Tuesday, February 7, 2017

Cloud Data Centers Now Originate, Terminate Traffic

Among the many changes happening in the global communications industry are changing patterns of traffic origination and termination. It has been some time since central offices originated and terminated most traffic. For some decades, internet exchange points were the places where traffic moved to, and from.

Now it is starting to be the cloud data centers that originate and terminate most traffic.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

How Artificial Intelligence is Relevant for a Mobile Apps Company

Charles Fan, Cheetah Mobile CTO, has a marvelous ability to take somewhat abstract ideas and make them concrete. You might wonder, for example, why a mobile apps firm actually thinks about how artificial intelligence and machine learning affects its business.

The immediate application for Cheetah is a news curation app. But Fan thinks artificial intelligence algorithms, which might today seem to represent value, eventually will be commoditized. When that happens, value will no longer be conferred by access to the algorithms, but to owners of content stores.

In other words, he wins who has the best data stores. That will be a change from today, when perhaps value is generated by firms able to hire "hundreds of PhDs." In the future, that will not confer value, Fan argues.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Managed Wi-Fi Service: How Big an Opportunity?

Consumer interest in managed Wi-Fi services represents a $6.7 billion missed opportunity for service providers globally, a new study from XCellAir suggests. That includes up to $3.3 billion in incremental revenue, as well as $3.4 billion in lower operating costs (fewer customer service interactions and truck rolls).

Data from a new survey of 1,000 consumers each in the United States and United Kingdom reveals that on average, 15 percent of consumers say they would be willing to pay for managed Wi-Fi service from their service provider or a third party, and are willing to pay $34 per year for such managed services.

Presumably, the main problem consumers experience is “coverage.”

The XCellAir Home Wi-Fi Advisor service for ISPs has in the past found that the average household typically is a single family of three people, with 14 internet connected devices.

The average home has two floors, with the majority keeping their primary Wi-Fi router on the first or ground floor.

While the average Wi-Fi speed need for a household is 23 Mbps, the peak speed needed to support all devices within the home is 40 Mbps.

Taking into consideration the number of people, devices, and size of home, the average household requires 2.6 access points in order to have complete Wi-Fi coverage throughout the home, XCellAir argues. So, presumably, the big advantage of a managed service is placing and monitoring the performance of multiple Wi-Fi base stations or repeaters.

As Wi-Fi suppliers increasingly market systems capable of such management, on their own, it is not so clear that the service opportunity is so much the solution as the diagnosis.

The consumer study, carried out in December 2016, found that 50 percent of consumers blame their internet service provider for problems with their Wi-Fi, regardless of who provided their router.

Despite 18 percent of consumers blaming their Wi-Fi equipment when service falters, as many as 39 percent of consumers would still call their ISP to assist with troubleshooting faults or problems.

The survey also revealed that as many as 89 percent of consumers have completely unmanaged Wi-Fi, yet there is notable appetite for managed and paid-for services from their ISP or other third party.

Some 80 percent of consumers surveyed experienced at least some issues with their Wi-Fi, with 31 percent experiencing occasional or frequent Wi-Fi problems.

As many as 19 percent of users in the United States, and 10 percent of respondents in the United Kingdom, said they were willing to pay their service provider or a third party technical services firm, such as Geek Squad or Knowhow, to manage their Wi-Fi for them.

The mean (arithmetic average) fee per month that consumers are willing to pay for managed Wi-Fi in the US was nearly $4 per month, with six percent indicating they were willing to pay as much as $15 or more. In the United Kingdom, the mean fee was £1.49, with six percent willing to pay up to £4 per month.

Some 74 percent of consumers get their Wi-Fi equipment from an ISP.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

3 or 4 for U.S. Mobile Market? Answer Might Still be "4"

The optimal mobile market structure for any national mobile market remains an open question. Some believe most markets balance consumer welfare and supplier sustainability better with three leading suppliers rather than four, but regulators in many markets continue to believe that four suppliers are necessary for robust competition.

Indeed, most financial analysts likely agree that three suppliers in the U.S. market, for example, would be better for suppliers. Were T-Mobile US and Sprint to combine, three roughly-equal firms would lead the market.

Under that structure, the fierce pricing wars would abate, many believe, while allowing Sprint and T-Mobile US to attain better scale economics. At the same time, many believe, AT&T and Verizon revenues and profits also would improve.

Of course, all such assumptions are just that: assumptions. What has to be considered is that Comcast and Charter Communications also are entering the market. So no matter what happens with mobile service provider consolidation, at least two potentially-powerful new contestants will be entering the market.

Some believe regulators and antitrust officials will have key problems with market share, were Sprint and T-Mobile to try a merger, as they have in the past concluded. Though many believe it will be easier to gain approval under the new administration, the international tests of market concentration are what they are, and antitrust officials still will be using those tools.

