

At one level, it is easy to point to continual growth. In fact, it would be hard to find a single year where aggregate revenue failed to grow, globally or in any single country.

But what that growth means for various providers, and different product segments, often is a different matter altogether.

U.S. Telecommunications Revenue

The top line paints one picture.

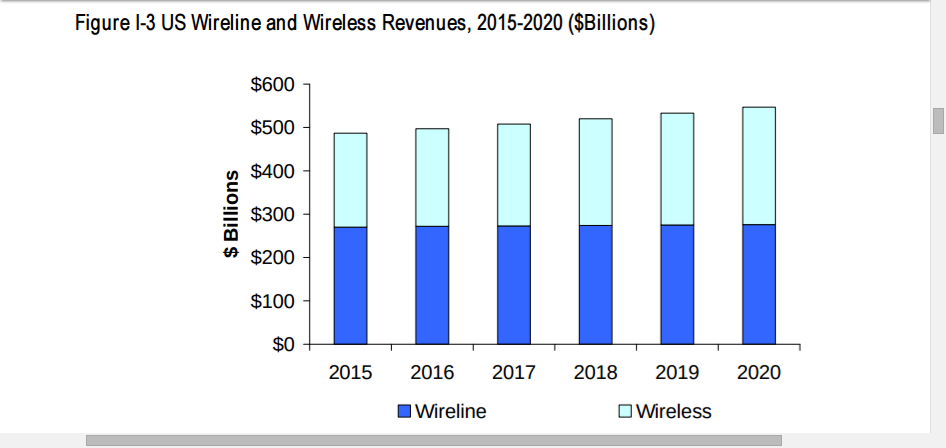

From 2015 to 2020, U.S. wireline revenue will grow from $270 billion to $276 billion, at a compound annual growth rate of 0.4 percent, while U.S. mobile revenue will grow from $217 billion to $271 billion at a CAGR of 4.5 percent, according to Insight Research Corp.

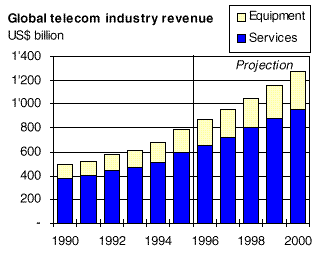

Globally, communications revenue is projected to grow from $2.2 trillion to $2.4 trillion at a compounded annual growth rate of 2.3 percent from 2015 through 2020, Insight Research Corp. estimates.

The detail might tell a very different story.

In 2002, the U.S. telecommunications industry’s gross revenues were $385 billion (including cable and satellite TV), and its net revenues (after interconnection costs, program content, and handset subsidies) were $315 billion.

By 2013, even while consumer revenues grew, aggregate business segment revenues fell at least 15 percent.

And that understates the changes. Fixed network revenue fell by half. All the net revenue growth came from mobility or linear video services.

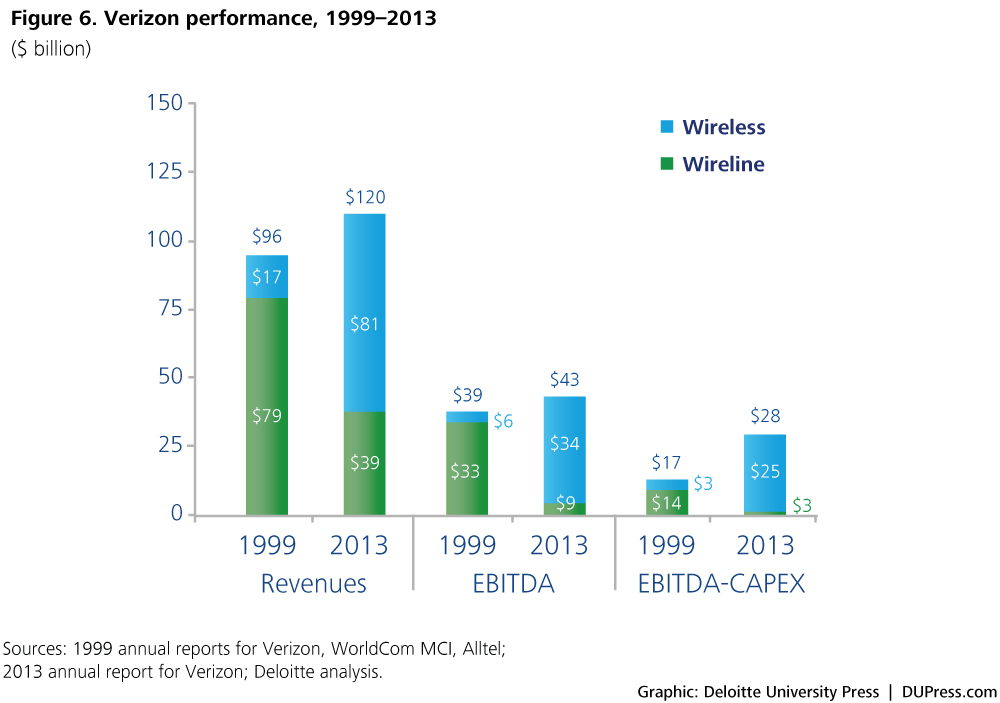

More significantly, where 85 percent of total Verizon earnings were driven by the fixed network, by 2013 the fixed network represented just 21 percent of earnings.

From 2015 to 2020, fixed network revenue will grow from $1.0 trillion to $1.1 trillion at a CAGR of 0.8 percent, while mobile revenue will grow from $1.1 trillion to $1.4 trillion at a CAGR of 3.5 percent.

Mobile revenues passed fixed network revenues a few years ago and by 2020 mobile revenue will be 25 percent higher than fixed revenue, according to Insight Research.

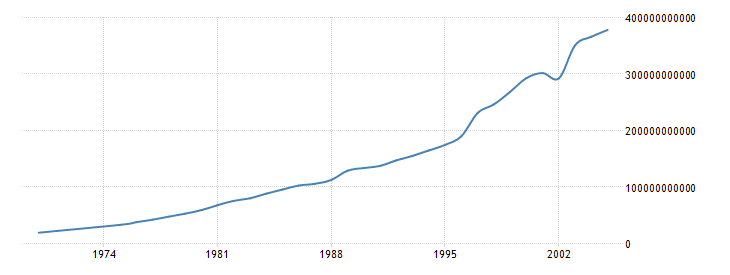

source: Global Telecommunications, International Telecommunications Union

source: Insight Research Corp.

source: Insight Research Corp.

The point is that gross revenue alone does not tell you what is happening with product demand or profitability.

International long distance, fixed voice, and now mobile voice and messaging, have suffered. High speed access, Ethernet access, cloud computing and mobile data have benefited.

Cable TV operators make more money, but many competitive providers make less, or are out of business.

New contestants, such as Google Fiber, Comcast and independent Internet service providers are demonstrating that facilities-based competition is more feasible than once believed.

So “total revenue” does not tell the story of what is happening “inside” the communications business, even at the level of access revenues, to say nothing of how application markets are changing.