It still remains to be seen whether mobile banking will be a widespread, or simply a niche business, for mobile operators. In regions where retail banking is well developed, it is likely to be a niche dominated by financial providers. In regions with undeveloped banking infrastructure, mobile banking is going to be more important.

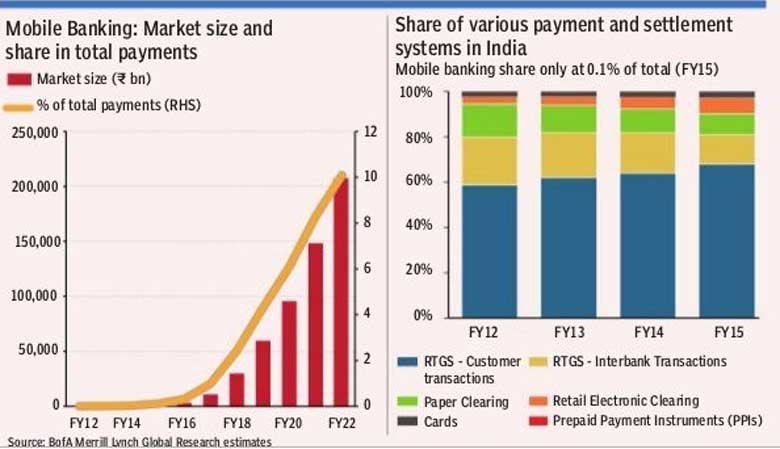

So far, in fact, mobile operator involvement in mobile banking has failed to get traction. That is not th case in other markets, such as regions of Africa where M-Pesa operates. In India, mobile banking is about to get a big boost, as well.

Airtel M-Commerce Services, which presently provides money transfer services in 800 towns in India, has been renamed Airtel Payments Bank, and also now plans to use the Airtel network to deliver banking services from 1.5 million outlets covering 87 percent of India’s population..

Kotak Mahindra Bank also has acquired 19.90 percent stake in Airtel Payments Bank.

Though not every tier-one access provider will inevitably become a supplier of banking services, many, in areas where the retail banking system is undeveloped, will do so. In some cases, that will take the form of remittances and payments. In other cases, a wider range of traditional banking operations will be supported.

In other instances, mobile operators might seek roles in retail payments as well.

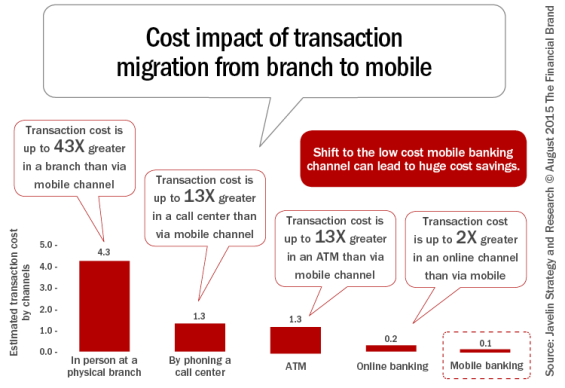

Mobile operations in core banking activities are important less for revenue upside than for cost reduction in some countries where banking systems are robustly developed. Cost savings and better customer quality of experience are the drivers in such markets, not “branch bank coverage.”

In fact, it might also be correct to say the shift in virtual banking in developed nations, is from online capabilities to mobile interactions, from retail payments to customer service functions, account balance checking and balance transfers.