Government owned and operated internet access networks are opposed so fiercely by private suppliers because those private suppliers are quite realistic about the potential implications for their business models.

The possibility exists that such networks could essentially displace current providers of internet access services, driving one or more out of business in local markets where a municipal provider takes significant market share.

Craig Moffett, then an analyst at Bernstein Research, estimated in 2012 that a 15-percent drop in access lines would lead to a 15 percent to 20 percent increase in operating cost for AT&T, while for Verizon a 15-percent drop in access line customers has caused a 20- to 25-percent increase in operating cost.

So one might infer that a loss of 30 percent market share could lead to something like a 40 percent increase in operating costs for an AT&T or Verizon fixed network operation in any market where a robust new competitor is able to get 30 percent share of internet access.

Any attacker could do just as well, at lower household take rates, if it offers internet access, voice and video services.

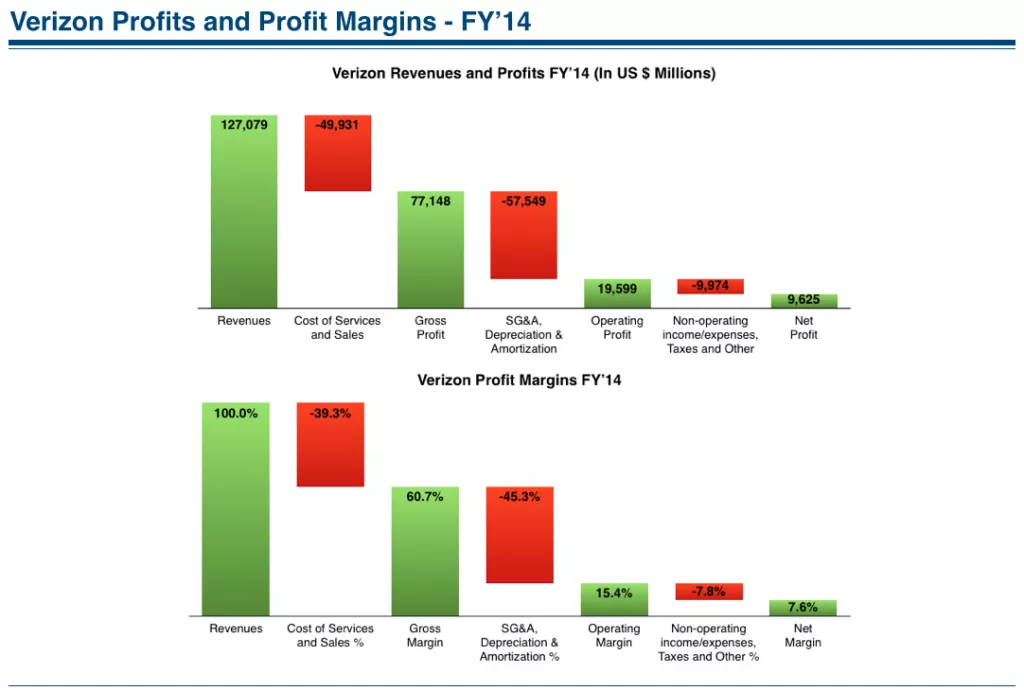

But other estimates suggest profit margins are much slimmer than that, being in single digits at Ve4izon in 2014, for example. And pressures have only grown since 2014.

So it is not hard to argue that, faced with share loss of 30 percent (theoretically, 15 percent lost at a local telco, 15 percent lost by the local cable company), telco or cable profit margins could evaporate.

Under some circumstances, it is theoretically possible for an upstart provider, owned municipally or privately, operating on a niche basis (not citywide, in many cases) to take so much market share (50 percent, for example) that at least one incumbent provider could be forced from the market.

But it still is quite risky, consultants suggest. A proposed municipal broadband in the suburbs of Portland, Ore. would be “marginally viable” at a 28-percent take rate, for example.

One might argue that a municipal network could have some advantages in construction, make-ready or marketing cost, but at least one study of such a network in San Francisco suggests that is not true. In other words, municipal network construction costs are on par with what a private firm would expect to pay.

If one assumes the objective of such municipal networks is to offer citizens and consumers lower prices, then some other economies are required. Lower operating or marketing costs, no need to generate funds to pay dividends, lower costs of capital or other cost advantages are necessary.