The biggest single problem telecom service providers face--bar none, including the threat of government regulation--is that connectivity prices in the digital era have shown a “disturbing” tendency to drop relentlessly lower, in some cases even trending towards zero.

Ad any industry facing near-zero levels of pricing faces a big existential (“concerned with existence”) problem. Unless that industry does something radically different, it is virtually guaranteed to become extinct. That does not mean the function goes away, only that the current industry supported by connectivity revenues could go away.

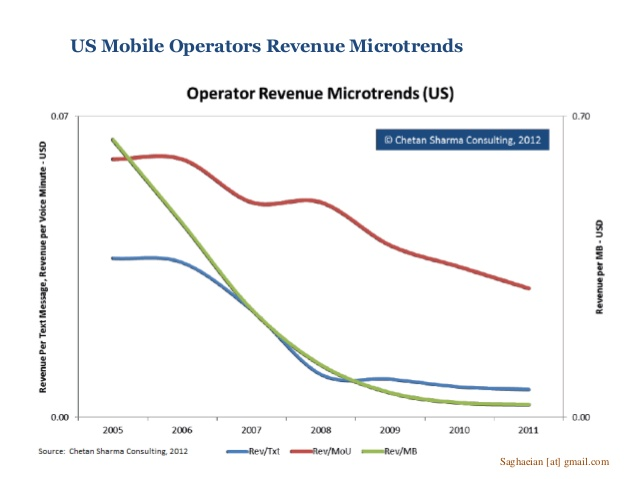

The illustrative cases are easy to name. Domestic U.S. calling rates; international calling rates; internet transit pricing; mobile text messaging; mobile voice prices; voicemail and other calling features.

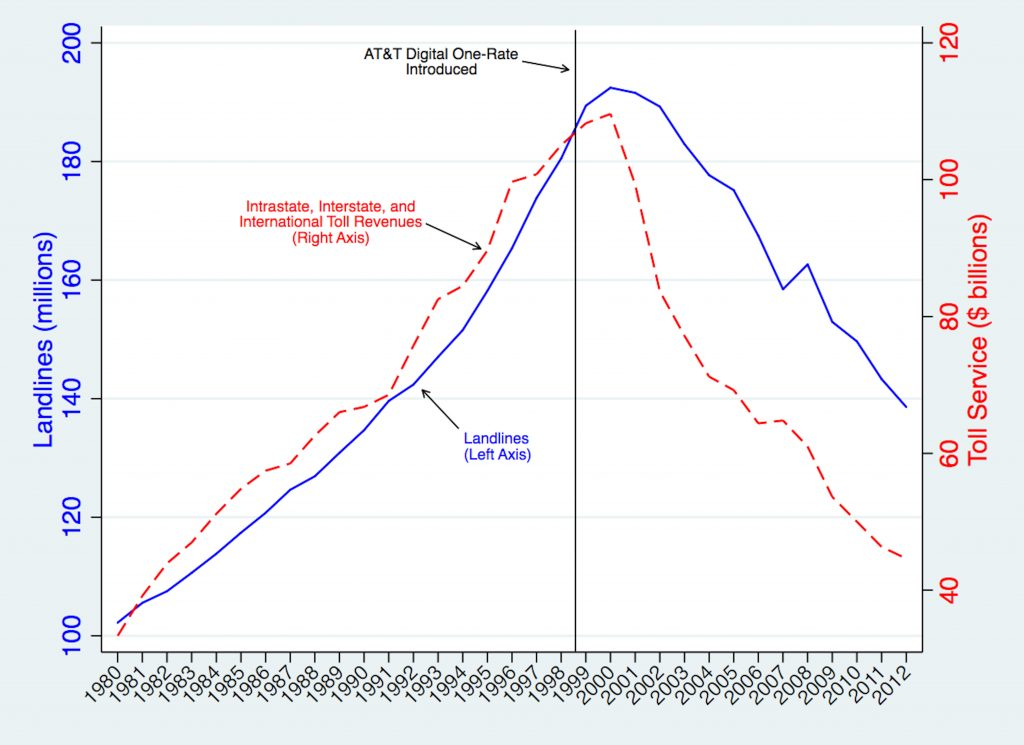

Consider the impact of just one form of product substitution. In 1998, AT&T launched “Digital One Rate,” conceived by Dan Hesse, (former Sprint CEO), who was at time in marketing for AT&T, that essentially eliminated the distinction between local calling and long distance calling. Within several years, both purchasing of local voice lines and long distance revenues began a long plunge.

In all those cases, products that once cost quite a lot now face substitutes literally offered for free, or for very little. So the legacy carrier products now have to contend with that product substitution, meaning lower prices and, in many cases, unlimited or virtually unlimited use.

Add the changes in user behavior--less calling, less texting, less buying of linear video services, ability to use Wi-Fi or other access mechanisms, substitution of mobile for fixed internet access--and one faces a potentially toxic mix.

Under such conditions, one can argue that surviving tier-one service providers must move up the stack, must take on additional roles in the value chain, must develop big new revenue sources beyond connectivity, as connectivity unit prices are going to keep dropping.

To reiterate, that belief flows directly from the marginal cost or near-zero levels of pricing for all connectivity services. Pricing that falls to nearly zero therefore is an obvious problem for the telecom or any other industry selling connectivity products as its main revenue sources.

Operating cost and some capex reductions are necessary, but not sufficient to remedy the near-zero pricing problem. The existential problem is that connectivity prices will continue to trend lower, and not even “higher consumption” will fix that issue, and demand for most of the products also is dropping as consumers switch to product substitutes.

The virtually universal set of solutions must include participation in much-wider parts of the ecosystems enabled by communications, as hard a challenge as that has, and will, prove.