It always is difficult to assess the potential impact of faster internet access in any area. “Areas that receive investment in infrastructure tend to do so because they are expected to grow rapidly in the future,” say researchers at Ipsos MORI.

The point is that investment follows growth potential. So investment might not “cause” growth, but reflects expectations for growth. And that might be an issue with any studies that suggest faster internet access causes economic growth.

The relationship could be merely correlative.

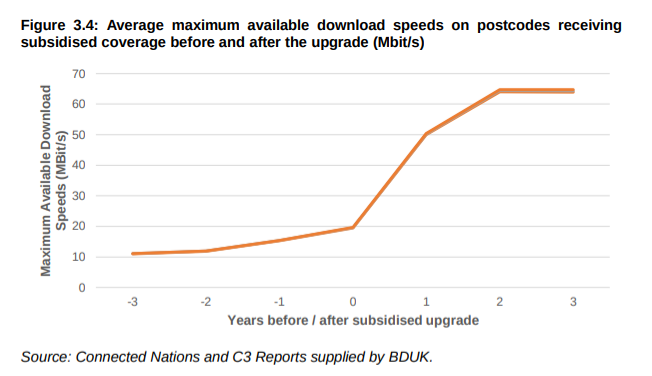

Researchers estimate that U.K. government support for “Superfast” (24 Mbps or faster) internet access between 2011 and 2016 lead to 2.5 million premises getting such speeds that would not have done so without the program. On average, speeds were boosted from about 20 Mbps up to more than 60 Mbps, the report says.

Perhaps another one million premises received superfast coverage one to two years earlier than they would have done otherwise, a report by Ipsos MORI says.

The perhaps more-controversial or potentially disputable portions of the report deal with economic growth outcomes.

“It is estimated that postcodes benefitting from subsidized coverage saw employment rise by 0.8 percent and turnover grow by 1.2 percent in response to improved infrastructure,” the report says.

Some 49,000 additional jobs were created in areas that got 30 Mbps or faster services. “The total turnover of firms located on those postcodes also expanded by almost £9.0bn (per year) in response to the upgraded infrastructure,” the report argues.

“The productivity of local economic activity, as approximated by turnover per worker, also increased by 0.32 percent as a result of faster available download and upload speeds, accounting for £2.1bn of overall turnover growth,” the authors assert.

“Over 80 percent of these impacts were driven by the relocation of firms to postcodes receiving subsidized coverage,” the report says.

The estimates are fine as far as they go, but arguably overstate the benefits. To sure sure, the faster internet might actually be “causal” if the firm relocations actually were triggered by the availability of faster internet access.

But other areas then also lost those firms, so the net national gain is arguably close to zero, for the activity gained and lost, in local areas. Report authors specifically say they have not discounted the impact of firms relocating from the analysis.

“Making superfast broadband speeds available also appeared to raise the productivity of firms that did not change location while the program was delivered,” the report says, and that is a possibly more-significant finding.

“It was estimated that subsidized coverage raised the turnover per worker of these firms by 0.38 percent, broadly consistent with other estimates of the impact of faster broadband in the UK, equivalent to £1,390 in output per firm per annum,” the report says.

“Assuming the results reflect underlying efficiency improvements,” it is estimated that the program led to a net increase in national economic output (GVA) of £690m by June 20166. The key word there is “assuming.” We do not actually know if the increase happened, or if it did, that those increases can be causally related to faster internet access speeds.

Subsidized coverage also supported “reductions in unemployment in the areas benefiting from the program.” That is probably what one would expect if a number of new firms relocated to the subsidized coverage areas.

It always is difficult to prove causation in such cases, to be sure.