Based on past behavior, it is hard to forecast the strength of consumer demand for 5G in Germany. So far, nearly half of all subscriptions might use 3G, instead of 4G. nearly a decade after 4G was introduced.

Governments and policymakers always are quick to quantify gaps in uptake, quality or availability of communications services, which is among the reasons stories about any form of digital divide are evergreen. Most often, studies about service gaps rely on supply or demand indices, including network availability, typical speeds and cost.

Demand side choices by consumers tend to overlooked. In other words, some “gaps” might reflect consumer choices, not failures of supply. And that matters for 5G, as much as it did for 4G. Consider the case of Germany.

We often are surprised at the resilience of legacy services, as those use of legacy services is always a case of supply failure. Not always. Sometimes demand choices are at work.

That appears to be the case for German mobile users and 3G. According to a recent study by Opensignal, as many as half of German subscriber identity modules (mobile accounts) are not enabled for 4G service.

In other words, a huge percentage of German mobile users seem to be opting to remain on 3G networks even when 4G networks now are in good supply, with good to improving performance metrics.

In other words, the question is why so many German users opt to remain on 3G networks when 4G networks are widely available and offer better performance. Low consumption of mobile data might be part of the explanation, some could argue.

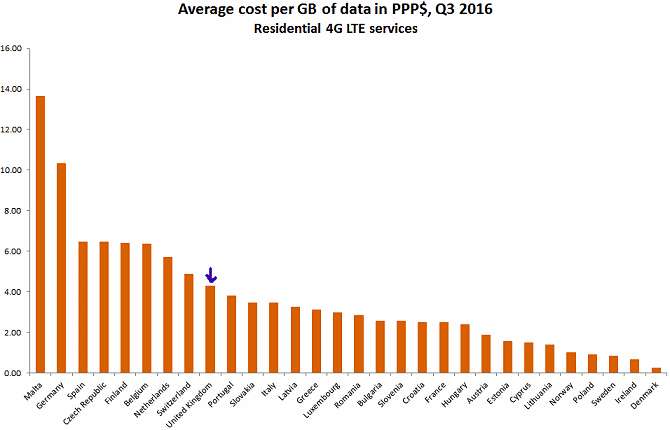

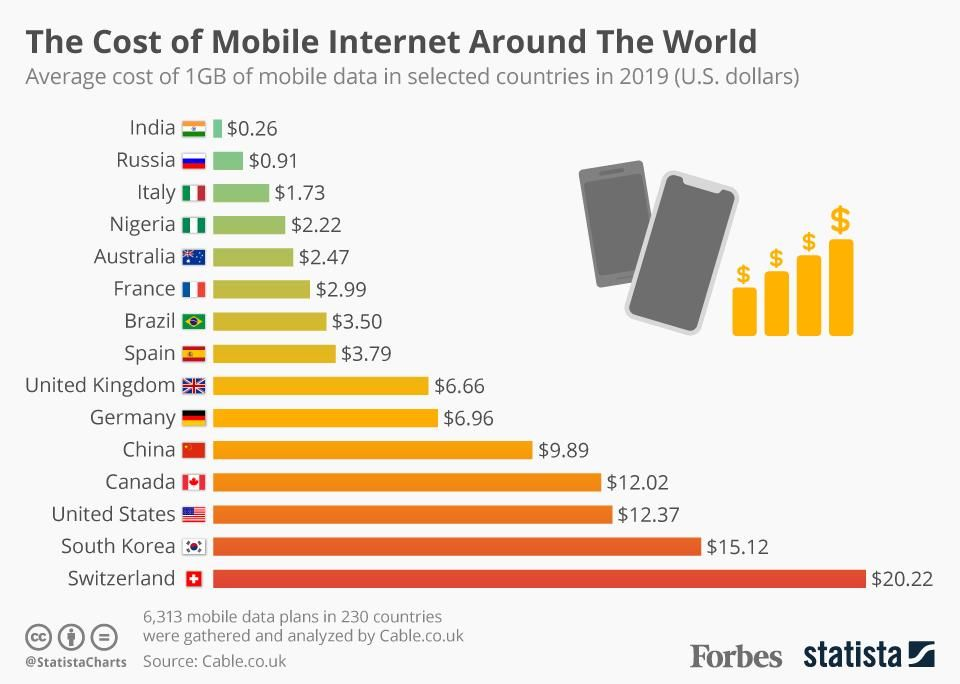

Compared to customers in other developed nations, Germans seem to consume less data. Some might point to high cost per gigabyte as a contributing factor. At least in 2016, German per-gigabyte costs were on the high side, compared to other European nations.

But per-gigabyte costs in Germany have fallen since 2016, as they have virtually everywhere else in the world.

To be sure, the actual cost of using mobile data depends on which plans users have. And international comparisons require choices about which plans to compare. That can distort results if the plans most-often used in particular countries are not uniform. In other words, if most consumers in some countries buy large-usage plans, others buy small-allocation plans, while in yet other instances most consumers buy on group or bundled service plans, not stand-alone mobile plans, comparisons are going to skew in ways that do not actually reflect buyer choices across countries.

