Comcast’s third quarter results were driven by consumer and business internet access connections. And that is the potential threat posed by 5G fixed wireless alternatives: they strike at the heart of the revenue growth model based on the Comcast fixed network.

Thursday, October 24, 2019

Comcast 3Q Results Driven by Internet Access, Which Explains Potential Danger of 5G Fixed Wireless

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Revenue from Digital Transformation Will Take Twice as Long as Enterprises Expect

Through 2021, incremental revenue from digital transformation initiatives is largely unlikely, Gartner researchers predict. That will not come as good news for executives hoping for revenue growth from repositioning existing business practices for digital delivery and operation.

On average, it will “take large traditional enterprises twice as long and cost twice as much as anticipated,” Gartner researchers predict.

"In most traditional organizations, the gap between digital ambition and reality is large," said Daryl Plummer, distinguished vice president and Gartner Fellow.. "We expect CIOs' budget allocation for IT modernization to grow seven percent year over year through 2021 to try to close that gap."

We probably should not be surprised, as major new technologies quite frequently take decades to show visible financial results. That might be another manifestation of the productivity paradox.

Quite often, big new information technology projects or technologies fail to produce the expected gains. That “productivity paradox,” where high spending does not lead in any measurable way to productivity gains, is likely to happen with artificial intelligence and machine learning, at least in the early going. And that “early going” period can last far longer than many believe.

To note just one example, much of the current economic impact of “better computing and communications” is what many would have expected at the turn of the century, before the “dot com” meltdown. Amazon, cloud computing in general, Uber, Airbnb and the shift of internet activity to mobile use cases in general provide examples.

But that lag was more than 15 years in coming. Nor is that unusual. Many would note that similar lags in impact happened with enterprises invested in information technology in the 1980s and 1990s.

investments do not always immediately translate into effective productivity results. This productivity paradox was apparent for much of the 1980s and 1990s, when one might have struggled to identify clear evidence of productivity gains from a rather massive investment in information technology.

Some would say the uncertainty covers a wider span of time, dating back to the 1970s and including even the “Internet” years from 2000 to the present.

Computing power in the U.S. economy increased by more than two orders of magnitude between 1970 and 1990, for example, yet productivity, especially in the service sector, stagnated).

And though it seems counter-intuitive, some argue the Internet has not clearly affected economy-wide productivity.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Wednesday, October 23, 2019

