This I did not see coming. AT&T will spin off AT&T’s interest in WarnerMedia to AT&T shareholders. I had assumed AT&T would retain its 71 percent interest in WarnerMedia.

In doing so, AT&T will shrink--in terms of equity value--to the fourth-biggest connectivity firm, behind Verizon, Comcast and T-Mobile.

I was wrong about AT&T’s “exit” from content. The characterization of AT&T’s merging of WarnerMedia assets with Discovery has been called a strategy shift that gets AT&T out of the content business. I had been characterizing it as AT&T monetizing part of the asset, since it still owned 71 percent.

But by spinning out the interest in a tax-free transaction--along with the shifting of DirecTV to a private equity joint venture--AT&T really is getting out of the content business.

Should AT&T also decide to spin out its interest in DirecTV, it will shrink even further, in terms of equity value.

It is at least the second big strategic shift we have seen AT&T make over the past three decades. Each time, there was a retreat, but arguably because the debt load associated with the strategic moves was burdensome.

Consider AT&T’s big move into cable TV in the mid-1990s, a time when the long distance provider was seeking a way to reenter the local access business with its own facilities. The thinking at that time was that a largely one-way cable TV plant could be upgraded to become full communications facilities, supporting home broadband and voice.

Given that development by virtually all cable TV companies in North America and Europe, the thinking was sound.

AT&T also made its first investment in DirecTV in 1996, owned and spun off Liberty Media.

Beside TCI, at that point the largest U.S. cable company, AT&T also bought Teleport Communications Group, a $500-million-a-year local business phone company, for $13.3 billion; MetroNet, a Canadian phone system, for $7 billion; and the IBM Global Network, which carries data traffic, for $5 billion. He also signed a joint venture with Time Warner ( to carry phone calls over the entertainment conglomerate's cable TV systems, and with British Telecom to serve multinationals overseas.

But the debt burden was too high and AT&T reversed course in 2004 and sold most of those assets. AT&T Broadband (the former TCI and US West Broadband assets) were sold to Comcast, making that firm the biggest U.S. cable TV company.

By 2005 AT&T itself was acquired by SBC Communications, which promptly rebranded itself AT&T.

AT&T's move into content with the full acquisition of DirecTV and Time Warner content assets was the second big diversification move AT&T has attempted since the mid-1990s.

AT&T spent about $170 billion since 2015, including taking on new debt, to transform itself into a media conglomerate.

By spinning out WarnerMedia, AT&T will shrink in equity value to about $130 billion. That is shocking in some ways. Verizon is valued at about $232 billion, Comcast at $262 billion and T-Mobile at $175 billion.

Beyond all that, one wonders what big tier-one carriers are going to do to keep revenue growing, given the pressures on their core businesses, and especially if they decide to retrench on their core businesses.

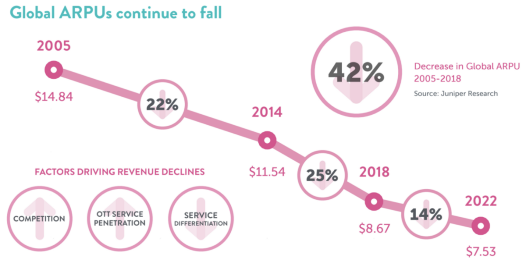

Growth rates are low and average revenue per user or account is flat to dropping.

source: Statista

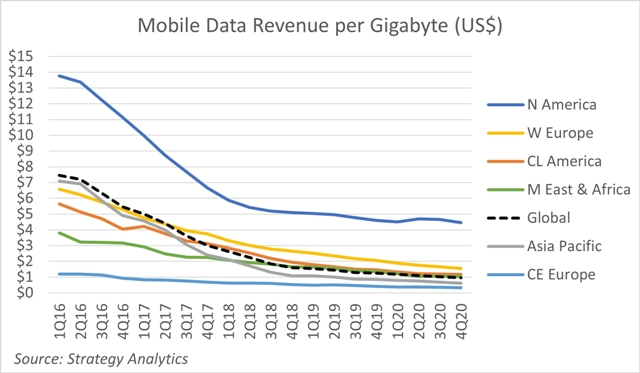

Especially important is mobile data ARPU, as mobility drives global revenues, while mobile internet access drives revenue growth.

source: Strategy Analytics

The declining ARPU poses revenue growth constraints in any market where subscriber penetration is close to saturation (every customer who wants to have a mobile account already has one).

source: Telefonica

And falling ARPU is a trend in both mobile and fixed network domains, though some hope the declines in mobile ARPU can be arrested.

source: Researchgate

Still, some think it is possible that revenue in the mobile industry could have peaked in 2021. That might be unduly pessimistic. Still, many expect flattish global revenue, going forward.

source: Statista

The strategy implications of another AT&T retreat from diversification are basically the fundamental problems the industry has been dealing with for some time. Where can growth be found, especially if one assumes service providers will largely stick to connectivity services?

Perhaps the better way to characterize the issue is to ask “where can growth be found within the connectivity realm at a level high enough to stay ahead of inflation?” Perhaps we ought to simply acknowledge that the public communications business remains a slow-growth industry that is challenged by disruptors of many sorts.

Perhaps “growth” needs to be framed in a modest way: enough revenue growth to replace lost revenues from declining product segments while staying ahead of inflation.