Few observers, it seems, are completely happy with the state of home broadband maps. Some argue the maps distort availability by as much as 21 percent. Others argue the degree of distortion likely is less than many believe, perhaps on the order of five percent, according to an analysis by George Ford, Phoenix Center for Advanced Legal and Economic Public Policy Studies chief economist.

Others note that the lack of access to fixed network “broadband internet access” at a minimum of 25 Mbps is between five percent and six percent. If satellite access is included in the analysis then virtually all continental U.S. locations have access to service at 25 Mbps.

Inaccurate maps are only part of the story, however. U.S. population density is quite thin across most of its geography. That directly affects the cost of building broadband networks, as hefty subsidies are required to reach the last one percent or two percent of remote locations.

And the United States has a huge percentage of its land mass that is thinly settled, if at all settled.

In Canada, 14 percent of the people live in areas of density between five and 50 people per square kilometer. In Australia, 18 percent of people live in such rural areas.

In the United States, 37 percent of the population lives in rural areas with less than 50 people per square kilometer.

Put another way, less than two percent of Canadians and four percent of Australians live in such rural areas. In the United States, fully 48 percent of people live in such areas.

Coverage is an issue in such rural areas. About six percent of the U.S. land mass is “developed” and relatively highly populated. Those are the areas where it is easiest to build networks.

But about 94 percent of the U.S. land surface is unsettled or lightly populated, including mountains, rangeland, cropland and forests. And that is where networks are hardest to build and sustain.

Industry statistics often suggest coverage is far better than critics say. The reality is likely that the maps are faulty, but coverage is still far better than some believe.

The Federal Communications Commission says 98 percent of U.S. homes have access to internet access at a minimum of 25 Mbps and 84 percent subscribe. Critics say those numbers are inflated by bad maps.

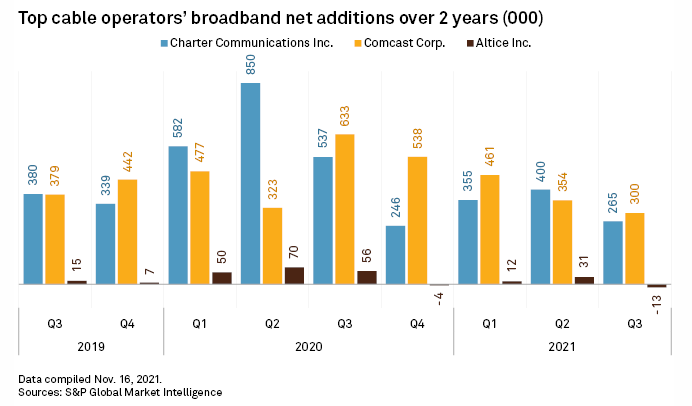

But one virtually never hears complaints that the leading U.S. cable companies do not, in fact, supply 500 Mbps (Charter Communications to 0gigabit internet access (Comcast) to nearly 100 percent of their customer locations. Add in Cox Communications and those three firms cover more than 75 percent of U.S. homes. Cox supplies gigabit access to 100 percent of its customer locations.

Gigabit speeds now are available to more than 88 percent of all U.S. homes, according to the Federal Communications Commission. Other estimates peg the percentage of homes with cable high-speed access at 90 percent.

One can disagree with the FCC statistics and still not quibble that cable operators generally do supply coverage within their franchise areas that is substantially at 100 percent and offering speeds between 500 Mbps and 1 Gbps.

Consider rural telco networks. “Respondents to this year’s survey report an average of 4,467 residential and 469 business fixed broadband connections in service,” NTCA says, with an average of 7,581 serviceable locations.

Respondents report an average of 72 percent of customers in their areas subscribe to a broadband service of some speed.

“On average, three-quarters (75.0 percent) of serviceable locations are served by fiber to the home (FTTH) in 2021; this is an increase of 5.1 percentage points from the prior year’s survey, says the latest Broadband/Internet Availability report issued by NTCA says.

An average of 15 percent of locations continue to be served via copper loops while fiber to the node (FTTN) is used to serve an average of six percent serviceable locations. Cable modems service 2.7 percent of locations, licensed fixed wireless 0.7 percent and unlicensed fixed wireless 0.6 percent of locations.

source: NTCA

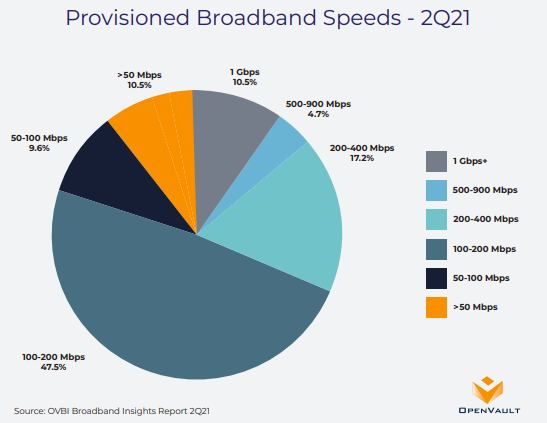

As for maximum speeds 55 percent of locations can get speeds between 100 Mbps but less than 1 Gbps. Some 20 percent of locations have maximum speeds between 25 Mbps and 100 Mbps.

Some 10 percent of locations have maximum speeds between 10 Mbps and 20 Mbps. About 3.7 percent of locations get speeds below 10 Mbps.

To be sure, the data is self reported. One might argue that firms that did not respond to the survey have coverage, speed or physical media attributes quite different from firms that did report.

Still, coverage in rural areas might be less a problem that generally is talked about.