You would expect an organization such as GSMA to argue that “5G is more than just a generational step; it represents a fundamental transformation of the role that mobile technology plays in society.”

But it is not in any way incorrect for GSMA to argue that 5G “is an opportunity for operators to move beyond connectivity.” In other words, one big attraction of 5G is that presents a new way for mobile operators to “move up the stack” in terms of role within the ecosystem.

Specifically, 5G--built to support pervasive computing--”will mark an inflection point in the future of communications, bringing instantaneous high-powered connectivity to billions of devices” and “enable machines to communicate without human intervention,” says GSMA.

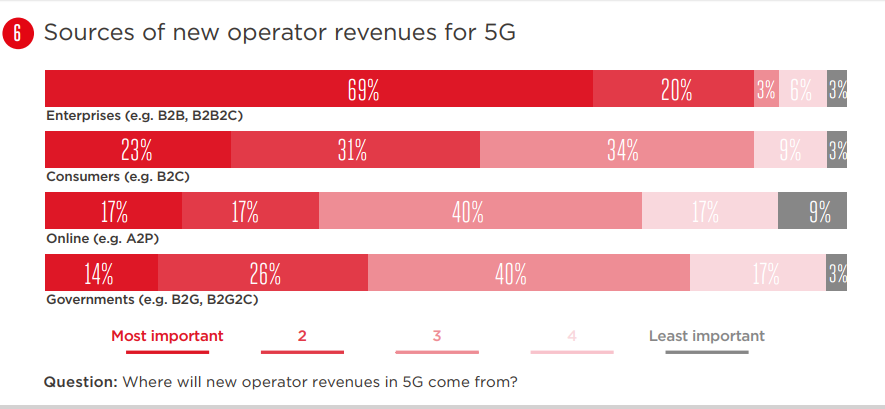

That is important. To the extent 5G actually enables service providers to move up the stack and occupy new and additional roles within the ecosystem, it will be by enabling new use cases, business models and revenue streams principally driven by enterprise customers not consumers.

That is among the big potential changes 5G will bring. To be sure, 5G is expected to enable new uses for the mobile network in supporting consumer internet access, including substitution for fixed network connections.

But the dramatic change is expected to come from revenues generated by enterprises, which will deploy most of the new pervasive computing services, apps and business models.

If 5G develops as most expect (we cannot be sure of that), there will be some historic differences: new revenue sources will be driven by enterprise customers and applications involving machines (pervasive computing).

{kind=link}