Lack of customer scale now seems to correlate with lower productivity and profits for fixed network connectivity businesses, while high scale seems also to correlate with mobile network productivity and profits.

“The difference in labor input between wired and wireless is mainly a matter of scale,” notes the U.S. Bureau of Labor Statistics. “The extreme rapidity of the labor productivity growth in wireless suggests that technological innovations—new ways of doing things with new types of hardware and software—still play a leading role in the story.”

“The difference in labor input between wired and wireless is mainly a matter of scale,” says BLS.

That arguably is true in most--if not all--businesses: scale and market share matter. Profits tend to correlate with market share, for example. Market share also tends to correlate with cost structure.

Drives to reduce operating cost and capex for new networks have been issues for a couple decades in the telecom business. Headcount reductions, tower sharing, streamlined customer service, open architecture, “do it yourself” servers and routers and open source have been tools used for that purpose, and the work continues.

But it appears much of the easy gains have been gotten, for mobile networks, computers, communications infrastructure and semiconductors, according to the U.S. Bureau of Labor Statistics. Only the mobile industry has improved its productivity since 1987.

source: BLS

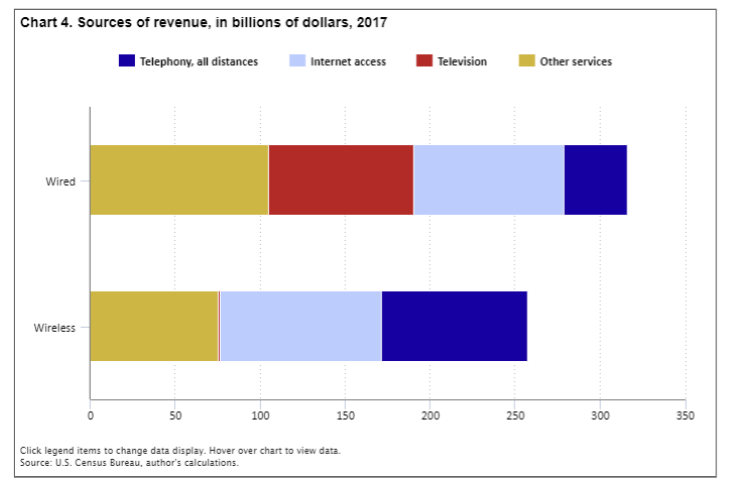

Scale matters elsewhere. In the U.S. market, fixed network revenue peaked around 2000, and has steadily fallen since then. For example, long distance minutes of use peaked in 2000. The number of U.S. landlines in service peaked about 2001. Long distance revenue peaked about 2001 as well. Most markets will follow a similar trajectory.

But mobile revenue has grown since 2000. So scale arguably matters for profitability and productivity, not simply gross revenue.

In the wired industry, output peaked in 2000. “The wired industry actually produced less output in 2018 than it did in 2000,” the BLS says. “Conversely, output for the wireless industry has continued to multiply, growing at an average annual rate of 13.1 percent since 2000.”

Open source and open architectures have played a role in reducing capex and opex, and continue to do so. The Open-RAN Alliance, GSMA, Telecom Infra Project and others are working to create open standards and interoperability of mobile radio access networks, core networks and other key infrastructure. That, in turn, is expected to lead to lower RAN costs.

But scale does matter most. The basic problem for a fixed network provider is stranded assets, caused by lost market share taken by competitors, product substitution that shrinks demand for fixed access. The installed base of assets remains the same, but declining subscriptions and revenue mean the actual cost per customer keeps going up.

At the same time, though prices have not fallen consistently for all products, the general trend is lower average revenue per account, or at least lower revenue per unit sold.