With the caveat that much could, and will, happen as the subscription video business switches to an over the top model, it already is possible to predict that as much as half of current subscription revenues could be lost over a decade.

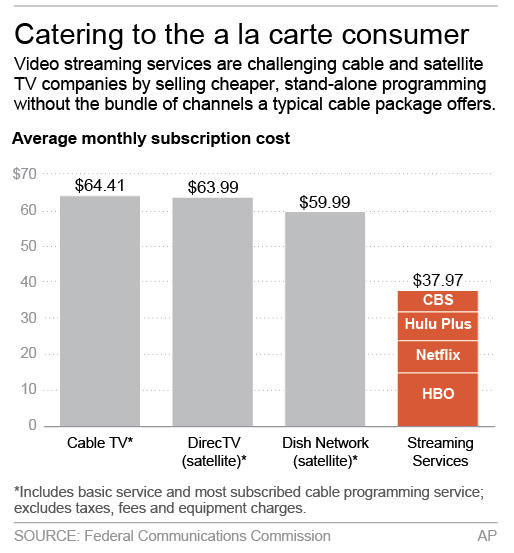

Already, consumers can spend 40 percent less, using a bundle of OTT services, compared to a standard linear video subscription, according to Federal Communications Commission data.

Those fees likely do not include the add ons (taxes, fees, box rentals, outlet charges) that increase an average bill closer to $103 a month.

Indeed, much of the total cost of a video subscription comes from regulatory fees, taxes and rental charges for equipment a consumer does not need when using a streaming, over the top approach. All of that can easily add up to as much as 30 percent of the total monthly bill, beyond the advertised subscription cost.

OTT streaming does not require rental of one or more cable TV decoders ($10 each, per month), additional outlets ($10 each, per month) and a number of regulatory fees not charged for OTT services.

The point is that it is not a rhetorical statement to argue that as much as half of all current subscription video revenue will disappear over the next decade. In fact, we could get close to a fall of 50 percent if consumers simply no longer needed to rental decoders and pay for additional outlets.

Since OTT relies solely on the internet access connection, and uses Wi-Fi for internal signal distribution, there is no outlet charge or requirement; not need for decoders or the regulatory fees.

That alone would drop gross revenue for subscription video 20 percent to 30 percent. So why bother with entertainment video, if a firm is a telco? Even at 50 percent of current revenues, subscription video still produces scores of billions of annual consumer account revenue, in the U.S. market.

Consider how hard it is to create a brand new, billion dollar a year revenue stream any other way. It is worth it, especially as voice and messaging clearly are headed for a 50-percent reduction as well.