Monday, June 11, 2012

Answer, Send to Voicemail, Reply with Message, Remind me to Call Back Later

Apple's latest operating system roughly doubles the typical inbound call handling options most people will use, especially for those of you who, for any reason, think call waiting is not something to be used.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple has 400 Million Payment Accounts

Apple now has 400 million active payment accounts, according to Apple CEO Tim Cook. That doesn't necessarily mean Apple is interested, at the moment, in doing much beyond supporting content payments on its own devices.

Apple now has 400 million active payment accounts, according to Apple CEO Tim Cook. That doesn't necessarily mean Apple is interested, at the moment, in doing much beyond supporting content payments on its own devices.But all of those 400 million active accounts have active credit cards that can be used on iTunes and the App Store.

PayPal has 110 million active accounts and Amazon.com has 152 million customer accounts.

At least for the moment, Apple seems content to use its payment system in a closed-loop way, as does Starbucks.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple's iOS 6 Will Launch Apps on iPads

Apple's iOS 6 mobile operating system will be made available on iPads, and will include the ability to its launch apps, Apple says. Siri now also answers real-world questions about sports, movies and restaurants.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Does it Mean that "Cloud Computing" is Growing 28% a Year?

Cloud computing was the fastest-growing category of U.S. service provider infrastructure spending in 2011, with a 28.4 percent increase, according to the Telecommunications Industry Association.

The TIA also expects cloud computing will continue to be the fastest-growing category of network and facilities investment during the next four years, averaging 20.3 percent compounded annually.

But it is end user spending that arguably drives most of the revenue, so one might argue that much of the opportunity will be reaped by firms that sell enterprise applications, not firms that sell infrastructure services more centrally related to hosting, for example.

TIA argues that end user spending on cloud apps will more than double to $12.1 billion in 2015 from $5.8 billion in 2011, according to the TIA. Separating out what that could mean for providers of cloud “data center facilities” is harder to assess.

In fact, most of the revenue upside appears likely to accrue to hardware and software suppliers, at least initially, according to a Morgan Stanley analysis.

In the infrastructure end of the business, telecom service providers might make a business out of rental of computing cycles, storage and ancillary services. But what has to be done to market and support that business, and should effort be put elsewhere?

In the telecom space, the analysts expect key winners to include Rackspace, Equinix and competitive local exchange carriers and metro bandwidth suppliers. In other words, hosting and access will be where the telecom revenue lies, possibly not in the infrastructure, platform or software as a service businesses.

The point is that assessing cloud computing revenue contributions for various ecosystem participants is complicated.

That forecast suggests why cloud computing initiatives by telcos will have to be targeted. There actually isn’t as much revenue in cloud computing as some tend to think. Nor is the space uncontested.

Companies such as Google, Amazon Web Services, Hewlett-Packard Development Co., Microsoft Corp. and Salesforce.com are themselves already leaders in the cloud infrastructure space, and already are displacing traditional infrastructure outsourcing alternatives, one might argue.

North America, specifically the U.S., currently represents the largest opportunity for SaaS, and it is the most mature of the regional markets. SaaS software revenue is forecast to total $9.1 billion in 2012, up from $7.8 billion in 2011.

But keep in mind that most of that revenue is earned providing expense management, financials, email and office suites. Though Web conferencing also is a SaaS application, few telcos are players to any major extent.

In Western Europe, SaaS revenue is forecast to surpass $3.2 billion in 2012, up from $2.7 billion in 2011, while SaaS revenue is Eastern Europe is projected to reach $169.4 million, up from $135.5 million last year.

SaaS revenue in Asia/Pacific is on pace to reach $934.1 million in 2012, up from $730.9 million in 2011.

SaaS revenue in Latin America is forecast to total $419.7 million in 2012, up from $331.1 million last year. None of those revenue streams are terribly large, by tier one service provider standards, nor are telcos the most logical providers.

In addition to the possibility that cloud-delivered enterprise apps compete most centrally with distributors of "shrink wrapped" apps, it can be argued that cloud infrastructure also competes with traditional "outsourcing" services.

Cloud infrastructure services are an alternative to traditional IT outsourcing services, often reducing the IT costs of their clients by at least 40 percent, according to livemint.com.

Likewise, you might argue that enterprise or other "app stores" might also compete with other software delivery channels.

What you will note about the enterprise app store concept is that it disintermediates nearly all of the premises networking infrastructure. There is no need for the enterprise local area network, except perhaps to switch to Wi-Fi access at times.

You can imagine this will have serious implications for firms that traditionally make a living selling gear and services for enterprise LANs. Just as easily, you can see the upside for traditional communications providers who now could have an expanded role in the information technology business.

