SoftBank is in final stages of talks with T-Mobile US parent company Deutsche Telekom about acquiring the U.S.-based wireless carrier, the Nikkei news service reports.

The acquisition, even if agreed to by both SoftBank and Deutsche Telekom, still faces an uphill battle for regulatory and antitrust clearance, many would say. On the other hand, a successful clearance of the merger likely would affect rules for upcoming 600 MHz auctions of former TV broadcast spectrum.

Both Sprint and T-Mobile US have argued for preferential bidding rules designed to allow both companies to acquire more lower-frequency spectrum. A merged Sprint and T-Mobile US should have a weaker argument for such bidding rules.

One big problem for the Federal Communications Commission is the rather complicated process to be used to first clear broadcasters out of spectrum, and then re-auction the cleared spectrum.

The trick is that broadcasters do not have to give up their spectrum. They might do so if the purchase price (with the FCC as the sole buyer) is high enough. But differential bidding rules will lower the value of the spectrum, and therefore tend to depress prices.

Lower prices make it less likely broadcasters will agree to sell their spectrum. So most observers agree that the highest payments would occur when there are no restrictive rules on the auctioning of spectrum in the follow-on process.

Setting aside blocks of spectrum that AT&T Mobility and Verizon Wireless cannot bid upon therefore make less likely the maximum amount of spectrum can be released.

A combined Sprint and T-Mobile US would suddenly emerge as a more credible alternative to either AT&T or Verizon, making any set-asides more questionable.

So the antitrust clearance process might be a bit more complicated than is typical. The U.S. Department of Justice already considers the U.S. mobile market unduly concentrated.

On the other hand, merger approval might then clear the way to hold an open auction with no set asides, thus making it more likely higher prices would be paid to broadcasters, thereby allowing the FCC to clear the most spectrum for the second stage auctions.

Wednesday, December 25, 2013

SoftBank Bid for T-Mobile US Could Reshape Thinking on 600 MHz Auction

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, December 24, 2013

Are Fixed, Satellite, Cable TV, Mobile Distinct Markets?

At some point, regulators and antitrust authorities will have to consider what the relevant market is for voice, Internet access and even video services, when attempting to make public policy judgments about potential mergers and acquisitions in the U.S. communications and video entertainment markets.

At some point, regulators and antitrust authorities will have to consider what the relevant market is for voice, Internet access and even video services, when attempting to make public policy judgments about potential mergers and acquisitions in the U.S. communications and video entertainment markets.

The reason is simply that it is becoming harder to justify regulating voice, video entertainment and Internet access services as distinct industries, when all three services already are offered by providers operating in at least three distinct regulatory frameworks.

Potential blockbuster mergers in the U.S. mobile business, cable TV industry and possible satellite video industry might loom in 2014.

Indeed, some would say huge proposed transactions challenging traditional notions of market dominance and market share are almost inevitable.

Trends are most advanced in the voice and Internet access business, while market share in the video entertainment business also will become even more competitive.

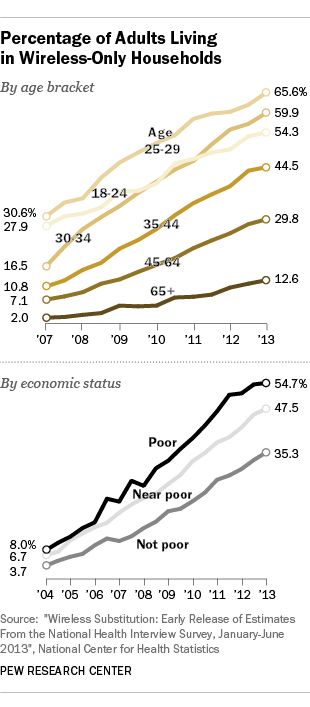

In the second half of 2012, 38 percent of U.S. households used mobile phones exclusively for voice communications. In most areas, some 11 percent to 19 percent “mostly” used mobiles for voice, even when a landline connection was available, according to the latest data from the

And among households of users 25 to 29, mobile-only rates already are at 66 percent.

