“If you look at what we do on a daily basis as it relates to connectivity, that's increasingly getting commoditized,” says Christopher Stansbury, Lumen Technologies EVP. “So that's not an interesting ending to the story.”

Which is why Lumen and just about everyone in the business always talks about, and strives, for “value add.” Here’s the problem: for at least 25 years, industry leaders have been telling that story and trying to execute on the vision.

One might conclude that nothing really has worked.

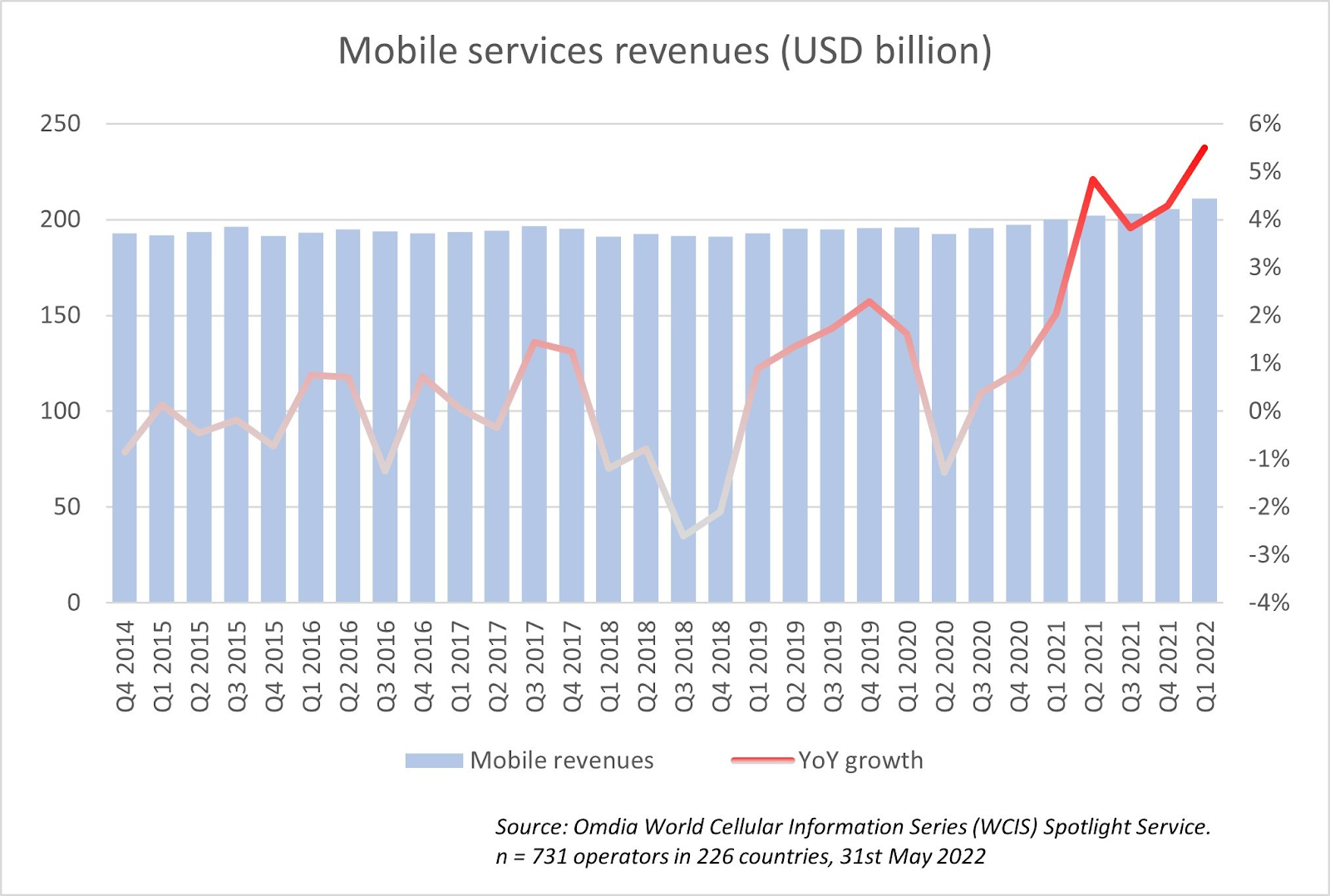

The answer is not simple. Connectivity providers have successfully added new lead revenue drivers. Mobile subscriptions now drive global revenue. Revenue growth often is driven by getting customers to add mobile internet access services; to shift up to more-expensive plans; or do the same with home broadband.

In past decades, expansion into new geographies has staved off revenue decline, as has asset acquisitions to bolster scale.

The key point is that the near evaporation of voice revenue was counteracted by shifting to home broadband, video services, mobility services, then mobile internet access, bundling of multiple services and enticing customers to buy more-pricey service plans.

It is not so clear we would characterize those as “value add” achievements. They are more on the order of creating new products to replace legacy products. That is arguably a bigger achievement than creating more “value add.”

To the extent there are other successes, they mostly might revolve around connectivity providers getting into new lines of business beyond connectivity. Some connectivity providers generate revenue from advertising, data center operations, content ownership or services, banking or payment services,

“Success” often depends on how one categorizes the value add or “new” revenue sources. Is mobile internet access a new service, or a value add? How about internet of things connections or cell tower backhaul? What about data center operations or cloud computing as a service?

IoT connections might be viewed as a value add. Data center operations or cloud computing might be better characterized as a new line of business. Mobile internet is a “new” service, but arguably a core business activity, not necessarily a value add or new line of business.

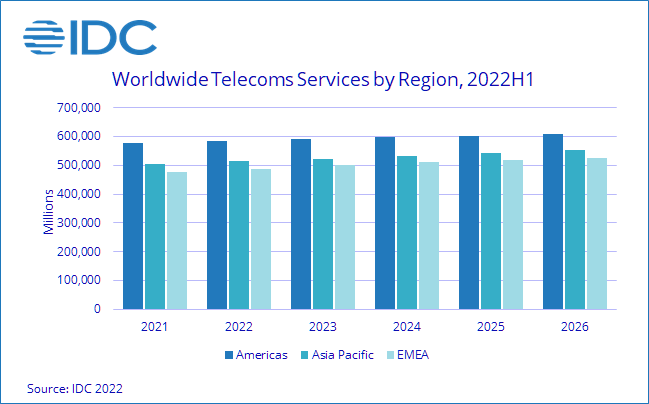

If one looks at global revenue figures, that observation might be concealed. After all, global growth these days is largely driven by net additions of mobile service accounts, with some contribution from home broadband account growth.

Globally, IDC sees perhaps two percent annual revenue growth for the global connectivity services market.

Most of that growth will come from more mobile service subscriptions, though average revenue per account is an issue.

Account totals will grow, but the problem is that average revenue per account is dropping, and has been almost the entire period during which competition has been encouraged in the connectivity business, starting in some markets in the 1980s.

All of that is important. “Commoditization,” or at least a trend of lower per-unit prices, is not likely something the industry can escape. But neither has the industry failed to create whole new product categories to replace lost legacy revenue.

Some have made a business of mobile payments, cloud computing or operating data centers or offering applications (consumer or business), even if global success is uneven.

We do not yet know how important internet of things, private networks, edge computing, application programming interface revenues or other products will become.