What products would be “natural” parts of a communications and information technology bundle? How much easier would it be for traditional telco sales organizations to sell key business software?

In fact, non-technical sales forces of all types might find there are new opportunities to sell products that might have been “too technical” in the past. Firms outside “IT” might find they can create bundles almost on the fly, customized for vertical markets or businesses of various sizes and types.

A shift to some new computing architecture based on cloud resources and mobility could have huge implications for any number of businesses in the information technology and communications businesses.

Although growing interest has been observed in vertical-specific software, the most widespread use is still characterized by horizontal applications with common processes, among distributed virtual workforces and within Web 2.0 activities.

Cloud computing will have implications for most firms in the business applications, information technology support and data center businesses. Whether that impact is large or relatively small is hard to say, at the moment.

The TIA also expects cloud computing will continue to be the fastest-growing category of network and facilities investment during the next four years, averaging 20.3 percent compounded annually.

But it is end user spending that arguably drives most of the revenue, so one might argue that much of the opportunity will be reaped by firms that sell enterprise applications, not firms that sell infrastructure services more centrally related to hosting, for example.

TIA argues that end user spending on cloud apps will more than double to $12.1 billion in 2015 from $5.8 billion in 2011, according to the TIA. Separating out what that could mean for providers of cloud “data center facilities” is harder to assess.

In fact, most of the revenue upside appears likely to accrue to hardware and software suppliers, at least initially, according to a Morgan Stanley analysis.

In the infrastructure end of the business, telecom service providers might make a business out of rental of computing cycles, storage and ancillary services. But what has to be done to market and support that business, and should effort be put elsewhere?

In the telecom space, the analysts expect key winners to include Rackspace, Equinix and competitive local exchange carriers and metro bandwidth suppliers. In other words, hosting and access will be where the telecom revenue lies, possibly not in the infrastructure, platform or software as a service businesses.

The point is that assessing cloud computing revenue contributions for various ecosystem participants is complicated.

That forecast suggests why cloud computing initiatives by telcos will have to be targeted. There actually isn’t as much revenue in cloud computing as some tend to think. Nor is the space uncontested.

Companies such as Google, Amazon Web Services, Hewlett-Packard Development Co., Microsoft Corp. and Salesforce.com are themselves already leaders in the cloud infrastructure space, and already are displacing traditional infrastructure outsourcing alternatives, one might argue.

North America, specifically the U.S., currently represents the largest opportunity for SaaS, and it is the most mature of the regional markets. SaaS software revenue is forecast to total $9.1 billion in 2012, up from $7.8 billion in 2011.

But keep in mind that most of that revenue is earned providing expense management, financials, email and office suites. Though Web conferencing also is a SaaS application, few telcos are players to any major extent.

In Western Europe, SaaS revenue is forecast to surpass $3.2 billion in 2012, up from $2.7 billion in 2011, while SaaS revenue is Eastern Europe is projected to reach $169.4 million, up from $135.5 million last year.

SaaS revenue in Asia/Pacific is on pace to reach $934.1 million in 2012, up from $730.9 million in 2011.

SaaS revenue in Latin America is forecast to total $419.7 million in 2012, up from $331.1 million last year. None of those revenue streams are terribly large, by tier one service provider standards, nor are telcos the most logical providers.

In addition to the possibility that cloud-delivered enterprise apps compete most centrally with distributors of "shrink wrapped" apps, it can be argued that cloud infrastructure also competes with traditional "outsourcing" services.

Cloud infrastructure services are an alternative to traditional IT outsourcing services, often reducing the IT costs of their clients by at least 40 percent, according to livemint.com.

Likewise, you might argue that enterprise or other "app stores" might also compete with other software delivery channels.

What you will note about the enterprise app store concept is that it disintermediates nearly all of the premises networking infrastructure. There is no need for the enterprise local area network, except perhaps to switch to Wi-Fi access at times.

You can imagine this will have serious implications for firms that traditionally make a living selling gear and services for enterprise LANs. Just as easily, you can see the upside for traditional communications providers who now could have an expanded role in the information technology business.

What products would be “natural” parts of a communications and information technology bundle? How much easier would it be for traditional telco sales organizations to sell key business software?

In fact, non-technical sales forces of all types might find there are new opportunities to sell products that might have been “too technical” in the past. Firms outside “IT” might find they can create bundles almost on the fly, customized for vertical markets or businesses of various sizes and types.

A shift to some new computing architecture based on cloud resources and mobility could have huge implications for any number of businesses in the information technology and communications businesses.

Although growing interest has been observed in vertical-specific software, the most widespread use is still characterized by horizontal applications with common processes, among distributed virtual workforces and within Web 2.0 activities.

