Some 37.2 million U.S. households will buy only internet access, and drop subscription TV services by 2022, according to Kagan Research, a media research group owned by S&P Global Market Intelligence. Some 19 million U.S. households already are broadband-only, the firm says.

By 2022, about 38.4 percent of cable or telco households buying internet access will rely mostly on a combination of broadband and over-the-air broadcast signals for home video entertainment, Kagan Research estimates.

Kagan expects broadband-only homes will grow at a 14.4 percent compound annual growth rate from 2017 to 2022, representing about 29 percent of U.S. occupied homes.

But more than 60 percent of occupied U.S. homes still will buy multichannel video packages, Kagan estimates.

Kagan also estimates that U.S. cable operators will have some 70 million internet access accounts in 2022. That is an interesting figure.

Assume there will be about 136 million U.S. homes in 2022. Assume 95 percent are occupied, leaving a base of about 129 million occupied housing units. Assume fixed network residential internet access adoption is about 75 percent in 2022.

That makes the total market about 96.75 million locations. If the Kagan forecast is correct, then cable might have 72 percent market share in 2022.

At the moment, cable has about 64 percent market share.

That requires some interpretation, though.

It is unlikely that cable operators facing Verizon or AT&T will do that well. At a high level, cable market share--where the cable operator faces AT&T or Verizon, could stabilize at about 60 percent.

The reason for that belief is that AT&T and Verizon appear not to be losing market share against cable, and that is before the upgrades by AT&T to gigabit networks, and before Verizon starts to launch new assaults out of region.

It might also be within reason that as AT&T and Verizon increasingly offer gigabit access across broader footprints, and independent providers also take some share, that cable’s share could drop to 50 percent or maybe less, as Comcast, Charter, Cox and a few others find themselves competing against both Verizon and AT&T in some markets, plus a handful of other independent providers.

That development would also assume that new bundles marketed by AT&T and Verizon, plus use of new forms of wireless access, also were successful ways both firms potential grew share.

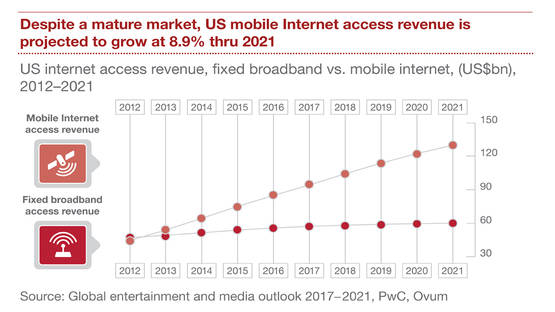

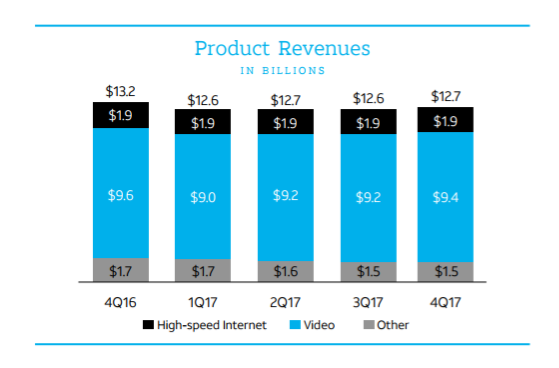

Researchers at PwC have estimated U.S. fixed network revenues will reach about $60 billion in 2021. That might be low.

Even if the average account generates only $50 a month, or $600 annually, 129 million accounts implies a market of about $77.4 billion. If one assumes average prices (gigabit and higher speed tiers) might sell for $70 a month, or $840 annually per account, then revenue could reach $108.36 billion.