Consider this analysis of mobile internet plans featuring big usage allowances of 20 to 42 gigabytes per month, compared to the analysis above of one-GB usage plans. Where smaller usage plans might feature per-GB costs as high as $12 per gigabyte, when bought in higher volume (22 Gbytes in this case), cost drops to about $2.50 per GB.

Still, the point is that cost per gigabyte, or absolute cost, might not explain why so many German consumers choose 3G over 4G.

Still, according to Opensignal, perhaps 81 percent of 4G non-users have for some reason elected not to buy 4G service. Some might suggest the “poor” state of German 4G networks explains why people do not buy. That seems unlikely.

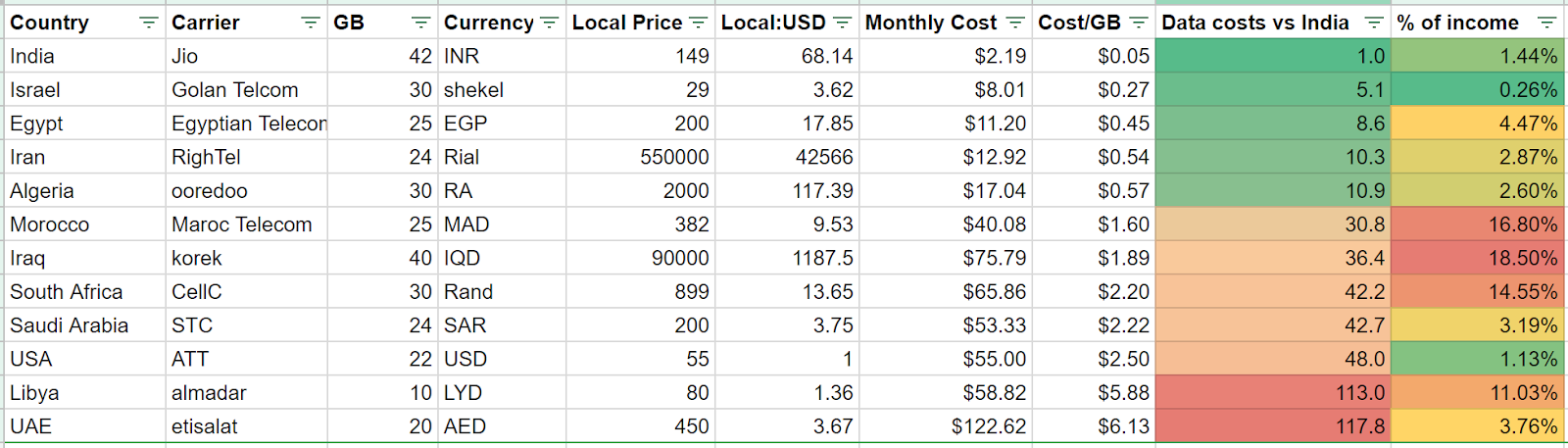

In a July 2019 study by Tutela, 4G downstream speeds averaged 23.5 Mbps on Telekom’s network, 21 Mbps on Vodafone and 18 Mbps on O2 networks.

To be sure, German downstream speeds tend to be slower than in Switzerland or Austria, as measured by Tutela, but average downstream speeds--based on both 3G and 4G activity--of about 14 Mbps do not seem out of line on a global basis.

Also, recent tests show typical 4G speeds in German cities ranging from about 25 Mbps to 35 Mbps, which does not seem slow, as far as 4G goes.

Nor do German 4G speeds seem to have lagged, by about 2017, in comparison to other developed nations.

The point is that it is not self evident that poor 4G experience explains the lag in uptake. But some might point to coverage, rather than speed, as an explanation.

“Whereas network providers in the Netherlands, Belgium and Switzerland can almost all offer LTE (4G) connections nearly 90 percent of the time, German communications giant Deutsche Telekom in Germany achieves only a 75 percent rate,” a study by consulting firm P3 says. Vodafone in Germany has 57 percent LTE coverage, P3 says.

By some estimates, 4G coverage in Germany does not seem underdeveloped, though, and less coverage in eastern regions might be explained by greater rural character in the east.

According to Germany’s Federal Network Agency (Bundesnetzagentur), at the end of 2018, there were 107.5m active SIM cards in Germany (excluding M2M and IoT cards), but only 50.5m 4G/LTE SIM cards in active use. This would indicate that roughly half of the active SIM cards were not LTE-enabled

According to Opensignal, 81.4 percent of users that have never connected to 4G had a 4G-capable phone and spent time in 4G-covered areas. “These users likely did not upgrade to a 4G subscription or have disabled 4G connections on their phones,” says Opensignal.

Perhaps 15.6 percent of users who did not connect to 4G networks spent time in 4G-covered areas but did not have a 4G-capable device.

A small percentage of non-4G users (perhaps three percent) appear not to live in rural areas where 4G is available.

The point is that consumers sometimes choose not to buy the better or best mobile data plans, based on speed, price, availability (coverage) or other considerations. German consumers seem to be content buying 3G, instead of 4G, for some combination of reasons.

So one wonders what the reception for 5G might be.