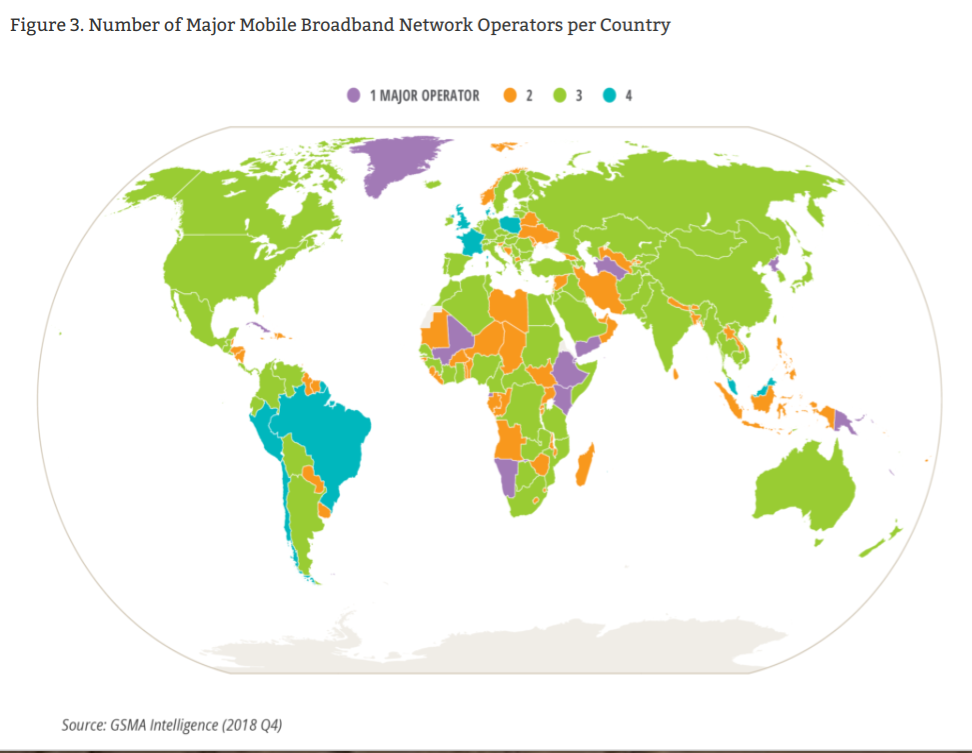

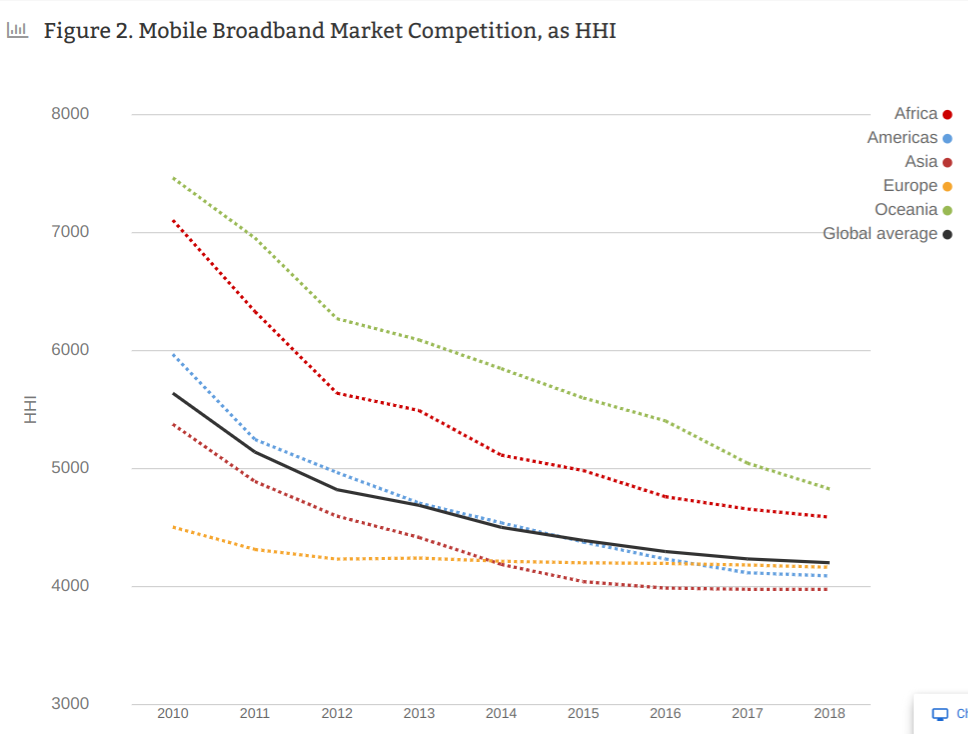

Mobile Industry is Highly Concentrated, and Unlikely to Change

With a few exceptions, the mobile service provider business tends to feature three providers in any single country. With the caveat that nationwide telecom systems always tend to be few in number, virtually every mobile market is highly concentrated, using the Herfindahl-Hirschman Index (HHI), a widely-used measure of market concentration.

A market with an HHI of less than 1,500 is considered to be a competitive marketplace, an HHI of 1,500 to 2,500 to be a moderately concentrated marketplace, and an HHI of 2,500 or greater to be a highly concentrated marketplace.

No mobile market actually can be deemed “competitive” using the HHI test. On the contrary, every mobile market is highly concentrated.

Some might argue that relative lack of competition explains the price of mobile data, which because of less than robust competition costs users an estimated $3.42 per gigabyte, according to the Alliance for Affordable Internet.

In cases where only a single facilities-based supplier operates, breaking up a broadband monopoly can create a savings of up to $7.33 per GB for users, the Alliance for Affordable Internet argues.

Across Africa, for example, a continent with generally less robust competition, the average cost for 1GB data is 7.12 percent of the average monthly salary. In some countries, 1GB costs as much as 20 percent of the average salary, says the Alliance.