Among users 30 to 34, some 60 percent of households are mobile only. Among households headed by people 18 to 24, 54 percent of homes are mobile only.

If the rates of mobile substitution continue as they have in recent years, in 2013 the percent of U.S. households that are “mobile only” for voice will have reached 40 percent, growing to 42 percent by the middle of 2014.

If the rates of mobile substitution continue as they have in recent years, in 2013 the percent of U.S. households that are “mobile only” for voice will have reached 40 percent, growing to 42 percent by the middle of 2014.

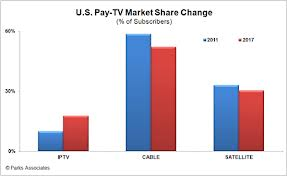

In the video subscription business, market share also continues to shift in the direction of telcos, the newest suppliers, while cable share drops and satellite share is stalled.

In both the voice and Internet access businesses, market share is dominated by telcos and cable providers, but with one notable caveat.

In both those businesses, huge amounts of share would be claimed by mobile service providers, if voice and Internet access were not regulated by distinct cable TV, telco and mobile rules.

Those facts might eventually play a role in regulator and competition authority evaluation of the state of competition in the voice services market. One might argue that mobile voice now is the preferred way most consumers consume voice services because the value-price relationship is better than that of fixed network voice.

At some point, mobile video entertainment or Internet access could attain similar advantages.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, December 23, 2013

What's Upside for AT&T Gigabit Networks?

Just how AT&T will fare, financially, by selling 1Gbps service in the Austin, Texas market is a fair question. Similar questions were asked about the Verizon Communications FiOS deployment as well.

As shareholder friendly as AT&T has been, some will begin to worry about the potential impact of a widespread gigabit network deployment, and that is a reasonable concern, especially given the $70 a month retail price, essentially dictated by Google Fiber's $70 a month price point.

Some of us who have watched fixed network service providers grapple with the loss of voice revenues will see a pattern that essentially means revenue and profit upside from the access service will be rather modest.

Many years ago, one telco pondering fiber to the home essentially cited strategic reasons for the investment, even if "traditional return on investment" rationales were tough to justify.

In essence, the argument was that the investment had to be made so that the telco could swap market share with the local cable operator. Essentially, the telco would gain video entertainment revenues, while the cable company took voice customers, while the two competitors split the high speed access market.

Some of you may have heard the quip, in answer to the question "what's in it for me?" that "you get to keep your job."

Basically, that was the strategic rationale for fiber to the home. The telco would remain in business. Perhaps that will provide scant comfort for investors. But the logic remains fundamentally sound, if not a recipe for huge increases in new revenue and profit margin.

In the end, AT&T might find it faces a similar challenge, as did Verizon Communications. To the extent a fixed network access service has value in the future, it will be as the provider of the highest bandwidth, lowest cost per bit Internet access service.

That doesn't mean, and likely cannot mean, that the Internet access service, or even voice and video entertainment are sufficient revenue drivers in the future. But the highest bandwidth, with the lowest cost per bit, will be the foundation.

No, it might not provide the highest absolute return on investment. But AT&T will be able to keep its business.

As shareholder friendly as AT&T has been, some will begin to worry about the potential impact of a widespread gigabit network deployment, and that is a reasonable concern, especially given the $70 a month retail price, essentially dictated by Google Fiber's $70 a month price point.

Some of us who have watched fixed network service providers grapple with the loss of voice revenues will see a pattern that essentially means revenue and profit upside from the access service will be rather modest.

Many years ago, one telco pondering fiber to the home essentially cited strategic reasons for the investment, even if "traditional return on investment" rationales were tough to justify.

In essence, the argument was that the investment had to be made so that the telco could swap market share with the local cable operator. Essentially, the telco would gain video entertainment revenues, while the cable company took voice customers, while the two competitors split the high speed access market.

Some of you may have heard the quip, in answer to the question "what's in it for me?" that "you get to keep your job."

