It has long been possible to get a reasonable debate on the respective values of content and distribution in the media business. Simply put, the issue is which part of the value chain is better positioned. Consider one illustration. The market value of Netflix is something on the order of $213 billion. Content creator Disney has a market cap of about $250 billion.

Market cap is not everything, and both firms produce and distribute content. But it might be surprising that Netflix is so close to Disney, given its simpler business model, which includes original content production, but relies on distribution (subscriptions) for its revenue.

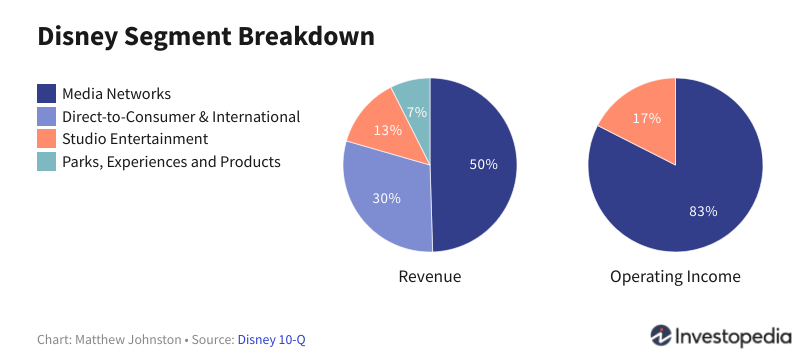

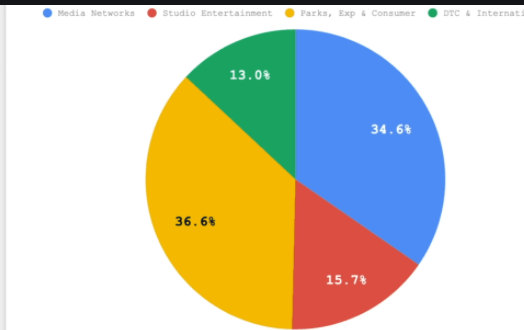

Disney is far more complex, spanning movie and animation studios, broadcasting networks, content networks, theme parks, hotels, merchandise and video streaming operations.

Think of Netflix as a content distributor, much as cable TV, satellite and telco video service providers; movie theaters; TV or radio broadcasters and increasingly, many online services and apps now act. True, Netflix invests heavily in original content, as do some other leading streaming video services. But its direct revenue comes solely from subscriptions.

Notice something about Disney, though. Direct-to-consumer, which includes the Disney streaming service, with 73 million paid subscribers, generates significant revenue, but negligible operating income. Granted, that is partially because the Covid-19 restrictions closed the theme parks, while Disney’s streaming service is in start-up mode, so operating income might not be expected for a bit.

In a non-Covid environment, the theme parks (which includes hotels and merchandise) contribution to operating income would be vastly higher, between 20 percent and 33 percent of revenue.

Operating income from theme parks, hotels and merchandise might range as high as 37 percent.

The point is that direct-to-consumer, lead by the streaming networks, should ultimately produce significant cash flow and operating income for Disney. The issue for some is how that cash flow and income might affect Disney value, and whether some different legal status for direct-to-consumer might affect the value of that unit.

To be sure, some are unsure Disney streaming businesses can approach the size of Netflix, which already has perhaps 201 million million subscriptions. All Disney streaming properties collectively might reach about 100 million subscriptions.

So the question is whether, someday, the value of Disney streaming is such that those assets would fetch a higher valuation if independent, as is Netflix.