If the average U.S. earner paid 7.12 percent of their income for access, 1GB data would cost $373 per month.

Though many would note that the existence of mobile virtual network operators will increase competition, it also is an industry fact of life that capital-intensive connectivity networks will always be relatively few in number. It is an oligopolistic industry.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, October 21, 2019

How Much Market Share Does 5G Fixed Wireless Have to Take to be Meaningful?

How much market share does 5G fixed wireless have to gain to be meaningful? For some new potential suppliers, even a few percentage points of market share could be significant. A million accounts represents about one percent of the total U.S. fixed network internet access market.

For a new provider, that could represent incremental recurring revenue of perhaps $720 to $960 in annual account revenue, assuming monthly recurring revenue of either $60 a month to $80 a month.

At just one percent market share, that represents $720 million to $960 million in recurring annual revenue. If the functional definition of the minimum revenue opportunity large enough to be considered by a tier-one service provider is $1 billion, then 5G fixed wireless fits the bill.

If any single internet service provider is able to get five percent market share, that represents about $5 billion in incremental recurring annual gross revenue. For a firm such as AT&T, with debt service payments about $6.8 billion (though set to decline), that is an important revenue contribution.

Another answer might be that, in the U.S. market, 5G fixed wireless will be meaningful for fixed network ISPs if it brings the rate of cable TV net additions close to zero. For cable, that would choke off the most-important driver of subscription revenue. For telcos, that also could mean a halt to share losses in the internet access category that have been on-going for at least a decade.

Consider that in any particular quarter, cable tends to gain about half a percent market share, or about 532,000 net accounts. With internet access now driving subscription revenue growth, that matters.

If all suppliers of 5G fixed wireless collectively manage to gain 532,000 accounts per quarter, or about 2.1 million net accounts a year, cable’s subscriber business grinds to a halt, all other things being equal.

Some predict 5G fixed wireless accounts could, over the next four years, garner about 4.5 million accounts. That would not cause cable gains to go to zero, but would cut internet access gains--all other things being equal--in about half.

Though many doubt fixed wireless can reach 15 percent to 20 percent share of the U.S. fixed network internet access market, that implies gains of between 15 million and 20 million accounts.

Some of us might argue that 5G fixed wireless would be significant for the market at even 10 percent share gains, as that could represent a key reversal of market share trends of some years standing, between cable and telcos. Gains might also be important for some other providers not presently in the fixed network internet access business.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, October 20, 2019

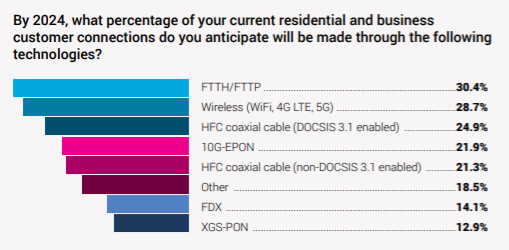

Cable Operators Plan Lots More FTTH Deployments

Hybrid fiber coax will remain a viable cable TV network platform for some time, as a Light Reading survey of cable operators globally found that executives expect 46 percent of their residential and business customer connections to be coaxial-based in 2024.

But it also is noteworthy that fiber to the home or premises for business customers are expected by 29 percent of respondents, as well as 22 percent who said they would deploy 10-gigabit EPON passive optical networks, while 13 percent said they would use XGS-PON.

The results among North American respondents are nearly identical to the global results, according to Light Reading. The percentage for Docsis 3.1-enabled HFC is two points higher among North American respondents (26.8 percent total), than among other respondents.

Among smaller North American cable providers (those with annual revenue of less than $1 billion), 55 percent of connections are expected to use coaxial cable drops, compared to 41 percent for larger North American providers (those making $5 billion or more annually).

Both small and large North American providers expect FTTH/FTTP to be a significant part of their mix. Smaller North American providers actually anticipate a larger percentage of their customer base will be served through direct fiber connections than large providers, 30 percent versus 24 percent, respectively.

Close to one-half of cable respondents (46 percent) said their company will carry out FTTP network upgrades with 10G-EPON over the next two years, making that the lead choice.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

FNB Connect Voice Revenue 30% to 40% of Total: What Next?

