Most mature markets feature a rule of three or a rule of four. “A stable competitive market never has more than three significant competitors,” BCG founder Bruce Henderson said in 1976. That often means the top-three providers have market share in the 70 percent to 90 percent range.

The rule of four refers to the expected market share in a stable market, where leader market share is twice that of provider number two, and where the number-two supplier has double the share of the number-three provider.

That creates a stable market share structure of 4:2:1. It arguably is stable because there is little incentive for either number one or number two to disrupt the market by attacking to gain share.

All of that explains the periodic waves of anti-trust action we see in many markets. Though there seems to be non-existent interest in anti-trust in the cloud computing “as a service” markets, some speculate it could eventually happen.

The issue is that such regulatory action never lasts. Competitive markets will revert to the rule of three or rule of four structure again. Look at U.S. telecommunications, where a former monopoly by AT&T was ended in 1982, creating eight new contestants instead of one AT&T.

What do we see some 40 years later? Essentially the rule of three. The rule of four is not yet in place, though.

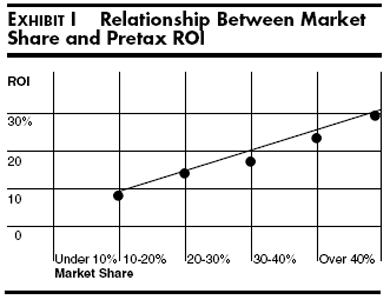

There also generally is a direct relationship between market share and profitability. Some note there is a similar return on sales and market share relationship.

source: Marketing Science Institute

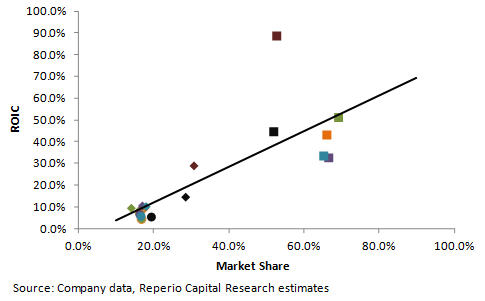

The point is that it is reasonable to expect that profits are directly related to market share, with a pattern where the leading three firms have something like a 40-20-10 share pattern, or perhaps 35-17-8 pattern.

Source: Reperio Capital

That pattern is--contrary to often-made claims--not a result of lack of competition, but instead evidence that competition exists. Competition means buyers gravitate to the perceived better products. That, in turn, leads to market share gains.

At some point, it is in the self interest of contestants not to wage ruinous price wars. Such wars depress earnings and profit margins for all contestants, but rarely change the relative standings. The more-profitable leader can absorb the losses more easily than the less-profitable attackers in second or third place.

Anti-trust action rarely, if ever, results in permanent change.