Cloud computing will have implications for most firms in the business applications, information technology support and data center businesses. Whether that impact is large or relatively small is hard to say, at the moment.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Africa Mobile Market Fastest Growing in World

If you can remember 1970s and 1980s policy discussions in the global telecom community about how to provide basic telephone service to the billion or more people who had never made a phone call, you will be astonished at how powerful mobile services have been. A problem thought too expensive to solve now is well on the way to vanishing.

Africa, for example, is the fastest-growing mobile market in the world and the largest after Asia, according to the GSM Association.

The number of subscribers on the continent has grown almost 20% each year for the past five years, according to the GSM Association GSMA report on the African mobile market. The GSMA expects there will be more than 735 million subscribers by the end of 2012.

Among the changes mobility is bringing is a new access to banking services. Africa already has 51 mobile money systems in place, serving more than 40 million African users.

Africa, for example, is the fastest-growing mobile market in the world and the largest after Asia, according to the GSM Association.

The number of subscribers on the continent has grown almost 20% each year for the past five years, according to the GSM Association GSMA report on the African mobile market. The GSMA expects there will be more than 735 million subscribers by the end of 2012.

Among the changes mobility is bringing is a new access to banking services. Africa already has 51 mobile money systems in place, serving more than 40 million African users.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

iPad Owners will Double in 2012

For most people, it appears, an Apple iPad will remain the preferred tablet, despite growing numbers of Kindle and other devices being purchased.

For most people, it appears, an Apple iPad will remain the preferred tablet, despite growing numbers of Kindle and other devices being purchased.In fact, eMarketer predicts the number of iPad users in the US will rise by over 90 percent in 2012 to 53.2 million, as users replace older models and new consumers purchase the device. This year, the iPad will continue to be in the hands of more than 75 percent of all tablet users in the country, eMarketer predicts.

Of course, no product or service can sustain triple-digit growth forever, so the 2011 growth of iPad sales of 143.9 percent will slow over time. On the other hand, Apple does not appear likely to lose its commanding market share lead.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, June 10, 2012

Mobile, Web Commerce Use Drastically-Different Payment Methods

A study by ShopVisible suggests mobile payments use different methods than online payments.

Some 67 percent of customers used PayPal or an alternative payment method when buying something from their mobile, while 33 percent paid by credit card, a ShopVisible study of 23,000 transactions has found.

For Web transactions over the same period, the results were reversed, the study found. Some 62 percent of buyers paid by credit card, 12.9 percent by Amazon Payments, 8.1 used Google Checkout, and just 16.8 percent used PayPal.

It might be too early to extrapolate too much from the results. It probably remains the case that mobile shopping is for different products than online shopping.

It might be that a typical transaction amount is significant enough to influence the choice of payment method.

There could be other reasons why credit cards make sense for PC-based shopping. Perhaps entering a long string of credit card numbers is viewed as a feasible and convenient operation on a PC and not so much on a mobile, leading to a preference for payment methods that do not require such operations.

Some 67 percent of customers used PayPal or an alternative payment method when buying something from their mobile, while 33 percent paid by credit card, a ShopVisible study of 23,000 transactions has found.

For Web transactions over the same period, the results were reversed, the study found. Some 62 percent of buyers paid by credit card, 12.9 percent by Amazon Payments, 8.1 used Google Checkout, and just 16.8 percent used PayPal.

It might be too early to extrapolate too much from the results. It probably remains the case that mobile shopping is for different products than online shopping.

It might be that a typical transaction amount is significant enough to influence the choice of payment method.

There could be other reasons why credit cards make sense for PC-based shopping. Perhaps entering a long string of credit card numbers is viewed as a feasible and convenient operation on a PC and not so much on a mobile, leading to a preference for payment methods that do not require such operations.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, June 9, 2012

"Senior" Internet Gap is Smallish, Will Disappear

Some 60 percent of U.S. seniors are online, according to Forrester Research. While they trail behind younger generations when it comes to device ownership and online usage, their usage of apps is not dramatically different from younger demographics or Internet users as a whole.

The other problem is that "seniors" comprise a relatively smaller portion of the total U.S.population than you might think. Millennials and Generation X represent 46 percent of the total U.S. population. Younger boomers between 45 and 54 represent about 20 percent. Most people would not consider people in that age bracket to be "seniors."

Those 55 to 63 represent about 13 percent. You might, or might not, consider these people to be the "seniors" who don't understand or want to use the Internet. But think about whether you actually know many people that age who do not use the Internet. Many of us cannot think of anybody we actually know, in that age bracket, that does not use the Internet.

Most might agree that people 64 and above qualify as "seniors." But all those people, at any age 64 or older, represent about 18 percent, in total.