Voice accounts for about 30 percent to 40 percent of FNB Connect total revenue, the firm says. FNB launched its own mobile service in 2015. That points out a salient fact for the telecom industry: voice once generated the bulk of revenues, but now is an essential function, but less a revenue generator.

In 2016, for South Africa as a whole, mobile operators made about 53 percent of total revenue from voice services. Mobile data services contributed 38 percent of total revenue, text messaging about seven percent of total revenue.

But voice revenue is declining fast, globally. Using 2008 as a baseline, by 2013, five years later, a number of tier-one service providers had lost between 20 percent and 55 percent of legacy voice revenues.

Looking back over a longer time frame, in the U.S. market, one can see that 2000 was the year of “peak voice” for long distance revenue earned by local telcos. The usage drop over about a decade from 2000 was more than 50 percent. The revenue drop tracked usage decline.

Mobile service providers in Asia might face similar pressures on revenue. My general rule on revenue earned by service providers is that telcos must expect to lose about half their legacy revenue every decade. The U.S. experience with revenue loss provides one example, but each nation and market should be able to find similar changes.

That of course creates the necessity of developing big new revenue sources to replace those lost revenues, and in turn reflects the product life cycle in general. Intel, for example, seems to exhibit that same general pattern.

Im 2012, for example, Intel earned nearly 70 percent of revenue from “PC and mobile” platforms. By 2018, PC/mobile had dropped to about half of total revenue. By 2023 or so, Intel should generate 60 percent or more of total revenue from sources other than PC/mobile.

The point is that any service provider that intends to make a living “sticking to its knitting” and selling connectivity products has to account for the shrinking demand curve. To be sure, new connectivity products are being created. Software-defined wide area networks provide one example.

But that will not be nearly enough. The challenge is to replace half of total revenues from legacy sources. SD-WAN revenues available to service providers presently do not exceed a couple billion dollars a year. Total global revenue is about $1.5 trillion. That implies a need to discover or create as much as $750 billion worth of new revenue over the next decade, globally.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, October 18, 2019

South Korea has 10% FTTH Take Rates. Is that a Problem?

Take rates (percentage of customers who actually buy a service) are not the same thing as availability (the percentage of consumers who actually can buy a product). That is worth keeping in mind when evaluating the relevance of take rates for fiber to home services. It is doubtful many people actually believe South Korea has an internet access problem, even if buy rates for FTTH might be as low as 10 percent.

Internet access reaches about 99 percent of South Korean households, and South Korea has the fastest average internet access speeds globally, in some studies, or ranks among the top three, in other studies.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

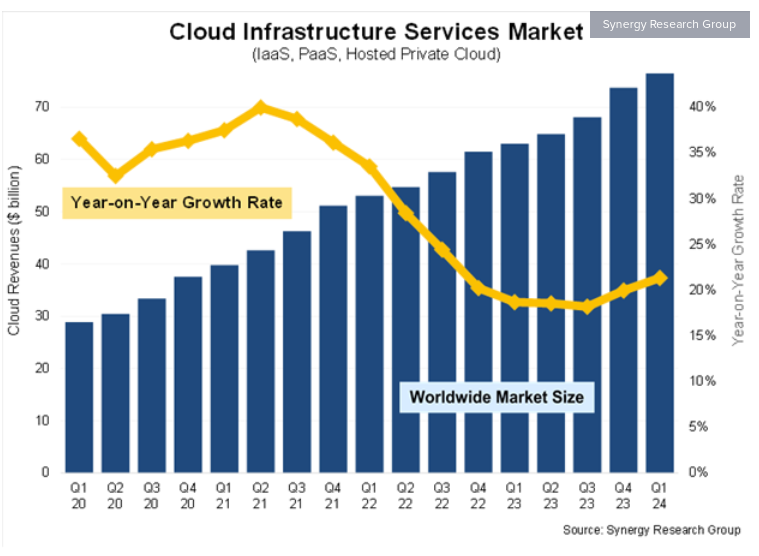

Cloud Computing Keeps Growing, With or Without AI

source: Synergy Research Group . With or without added artificial intelligence demand, c loud computing will continue to grow, Omdia anal...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...