Basically, that was the strategic rationale for fiber to the home. The telco would remain in business. Perhaps that will provide scant comfort for investors. But the logic remains fundamentally sound, if not a recipe for huge increases in new revenue and profit margin.

In the end, AT&T might find it faces a similar challenge, as did Verizon Communications. To the extent a fixed network access service has value in the future, it will be as the provider of the highest bandwidth, lowest cost per bit Internet access service.

That doesn't mean, and likely cannot mean, that the Internet access service, or even voice and video entertainment are sufficient revenue drivers in the future. But the highest bandwidth, with the lowest cost per bit, will be the foundation.

No, it might not provide the highest absolute return on investment. But AT&T will be able to keep its business.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sunday, December 22, 2013

Some Things Won't Change in 2014

Tactical challenges vary from year to year in the global telecom business. Strategic challenges tend not to vary much. Over the last 30 years, all markets have been transformed from monopoly to competitive businesses. So the key strategic context, in every market, is coping with relentless competition.

The “easy” answer to competitive threats is that service providers will find and develop new products that drive new revenues. So far, service providers have been able to do so. As high-margin international and long distance calling dwindled, mobile revenues have skyrocketed.

As aggregate voice and messaging revenues have begun to decline, Internet access and video entertainment revenue has grown. Virtually everybody believes mobile machine-to-machine (Internet of Things) revenues are the next big wave, though multiple bets on other sources are under active development.

But when revenue upside is tough, hard slogging, and the top line cannot easily be grown, a rational business will look to preserve profit margin by cutting costs.

One might argue there are two fundamental ways that operators can compensate for lower prices caused by competition.

They can get bigger, typically by acquiring other providers, to boost aggregate revenue. The other major operating area under their own control is costs. So in addition to acquisitions, firms try to cut costs, according to Strand Reports.

And those two approaches typically have a major advantage over the effort to develop new revenue sources: acquisitions and cost cutting affect the bottom line now.

“Lessons from the last 15 years of the premium SMS market show that mobile operators have limited ability to develop, market and sell the services demanded by customers,” says John Strang, Strand Research CEO. There are a couple obvious exceptions.

The shift from dial-up Internet access to broadband access clearly was important.

Where service providers essentially made very little incremental revenue offering dial-up services (it was fairly easy for independent competitors to sell the Internet app without providing the physical connection), access providers have tended to earn profit margins of 40 percent or more on broadband services, where independent providers have not been able to compete.

Also, mobile Internet access now is fueling mobile revenue gains, globally. In some markets, Long Term Evolution is boosting mobile Internet access revenues. But not everywhere. In some markets, LTE capital investment is not poised to create an opportunity for higher recurring revenue.

In some markets, LTE is not a premium product, and can be used with no price premium over 3G access.

Nor is it absolutely clear that faster fixed network access speeds necessarily or easily boost access revenues, either.

Some 65 percent of homes in Denmark can buy service at 100 Mbps, but only 0.7 percent do so.

That trend is broadly similar In countries such as Sweden, Belgium, and Netherlands. Even where triple-digit speeds are available, consumers often buy services that are not as fast, but still satisfy consumer needs.

Faster speeds are useful, and over time consumers have historically shown willingness to buy faster speed services. But faster Internet access might not be as popular a product as providers believe, unless the prices are substantially lower, a trend Google Fiber has almost singlehandedly begun in the U.S. market.

That is not to slight bandwidth pioneers or innovators, but only to recognize that big markets lead by big companies often are disrupted only by other big companies. Google, Amazon and Apple are key cases in point.

The point: while efforts to develop new products and revenue sources continue, the immediate impact on earnings will come from acquisitions and cost cutting. That will be true in 2014 as it is, every year.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Saturday, December 21, 2013

Cheaper to Manufacture in U.S. Than China, Firms Find

One of the biggest problems people and forecasters make is to extrapolate from current trends into the future.

But trends change. Consider textile manufacturing, once a staple in the U.S. Northeast and U.S. Southeast.

