Tuesday, July 9, 2019

The Earth is Getting Greener, Because of Higher CO2

Science is pretty amazing. Without minimizing carbon dioxide levels in the atmosphere, which can cause warming, carbon dioxide also is food for plants. That might explain why plant coverage now is increasing.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, July 8, 2019

Enterprise AI is in Early Stages, Expect Disappointment

A recent International Data Corporation survey of global organizations that are already using artificial intelligence solutions found only 25 percent have developed an enterprise-wide AI strategy.

It is likely very few enterprises had comprehensive personal computing or local area networking strategies in place in the early days, either. In fact, one might be safe in arguing that productivity paradox will continue to hold, and that quantifiable benefits from a shift to AI-enabled processes will lage investment by quite some degree.

The primary drivers behind these organizations' AI initiatives were to improve productivity, business agility, and customer satisfaction via automation, IDC researchers say.

Faster time to market with new products and services was another leading reason for implementing AI.

As always, though, there is a lag between capital investment in new technologies and tangible business results, if only since entire business processes must be redesigned before the full advantage can be gained.

So much disappointment with the outcomes of AI are to be expected. Quite often, big new information technology projects or technologies fail to produce the expected gains.

That “productivity paradox,” where high spending does not lead in any measurable way to productivity gains, is likely to happen with artificial intelligence and machine learning, at least in the early going. And that “early going” period can last far longer than many believe.

To note just one example, much of the current economic impact of “better computing and communications” is what many would have expected at the turn of the century, before the “dot com” meltdown. Amazon, cloud computing in general, Uber, Airbnb and the shift of internet activity to mobile use cases in general provide examples.

But that lag was more than 15 years in coming. Nor is that unusual. Many would note that similar lags in impact happened with enterprises invested in information technology in the 1980s and 1990s.

So prepare now: artificial intelligence and machine learning are eventually going to have the impact many now expect. It simply will take far longer than many expect.

No doubt, spending is growing. Some surveys suggest enterprises have dived into machine learning (artificial intelligence).

Half of those adopting machine learning are looking for insights they can use to improve their core businesses. About 46 percent report they are looking for ways to gain greater competitive advantage. Some 45 percent are looking for faster gleanings of insight. And 44 percent are looking at use of machine learning to help them develop new products.

But clear and quantifiable benefits will lag the investments. Thus it always is.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Net Neutrality Rules, or Absence of Rules, are Just Noise

Some argue U.S. customers are worse off since the end of network neutrality regulations, referring to transparency of charges and fees. Others would offer argue that net neutrality rules are sort of “noise,” not signal.

Broadband prices also are not high in U.S. markets, as a percentage of household or national income. Prices over time arguably have dropped, as between 1990 and 2000, for example. Adjusting for purchasing power parity, U.S. prices are in line with global prices.

