The internet’s future, many believe, is intimately bound up with artificial intelligence, used in various forms. But AI already is a practical tool, used by Google to support its advertising operations.

Author Patrick Tucker argues that “when the cost of collecting information on virtually every interaction falls to zero,” insights gleaned from activity will transform those interactions. AI will be the enabler, allowing the sifting of huge amounts of data to glean insights and patterns.

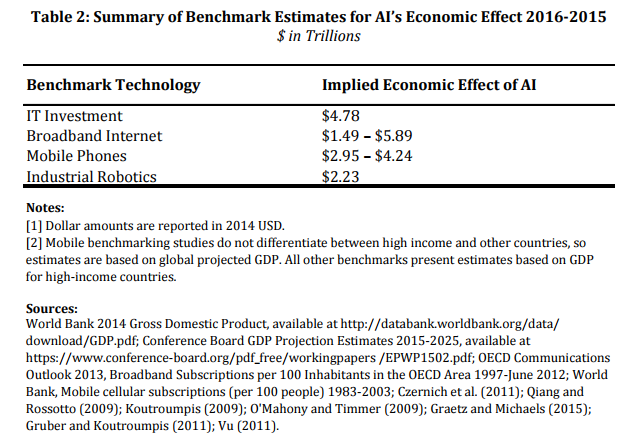

To assess what the economic impact might be, some analysts compare AI to other innovations such as computing advances, internet access, mobility and industrial robotics. That is not to say AI will produce value in these stated industries in equivalent volumes, only to note that big and important innovations have produced estimated benefit in about such volumes.

What is telling, though, is the importance content as assumed in the internet apps space as well as the internet access business.

“It is increasingly clear to us that content is the driver for future growth and AI is a core enabler to connect our user with highly personalized content,” said Fu Sheng, Cheetah Mobile CEO. Though Cheetah Mobile made its mark as a supplier of mobile utility apps, it now sees content services as its growth driver. “Looking forward, we remain both focused in implementing our mobile content strategy, leveraging the big data generated by a massive user base and AI technology to connect our user with more personalized leisure content.”

In fact, Cheetah Mobile sees artificial intelligence being “a very core technology” for content, he said.

“There is a lot of commonality between robotics, especially in deep learning and AI that may have common applications for what we want to do on the Internet space.”