Rising costs have made it more expensive to spin yarn in China than in the United States, said Brian Hamilton, a 2012 doctoral graduate of North Carolina State University's College of Textiles, who wrote his Ph.D. dissertation on the global textile industry.

He found that in 2003, a kilogram of yarn spun in the U.S. cost $2.86 to produce, while it cost $2.76 to produce a kilogram in China. By 2010, however, it cost $3.45 to produce a kilogram in the U.S. and the cost in China had jumped to $4.13 per kilogram. U.S. production costs were lower than Turkey, Korea and Brazil.

Perhaps you have heard the phrase "and the last shall be first." Sometimes it happens in business.

But trends change. Consider textile manufacturing, once a staple in the U.S. Northeast and U.S. Southeast.

Rising costs have made it more expensive to spin yarn in China than in the United States, said Brian Hamilton, a 2012 doctoral graduate of North Carolina State University's College of Textiles, who wrote his Ph.D. dissertation on the global textile industry.

He found that in 2003, a kilogram of yarn spun in the U.S. cost $2.86 to produce, while it cost $2.76 to produce a kilogram in China. By 2010, however, it cost $3.45 to produce a kilogram in the U.S. and the cost in China had jumped to $4.13 per kilogram. U.S. production costs were lower than Turkey, Korea and Brazil.

Perhaps you have heard the phrase "and the last shall be first." Sometimes it happens in business.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Will T-Mobile US (and someday Sprint) Achieve Iliad Free Mobile Levels of Success?

Whether T-Mobile US ever will fully realize the fruits of its “Uncarrier” strategy to shake up the U.S. mobile industry is unclear, simply because T-Mobile US might not exist, as an independent company, in a couple of years.

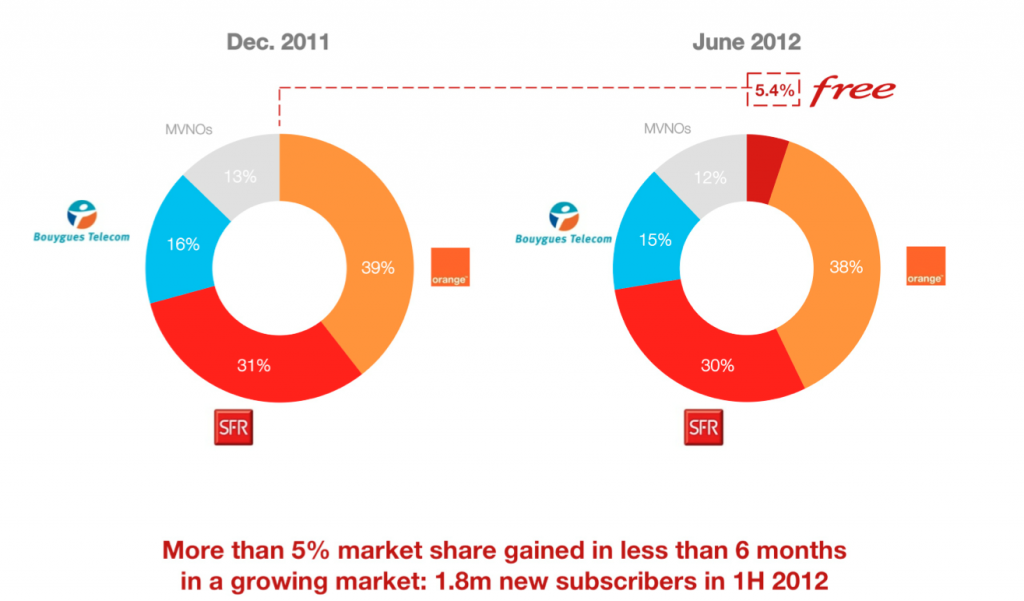

Also unclear is whether the “Uncarrier” strategy can be as successful an assault on market structure as SoftBank accomplished in Japan and that Illiad’s Free Mobile is doing in the French mobile market, namely, to significantly change both market share and industry pricing levels within two years.