In fact, a horizontal merger might not even wind up being the key transaction to be weighed. Vertical mergers or acquisitions (cable plus mobile, for example) are equally likely.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Three Buys UK Broadband for Spectrum Rights

When does it make sense to spend £250 million (US$310 million)--$2,067 per account--to acquire 15,000 money-losing mobile subscribers? When the acquisition also comes with spectrum rights.

UK Broadband is the UK's largest commercial holder of national radio spectrum suitable for 4G mobile services and fixed wireless solutions. UK Broadband has rights to use 124 MHz of spectrum in international LTE bands 42 and 43 (3.GHz and 3.6GHz), as well as additional spectrum suitable for high-capacity point-to-point and point-to-multipoint services in the 3.9GHz, 28 GHz and 40 GHz bands.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Nobody Yet "Knows" How IoT Will Create Value

In the early days of any potentially-revolutionary technology, even the most-experienced industry executives might be nearly clueless about the eventual impact. That is worth keeping in mind as internet of things, artificial intelligence and machine learning are applied to a wide range of industries and processes. Right now, we cannot predict the outcome. In most cases, we are not even sure about the strategies that produce the best outcomes.

In the past, executives have disparaged demand for telephones, alternating current, automobiles, television, audio systems, satellites, mobile phones, video on demand or iPhones.

Bill Gates, when he was CEO of Microsoft, missed the importance of the internet. IBM executives once believed the global market for computers was less than a half dozen.

The CEO of DEC believed nobody would want a computer in their home. Gates once believed nobody would need, or use, a 32-bit computing system.

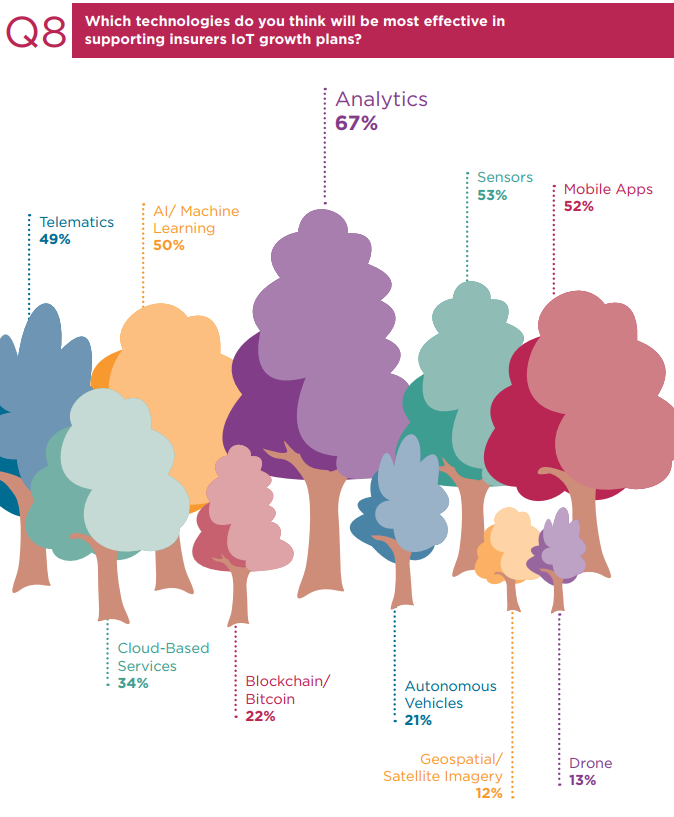

An overwhelming percentage of insurance industry executives believe the internet of things will “revolutionize” the business. They just do not know precisely “how” that will happen.

Those executives believe IoT will allow better risk-based pricing and will change customer behavior in ways that benefit the industry. But it also is fair to note that executives are at such an early stage of IoT application that strategies have not been developed.

At the moment, most seem to believe that better analytics will produce benefits.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, February 6, 2017

Low Power Wide Area Netwoks Using Unlicensed and Licensed Spectrum Will Support 1.4 Billion IoT Devices by 2022

One more sign of the growing role played by unlicensed technologies in “public communications” is the expected use of unlicensed spectrum to support Low Power Wide Area (LPWA) services.

Such LPWA services will play a large part in supporting 1.4 billion Internet of Things (IoT) connections by 2022, according to Machina Research, even as NB-IoT and LTE-M, using licensed spectrum, also contribute.

The GSMA’s Mobile IoT Initiative, which promotes adoption of LPWA technologies, is currently backed by 67 global mobile operators, device makers, chipset, module and infrastructure companies worldwide, GSMA says.

LPWA networks are an emerging, high-growth area of the IoT, designed to support M2M applications that have low data rates, require long battery lives and operate unattended for long periods of time, often in remote locations. They will be used for a wide variety of applications such as industrial asset tracking, safety monitoring, water and gas metering, smart grids, city parking, vending machines and city lighting.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...