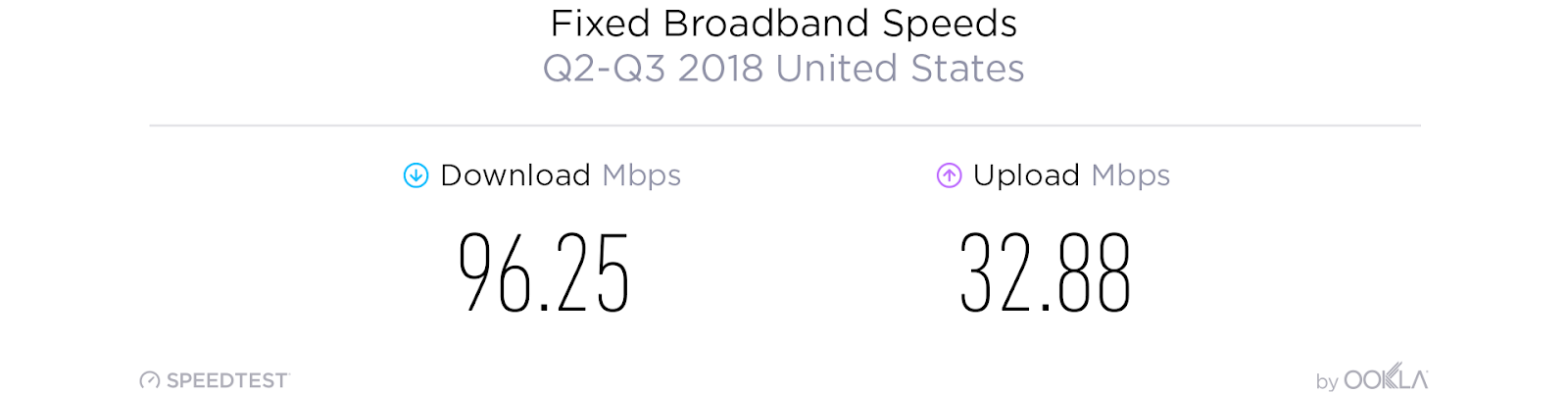

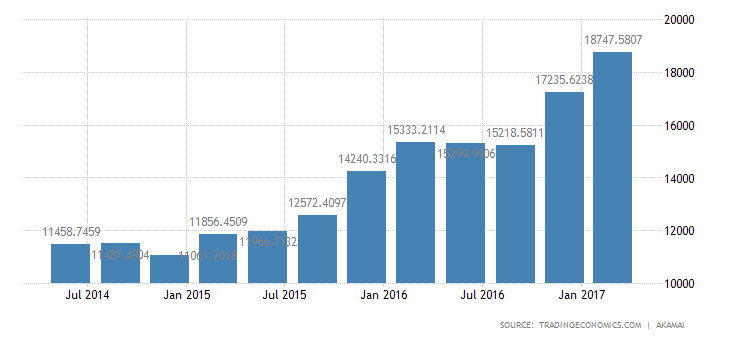

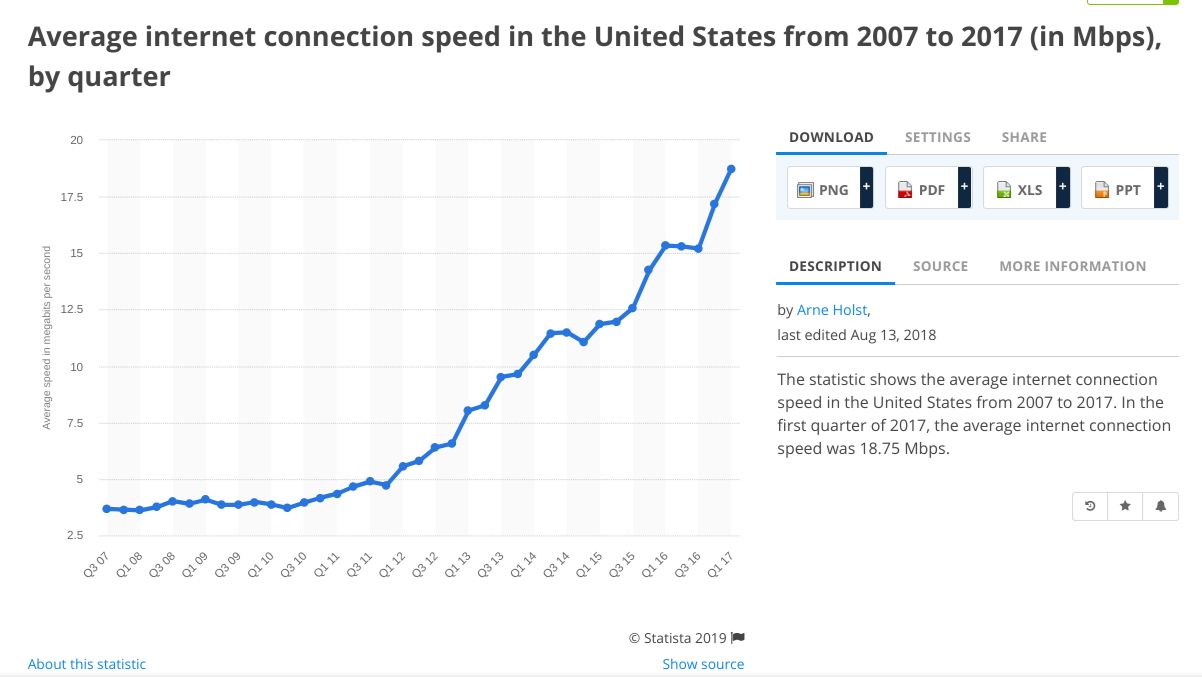

With or without the rules, speeds are climbing--and fast--while prices are in line with global norms or have decreased.

Though there are many other reasons for investments in networks that lead to speed improvements, network neutrality rules were in place from 2015 to 2017.

The larger point is that average U.S. fixed network speeds have risen dramatically since 2010.

Some focus on price as the problem, but absolute prices do not appear to have changed much, even as speeds and usage allowances have grown rapidly. Stand-alone pricing for residential internet access costs between $50 and $60 a month, less if purchased as part of a bundle, which most consumers do.

Broadband prices also are not high in U.S. markets, as a percentage of household or national income. Prices over time arguably have dropped, as between 1990 and 2000, for example. Adjusting for purchasing power parity, U.S. prices are in line with global prices.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, July 6, 2019