In the two years since the Free Mobile launch in January 2012, mobile prices in France have fallen, in large part because the bigger incumbents have had to lower their retail prices. Orange, for example, in 2012 lowered mobile data prices on some packages by 60 percent, while increasing data allowances 300 percent.

Prices fell 11 percent in 2012 alone and are expected to have dropped eight percent to 10 percent in 2013.

Also, Free Mobile managed to get from zero market share to about six percent market share in about nine months of 2012. By early 2013 Free Mobile had grown to about eight percent share. At the end of 2013 Free Mobile appears to have 11 percent share.

That isn’t the first time Illiad has disrupted the French market. Iliad in 2002 launched its “Freebox” fixed network broadband service. What is different is the speed of disruption.

But by the end of its first year in service, Illiad Free had in December 2012 nearly as many subscribers as it has gotten for its fixed network service in 10 years.

At the end of December, 2012, Illiad had over 5.3 million broadband subscribers and 5.2 million mobile subscribers, representing market shares of over 24 percent in the French fixed network broadband business and almost eight percent in the mobile business.

Whether T-Mobile US would be able to, or will ever, gain 11 additional market share points in two years is the issue.

Whether T-Mobile US could gain 36 percent incremental market share over a decade, as Illiad has done in its fixed business, also is an issue.

In the first half of 2011, Iliad gained 36 percent market share of French broadband net additions, of which 80 percent were new subscribers opting for its new offer branded “Freebox Revolution,” and offering a triple play service (some might call it a quadruple play) including broadband Internet access, digital TV, gaming and a fixed phone line which includes unlimited calls to mobile phones on any domestic networks, for EUR29 (about $40) a month.

But Free’s disruption continues. Now Free Mobile plans to lease high-end smartphones to subscribers of its low-cost Free Mobile packages, a move that will hit squarely on the most-profitable part of the incumbent mobile service provider business.

Up to this point, Free Mobile has required that its subscribers buy their own phones, outright.

Up to this point, Free Mobile has required that its subscribers buy their own phones, outright.

Subscribers on Free Mobile 15.99 euro and 19.99 euro plans now can rent Samsung's Galaxy S4 for 12 euros a month over two years with an initial payment of 49 euros, or Apple's iPhone 5S for 12 euros a month and 99 euros up front.

Customers must return the phone after two years. In the U.S. market, most mobile virtual network operators have had the same "buy your own device" approach, in part because the cost of offering bundled phone plus contract service plans was too high.

Recently, U.S. providers have moved to "installment plans," eliminating the bundle, but still allowing consumers to buy their devices over time. Free Mobile now is moving to outright device rentals.

Recently, U.S. providers have moved to "installment plans," eliminating the bundle, but still allowing consumers to buy their devices over time. Free Mobile now is moving to outright device rentals.

Iliad's packages are different from the sales model used by its competitors, in which customers who sign two-year contracts of at least 20 euros a month receive an upfront subsidy worth 300 euros or more on a smartphone.

Iliad's lease offer represents a discount of about 40 percent on the cost of buying an iPhone 5S and then taking out a Free Mobile monthly plan.

Whether T-Mobile US or eventually Sprint can attack the U.S. market that aggressively remains to be seen. Whether T-Mobile US might try the "device rental" avenue is another good question.

So far we have moved from outright purchase to installment payment. Might rentals be next?

So far we have moved from outright purchase to installment payment. Might rentals be next?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, December 20, 2013

Internet Does Not Change the Fact that Most Communications are Relatively Local

A study by MIT professor Carlo Ratti, of MIT’s Department of Urban Studies and Planning, confirms that even in an Internet age, most communications occur within 100 miles of where people live.

The data for the United Kingdom shows that only about 9.5 percent of communications cross a line about 100 miles north of London.

In Italy, only 7.8 percent of communications cross a line roughly along the northern border of the Emilio-Romagna region, above which lie the industrial and commercial metropolises of Milan and Turin.

