It might be rational to expect connectivity provider revenue to dip in the wake of the economic shutdowns imposed to combat the Covid-19 pandemic. That might not prove to be the case.

A better assumption is that markets growing before the pandemic will see reduced growth, but not a dip in growth. Markets that were flat will probably simply remain flat. Markets that were contracting before will contract afterwards.

That might make sense two years after 2020, some might argue, but will not apply to 2020. After all, the economic impact of efforts to defeat the pandemic will lead to major dips in economic activity and employment. There will be significant numbers of business bankruptcies. All that should reduce aggregate demand for communications services.

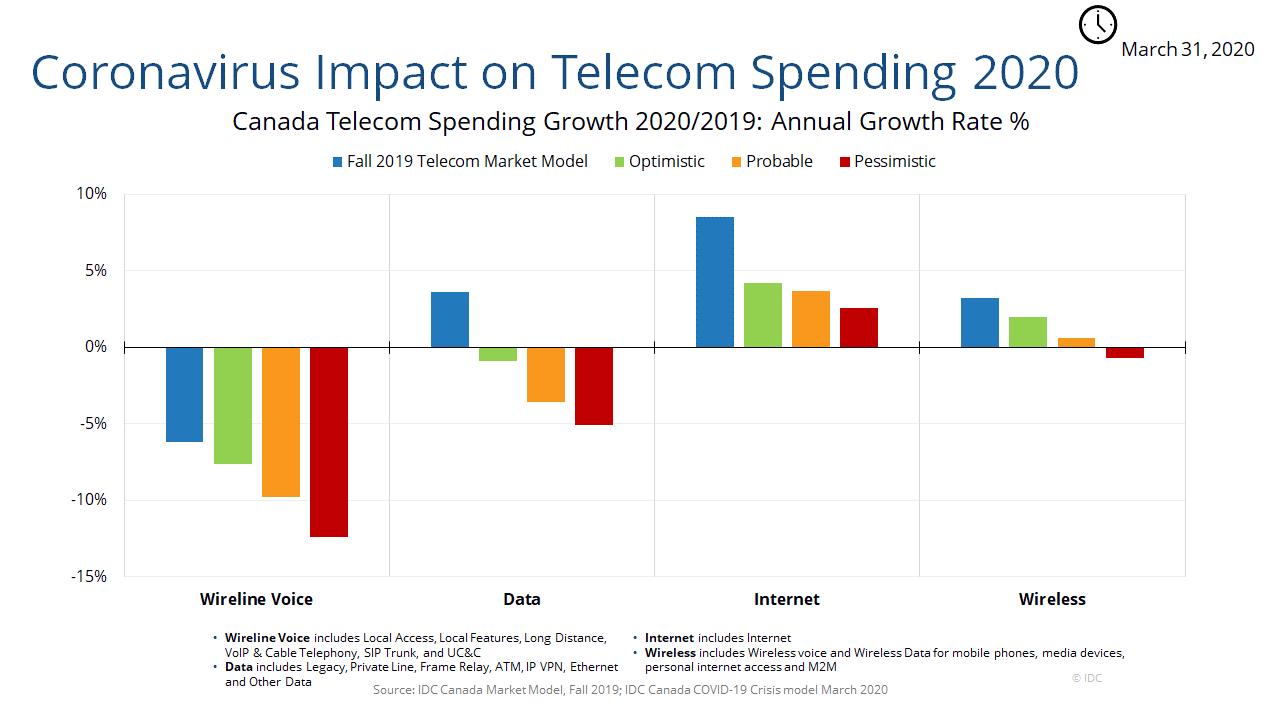

That appears to drive analyst thinking at IDC Canada. Analysts expect that the telecom services market will contract by almost C$2 billion with the overall revenue expected to fall to C$47.9 billion – a negative -0.8 percent decline from a year earlier.

“As recently as December 2019, we had projected positive 3.2 per cent annual growth for the sector in 2020,” they say. By comparison, IT spending in Canada is expected to decline by negative five percent in 2020, according to IDC Canada's most recent forecast estimate.

The greatest adverse impact on telecom spending forecasts is the projected number of business failures, IDC predicts. The contrary argument would be that communications spending, overall, did not seem to dip in the wake of the great recession of 2008, but only flattened.

A dip in revenue might seem the obvious call, as consumption and consumer spending fell virtually across the board in the great recession of 2008, and the virtual shutdown of large parts of the economy in response to the Covid-19 pandemic would seem likely to produce something similar, if not worse.

But that does not directly translate into consumer, small business and enterprise spending on communication services and products. According to TeleGeography Research, revenue growth slipped from about seven percent annually to one percent in 2009, returning to about three percent globally in 2011. The recession affected revenue growth, but there was no dip in total revenues, overall.

Underlying revenue trends will persist, in other words, within a couple of years after the event. Markets that were growing before will continue to grow. Markets that were contracting will continue to contract. Markets with slightly-positive growth will continue to grow slowly.

Looking at cash flow earned by Canadian communications firms, total cash flow has been dropping since 2015, according to the Canadian Radio-television and Telecommunications Commission. In terms of revenue, mobile and internet access revenues (not profits, necessarily) have been growing since about 2014, while all other revenue sources have shrunk.

One important input for the mobility business that drives overall revenue is the role played by device sales, with a 43 percent compound annual growth rate between 2014 and 2018, while voice and messaging revenues actually had negative rates of growth, with data services, roaming and other sources were up less than six percent.

In other words, perhaps Canada is a market where revenues and profits had been dropping before the impact of Covid-19. A dip in 2020 revenues, as a temporary impact, ignores the preceding trend, which was downward. Again, the point is that the underlying preexisting trend prevails, after the temporary Covid-19 effect in 2020.

Telecom service provider revenues did not change much in the wake of the great recession of 2008. In fact, according to some studies, U.S. consumer spending on communications actually grew, overall, in the wake of the Great Recession, for example.

Some surveys found that device purchases slowed during the recession. But some surveys also found consumers willing to make other tradeoffs to keep their broadband, mobile and video subscription services. There was, in other words, less willingness to cut high speed access than other services, for example.

The point is that service provider revenues might not fall, though growth might be reduced to zero. In fact, some studies show that global revenue continued to grow even during the recession of 2008.

IDC Canada says the fixed network voice, which has been a shrinking market, remains the worst-performing segment under all scenarios because of continued mobile and internet substitution, IDC says. However, long-distance revenue gains might be “major” gains from use of toll-free long-distance conferencing.

Wide area networking services could be affected by business failures, while internet access “will be one of the most insulated markets.”

Mobile services, which account for almost half of telecom revenue in Canada, remain essential, and likely might see some roaming revenue loss, but not much other downward pressure, the analysts believe.