U.K. Service Provider Revenue has Dropped Since 2012

Connectivity traditionally has not been a “growth” business. Far from it, telecom had for most of its history been considered a natural monopoly, on a par with water, sewer and electrical service. Around the turn of the century there was some thinking that might have changed.

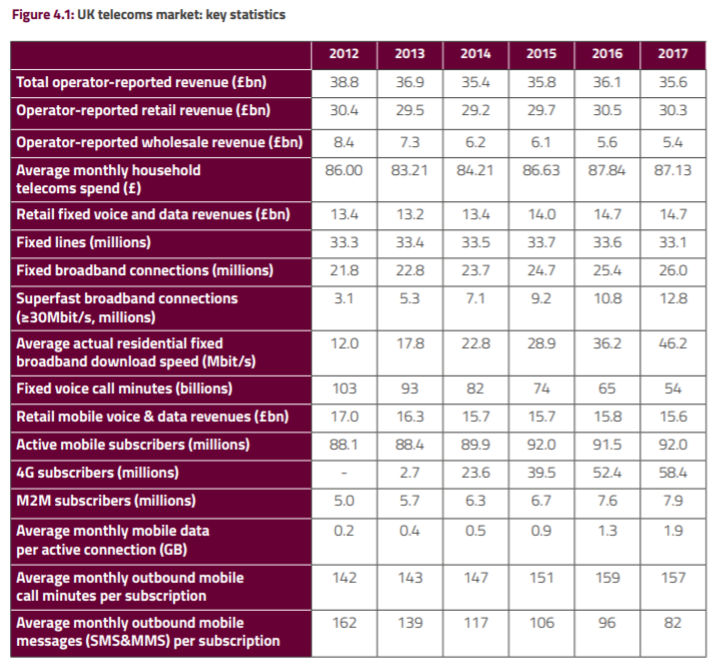

Alas, the connectivity business still seems to be a slow growth--in some cases no growth--type of industry. The latest data from U.K. regulator Ofcom shows this. Since 2012, total service provider revenue in the United Kingdom has dropped. Monthly household spending on communications has remained relatively flat, growing about one pound per household, per month.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

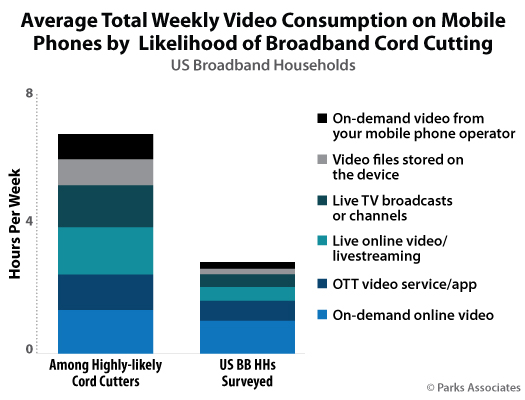

Heavy Mobile Video Viewers More Likely to Drop Fixed Network Inrternet?