In the past, when voice was the only form of telecommunications, most calling likewise was local and regional.

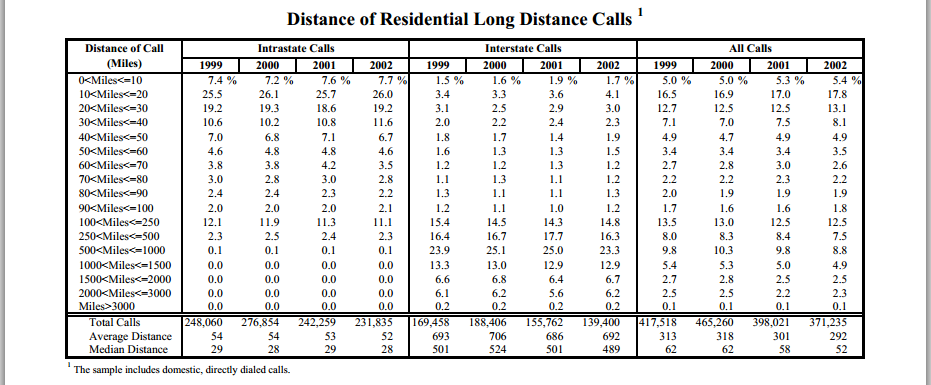

An analysis by the Federal Communications Commission, for example, looking at U.S. residential long distance calling from 1995 through 2002, showed a stable calling pattern where about 60 percent of long distance calling was intrastate, while 39 percent was interstate and international, combined.

But the key finding was the calling distance. The distance traveled by a typical call remained short, even long distance calls, and even within a continent-sized country.

Looking at all calls from 1999 to 2002, about half of all calls connect parties within 60 miles of each other and around 17 percent of toll calls are to parties only 10 to 20 miles distant.

About five percent of all residential calls terminated within 10 miles. Some 18 percent terminated more than 10 but less than 20 miles away.

About 13 percent of calls were placed to locations greater than 20 but less than 30 miles distant.

In other words, 36 percent of calls were to locations no more than 30 miles away.

And 61 percent of calls were to locations no more than 100 miles distant. Less than 19 percent of all calls were to locations 1,000 miles or more away.

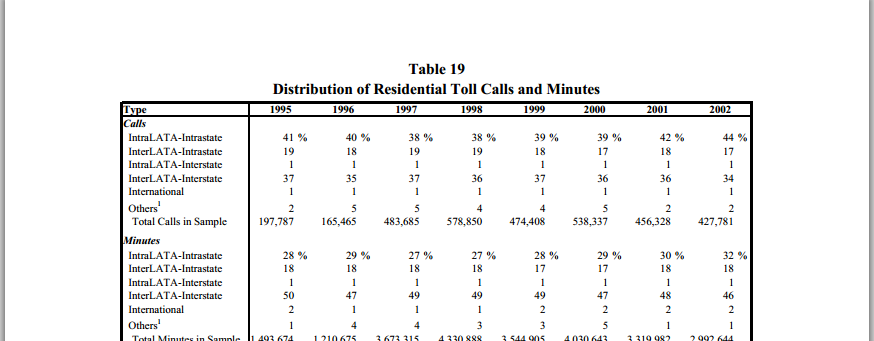

The notion of the "local access and transport area" (LATA) illustrates the concept. When the old AT&T system was broken up in 1984, 163 LATAs were created across the United States, each representing an average of 500,000 people, but in practice ranging from 10,000 to 10 million people.

Most LATAs were contained within a single state, but sometimes a LATA spanned two states. The point is that intra-LATA calling is a proxy for distance. Intra-LATA calls travel the shortest distances.

Typically, inter-LATA calls within the same state traveled further, while the greatest distances were typical of inter-LATA calls between states (or internationally).

In 2002, for example, about 44 percent of calls were placed intra-LATA and intra-state (within the same local calling area and within the same state).

About 17 percent of calls left one LATA, but were terminated within another LATA within the same state.

