| source: Telco 2.0 |

Looking only at markets in the United States, Canada, France, Germany, Spain, UK, Italy, Singapore and Taiwan, researchers at STL Partners have estimated core revenue losses of 25 percent to 46 percent between 2012 and 2018, potentially.

In other words, to stay where they already are, in terms of revenue, service providers will need to create between 25 percent and 46 percent more new revenue over the six-year period. Big acquisitions are almost certain to be part of the answer.

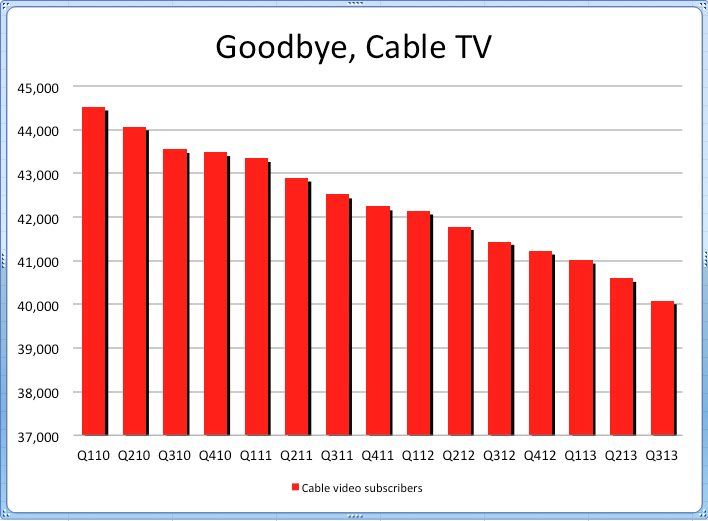

AT&T’s acquisition of DirecTV, for example, instantly made AT&T one of the biggest providers of video entertainment in the U.S. market, and changed its revenue profile by about $7 billion per quarter, or potentially $30 billion annually.

It would have been virtually impossible to add that much revenue, so fast, by any organic means.

In similar fashion, Verizon spent $130 billion to buy the minority stake in Verizon Wireless owned by Vodafone, boosting annual revenue by about $22 billion.

Still, even that will not be enough, long term. Voice, messaging and linear entertainment video already are flat or declining.

Eventually even Internet access revenues will stall, then decline, at some point. Long term, big new revenue sources must be found.