Will disintermediation be one of the ways blockchain ultimately has value in the “technology, media and telecom” (TMT) industry? Possibly. Disintermediation is the process of removing distributors from any supply chain. Think “over the top” and you get the concept. So anything that promises disintermediation could have big consequences in the TMT space.

In the case of blockchain, that disintermediation could be a positive, not a negative, for content owners or distributors, though. Think about the problem of authenticating users and subscribers; participants in any social media transaction or in any highly-distributed access services environment.

Consider the case of a mobile services provider that amalgamates access to multiple networks, including assets secured from two or more other underlying service providers. Think of Google Fi, which uses Wi-Fi, Sprint and T-Mobile US networks. In some future scenario, perhaps blockchain is used to authenticate users for access to each of the participating networks.

To be sure, there are other ways of doing so. The issue is whether blockchain might be easier or cheaper, eventually, perhaps for cross-border (international roaming) transactions, for example. International settlements always are seen as a value of blockchain, in terms of taking cost out of such transactions.

The idea is that blockchain could have value whenever databases must be kept or transactions completed. Communications and content arguably have lots of places where those two things happen.

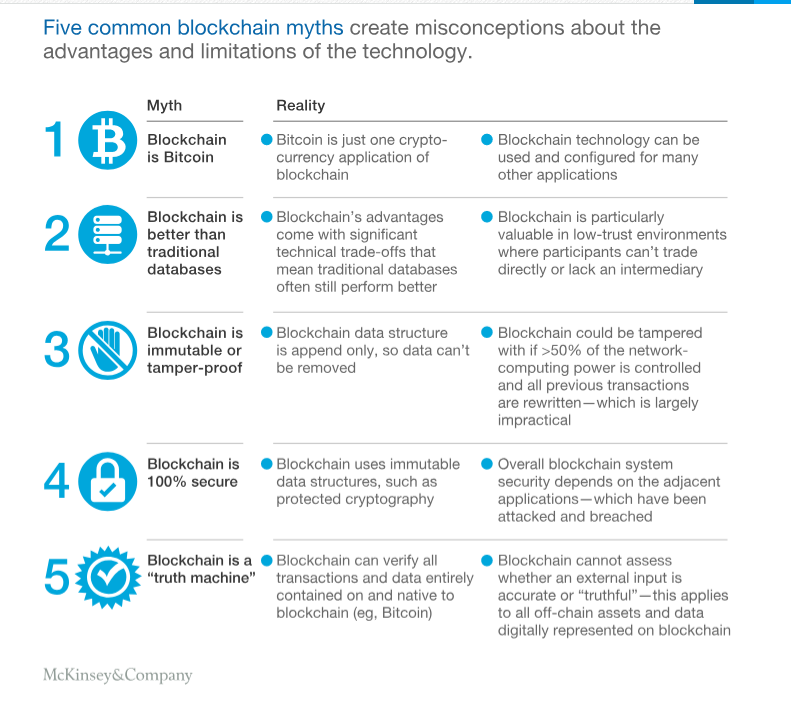

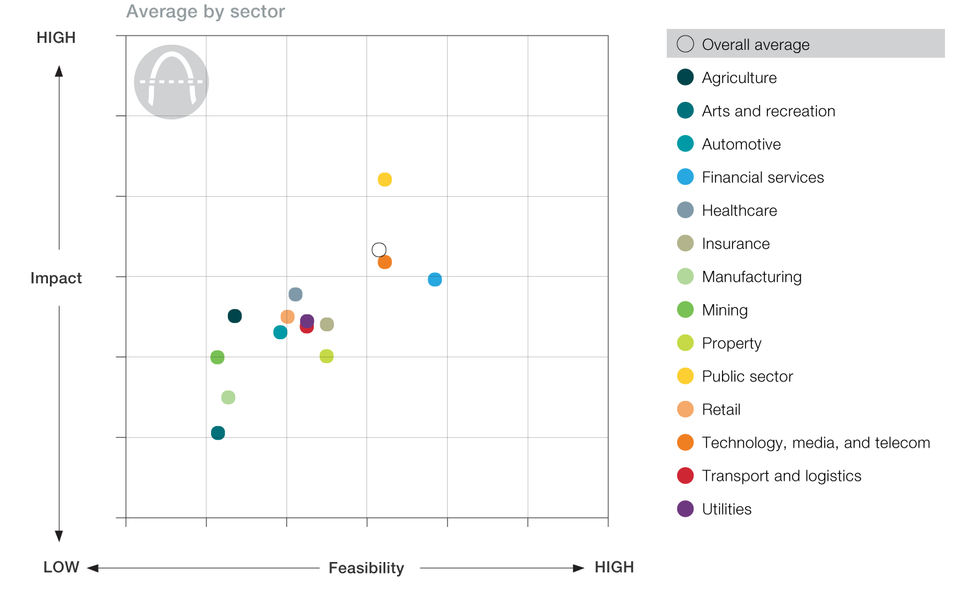

Blockchain is a technology of more than average potential usefulness in the “technology, media and telecom” industry (or industries; it is hard to say which is the more-apt description), according to consultants at McKinsey. In fact, in most industries, blockchain might have both low feasibility and relatively-modest impact, the consultants say.

Essentially, blockchain offers the hope of “perfect audit history,” without fraud. That obviously has implications for the financial industry, or any situation where “trust” is essential. And since “money” is always based on trust, that matters.

But trust has become a bigger issue for social media and advertising as well, which is likely why blockchain could have relevance in the TMT space. Though blockchain is not foolproof, it arguably is more hardy than most other ways of using databases, as fraud generally requires a wide level of willingness to commit fraud (something over half of all connected computers are in on the attempt, McKinsey essentially argues).

Nor can blockchain check on the integrity of data that is input into the database. “All that the blockchain itself does is ensure the integrity of the individuals making the transaction, ensuring that you have the right combination of a public and private key,” McKinsey analysts note.