About 34 percent of calls were to another state. Only about one percent of calls were placed to international destinations.

Then, as now, most communications take place between people not too far distant, a likely reflection of the fact that most economic, social and other activity takes place locally or regionally.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Where Fixed Broadband Prices in Developing Nations Need to Go

Affordability is a key driver of service adoption, even when latent demand is high. That is especially true for fixed broadband access services in developing nations, where prices are dropping rapidly.

Affordability is a key driver of service adoption, even when latent demand is high. That is especially true for fixed broadband access services in developing nations, where prices are dropping rapidly.Where in 2008 the cost of a fixed network broadband connection represented as much as 165 percent of per-person income, since then, prices have dropped about 500 percent, according to International Telecommunications Union data.

Still, there is some distance to go. In developed nations, fixed network Internet access represents about 1.7 percent of per-person income. In developing nations, fixed network Internet access represents about 31 percent of per-person income.

That is why mobile Internet access widely is expected to represent the way most people in developing regions get access to the Internet. For fixed services to reach cost parity (in local terms), retail prices would have to drop another 18 times.

Prices lower by an order of magnitude is helpful. But prices might need to drop another two orders of magnitude to reach developed region levels. One might suggest that is unlikely to happen over the next decade or two.

It is far easier to envision mobile Internet access prices dropping by an order of magnitude over that period

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

2013 Not the Year Video Subscription Business Breaks

No prediction is required where it comes to expected 2014 price levels for video subscription services. They will rise. They always do.

No prediction is required where it comes to expected 2014 price levels for video subscription services. They will rise. They always do.

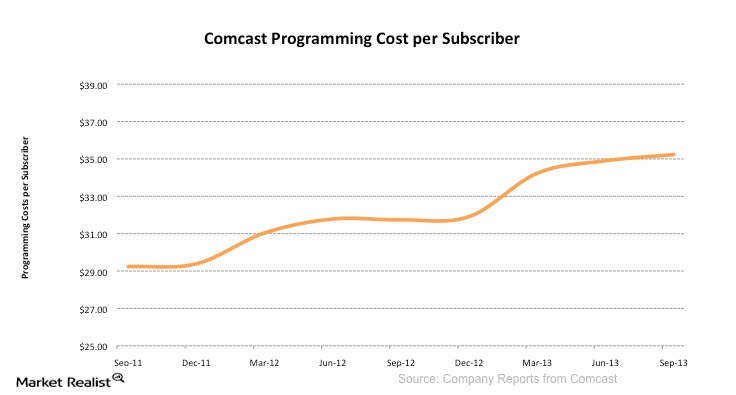

DirecTV hasn’t announced the precise amount of the increase, but something on the order of a four percent rate increase is logical, after an increase of 4.5 percent or so in 2013.

Comcast typically hikes prices about five percent a year. It is possible the aggregate 2014 rate hikes will amount to about three percent.

Comcast typically hikes prices about five percent a year. It is possible the aggregate 2014 rate hikes will amount to about three percent.

In 2013, Dish Network raised prices between seven percent and 20 percent. Another hike, of course, is coming in 2014. Some predict a price increase of about $5 a month, sometime in February 2014.

To be fair, those increases largely reflect increases in distributor programming costs. Time Warner Cable’s 2014 payments just to CBS will triple, some predict.

Some argue those annual price hikes, which consumers almost always say they object to, are the reason people slowly are falling out of the habit of paying for traditional video subscriptions.

Some argue those annual price hikes, which consumers almost always say they object to, are the reason people slowly are falling out of the habit of paying for traditional video subscriptions.

There is a more dangerous explanation, though. Many younger users find they do not appreciate the product enough to buy it, even when the actual price is really not the barrier.

But higher prices eventually are going to convince greater numbers of people they can do without the subscriptions, and substitute other behaviors, especially as it is easier to display Internet-delivered content on a standard TV.