“Potential broadband cord-cutters rely on their mobile devices for entertainment,” says Parks Associates senior research director Brett Sappington. “They are significantly more likely to watch live video content via mobile, including live TV broadcasts and live streaming, averaging an hour more per week each compared to average broadband households.”

That is a partial answer to the question of whether heavier mobile video usage can lessen the value of fixed network internet access as well.

Parks Associates argues U.S. broadband households highly likely to drop linear video services in the next 12 months watch more than six hours of video content on their mobile phone a week, compared to 2.5 hours among all US broadband households.

“Roughly 10 percent of broadband subscribers are likely broadband cord-cutters, with half of them highly likely to make the change in the next 12 months,” said Sappington.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, July 5, 2019

PTC Academy Bangkok

PTC Academy Bangkok: Executive Insight for Exceptional Leaders will be held 23 September through 25 September, 2019 at CAT Tower, 72 Charoen Krung Road, Khwaeng Bang Rak

Khet Bang Rak, Krung Thep Maha Nakhon 10500, Thailand. Registration is limited to the first 30 students.

The event begins with a dinner cruise on the Chao Phraya Princess, offering compelling views of the Bangkok metro area from the The Chao Phraya river.

The first day of classroom instruction includes:

The second day’s class includes:

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

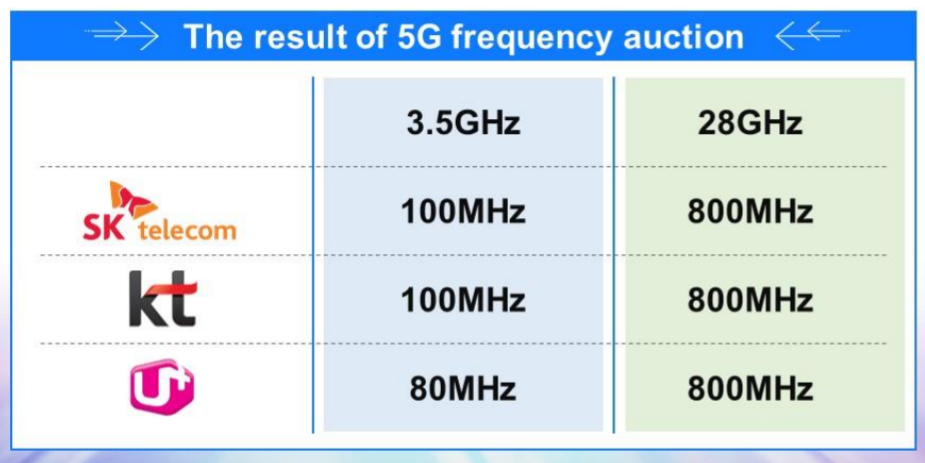

5G Spectrum Allocation Policies Differ in Japan, Korea

Communications policymakers in various countries will have to decide how to allocate additional mid-band and millimeter wave spectrum to various contestants. In some cases, policy might allow contestants to bid as vigorously as they like. In other cases, government policy might be more akin to “supporting a level playing field” by allocating spectrum on an equal basis.

Here’s a look at mid-band spectrum held by the leading mobile operators in Japan, according to Gaku Nakazato of Japan’s Ministry of Internal Affairs and Communications. As you might guess, KDDI and NTT have the largest allocations. NTT and KDDI have the largest subscriber shares, and therefore arguably require the most spectrum.

Policy in South Korea seems to aim for equal capabilities for the leading service suppliers. Both mid-band and 28-GHz millimeter wave allocations are virtually equal.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Will Video Content Industry Survive AI?

Virtually nobody in business ever wants to say that an industry or firm transition from an older business model to a newer model is doomed t...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...