Sign of the times: each of the two largest U.S. cable TV companies now have more voice subscribers than does AT&T, the largest fixed network telco.

In the fourth quarter of 2017, Charter Communications had 10,405,000 residential lines while Comcast had 10,351,000 accounts in service. AT&T had 10,333,000 lines. So, for the first time, the largest U.S. “telephone companies” were cable TV providers, not telcos.

A key qualification is required, however. Mobile is the way most U.S. residents use voice services. Well over half of U.S. homes (53 percent, according to the U.S. Centers for Disease Control) have no fixed telephone service at all. As recently as 2004, nearly 93 percent of U.S. homes had fixed network voice service.

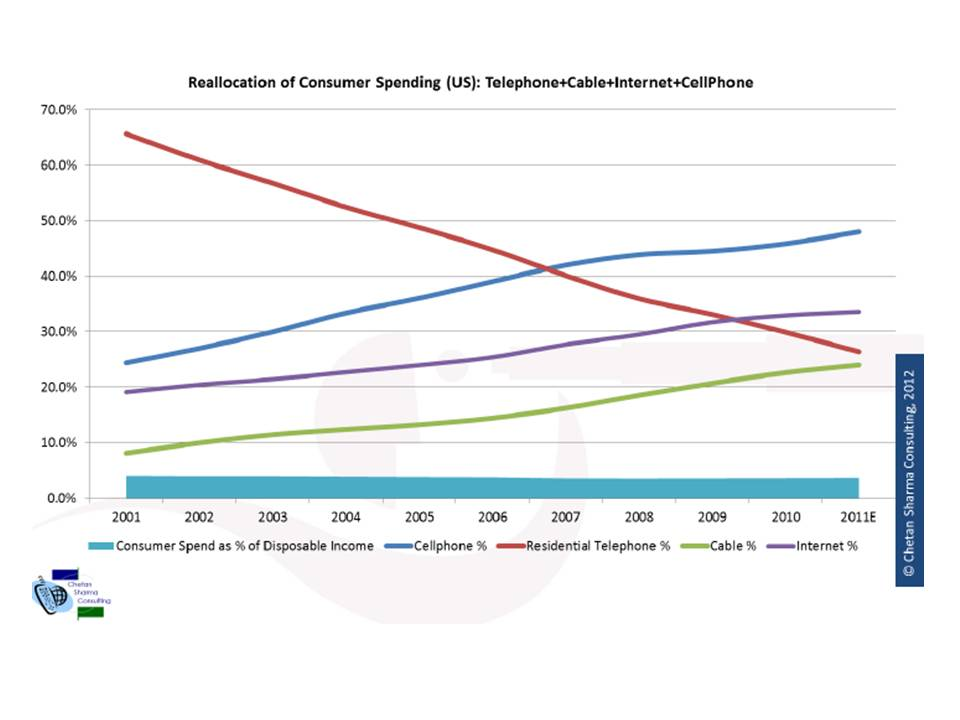

And, as always in the internet era, usage and revenue can be very different matters. In 2011, for example, U.S. consumer spend on fixed network voice had dropped from 65 percent to perhaps 26 percent, compared to 2001 levels, while mobile revenue grew from 25 percent to nearly 50 percent of total household spend, according to analyst Chetan Sharma.

Internet access spending grew from 20 percent of household budgets in 2001 to about 33 percent in 2011, Sharma estimates. Video entertainment spend grew from less than 10 percent of budgets in 2001 to about 24 percent of budget by 2011.

Such is the misfit between our legacy names for things and the new reality. Cable TV companies increasingly make most of their money from internet access, not voice. “Telcos” now likewise make most of their money from internet access, not voice.

Eventually, at least some major service providers will find they make 40 percent or more of total revenue from a range of services not directly related to internet access, voice or messaging. That already is the case for Comcast, and is close to the reality for AT&T, which earns about 31 percent of total revenue from entertainment video.

In fact, Comcast earns only about 29 percent of total revenue from its legacy TV business. Just as important, Comcast now earns about 37 percent of total revenue from applications, not services related to the access network (video, voice, internet access).

Over time, many tier-one service providers are going to have a similar profile, earning 40 percent or more of total revenue directly from applications (consumer and business), not managed services related to the ownership of the access network.