To be sure, a major change in buying habits likely will not happen until people can buy, at prices they believe are reasonable, much of the content they now expect to view when they buy a video entertainment subscription. That is a ways off, it would seem.

But pressure slowly is building. That doesn't mean an immediate collapse of the current model. But neither would it be unrealistic to predict that, at some point, a major disruption will happen.

But pressure slowly is building. That doesn't mean an immediate collapse of the current model. But neither would it be unrealistic to predict that, at some point, a major disruption will happen.

Typically, major changes in consumer behavior happen rather suddenly, when a better alternative to a desired existing product emerges. Globally, there was an inflection point reached sometime early in the 1990s.

An analogy from the mobile adoption rate in most developing markets provides another example.

An analogy from the mobile adoption rate in most developing markets provides another example.

About 2003, an abrupt change in buying and adoption occurred. The video subscription business can be likened to the long period prior to 2003. The change, in other words, will be discontinuous, not gradual and linear.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

The Year Broadband Access Prices Were "Destroyed"

Major Internet service providers long have argued that demand for very high speed Internet access (50 Mbps, 100 Mbps, 300 Mbps and faster) is limited. For a very long time, those ISPs have had the numbers on their side.

Take rates, a measure of consumer demand for very high speed Internet access services, have historically been rather limited in the United States.

Major ISPs would have been on firm ground in arguing that most consumers were happy enough with the 20 Mbps to 30 Mbps speeds they already were buying, and that demand for 50 Mbps, 100 Mbps, 300 Mbps or 1 Gbps services were largely limited to business users or early adopters.

But something very important changed in 2013, namely the price-value relationship for very high speed Internet access services. Previously, where triple-digit speeds were available, the price-value relationship had been anchored around $100 or so for 100 Mbps, each month.

In the few locations where gigabit service actually was available, it tended to sell for $300 a month.

Then came Google Fiber, resetting the value-price relationship dramatically, to a gigabit for $70 a month. Later in 2013, other providers of gigabit access lowered prices to the $70 a month or $80 a month level, showing that Google Fiber indeed is resetting expectations.

Sooner or later, as additional deployments, especially by other ISPs, continue to grow, that pricing umbrella will settle over larger parts of the market, reshaping consumer expectations about the features, and the cost, of such services.

An analogy: in the past, voice service was the basic offer, while “voice mail” was a separate add-on. These days, it is inconceivable that a standard voice service comes without voice mail.

To be sure, instant messaging and over the top VoIP services do not routinely include the equivalent of “voice mail.” But the price-value relationship there also is quite different. People expect to use those services, much of the time, for no incremental cost. So despite the fact that a store-and-forward messaging capability is not available, the retail price also reflects the difference: no messaging, but also no incremental cost.

For a “paid” service, voice mail has to be included in the basic product.

The big change in 2013 was that the high end of the Internet access or broadband access market was fundamentally reset, even if the practical implications will take some time to be realized on a fairly ubiquitous basis.

Google Fiber’s 1 Gbps for $70 a month pricing now is reflected in most other competing offers, anywhere in the United States.

And those changes will ripple down through the rest of the ecosystem. Where Google Fiber now offers 5 Mbps for free, so all other offers will have to accommodate the pricing umbrella of a gigabit for $70 a month.

Be clear, Google Fiber has sown the seeds for a destruction of the prevailing price-value relationship for Internet access.

Eventually, all consumers will benchmark what they can buy locally against the “gigabit for $70” standard. And those expectations will affect demand for all other products.

Where alternatives are offered, many consumers will opt for hundreds of megabits per second at prices of perhaps $35 a month, because that satisfies their needs, and is congruent with the gigabit for $70 pricing umbrella.

One might also predict that, on the low end, 5 Mbps will be seen as a product with a retail price of perhaps cents per month.

Someday, we will look back and likely see 2013 as the year broadband access prices started to be “destroyed” (one way of looking at matters) or “reshaped” (the way Google looks at it).

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Who gets to use spectrum, and concerns about interference from other users, now appears to be an issue for Google’s Project Loon in India. ...