At some point, there will might not be many significant differences in Internet usage, in any demographic. Someday, all Millennials will be seniors.

The other problem is that "seniors" comprise a relatively smaller portion of the total U.S.population than you might think. Millennials and Generation X represent 46 percent of the total U.S. population. Younger boomers between 45 and 54 represent about 20 percent. Most people would not consider people in that age bracket to be "seniors."

Those 55 to 63 represent about 13 percent. You might, or might not, consider these people to be the "seniors" who don't understand or want to use the Internet. But think about whether you actually know many people that age who do not use the Internet. Many of us cannot think of anybody we actually know, in that age bracket, that does not use the Internet.

Most might agree that people 64 and above qualify as "seniors." But all those people, at any age 64 or older, represent about 18 percent, in total.

At some point, there will might not be many significant differences in Internet usage, in any demographic. Someday, all Millennials will be seniors.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

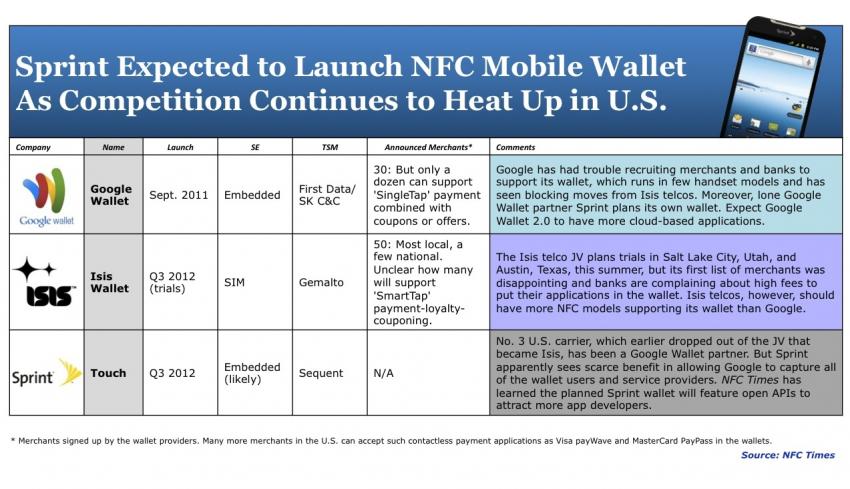

Slow Traction for Google Wallet Isn't Surprising

The possibility that Sprint is launching its own mobile wallet platform, and might, as part of that effort, have to displace Google Wallet on its devices, will add yet one more provider to a chaotic mobile wallet environment. Neither Google Wallet nor Isis, for example, have gotten significant traction yet, nor, in truth, should have that been expected.

Both Isis and Google Wallet require creation of a huge new infrastructure of near field communications point of sale terminals and end user devices, plus new end user behaviors and a clear value proposition. Those would be difficult under the best of circumstances.

Google will do what it always does: keep working on the next version. It is far too early to declare any long-term winners in the NFC mobile wallet business. Consumer adoption of important new technologies can take some time.

Products such as tablets can reach significant penetration rather quickly because the rest of the infrastructure, including widespread Wi-Fi, apps, end user behavior, business models, quality broadband (at least for purposes of supporting video apps, a key tablet app) and even familiarity with the touch interface are established.

Near field communications has almost none of the infrastructure requirements well established. For that reason, many of us would caution that patience is needed. It might take as much as a decade before there is significant penetration.

ATM card adoption provides one example, where "decades" is a reasonable way of describing adoption of some new technologies, even those that arguably are quite useful.

“Mobile proximity payments will remain in infancy for at least five years,” said Jim Van Dyke, Javelin Research president. In other words, payment systems based on near field communications, and others, might take that long to begin getting serious traction.

Both Isis and Google Wallet require creation of a huge new infrastructure of near field communications point of sale terminals and end user devices, plus new end user behaviors and a clear value proposition. Those would be difficult under the best of circumstances.

Google will do what it always does: keep working on the next version. It is far too early to declare any long-term winners in the NFC mobile wallet business. Consumer adoption of important new technologies can take some time.

Products such as tablets can reach significant penetration rather quickly because the rest of the infrastructure, including widespread Wi-Fi, apps, end user behavior, business models, quality broadband (at least for purposes of supporting video apps, a key tablet app) and even familiarity with the touch interface are established.

Near field communications has almost none of the infrastructure requirements well established. For that reason, many of us would caution that patience is needed. It might take as much as a decade before there is significant penetration.

ATM card adoption provides one example, where "decades" is a reasonable way of describing adoption of some new technologies, even those that arguably are quite useful.

“Mobile proximity payments will remain in infancy for at least five years,” said Jim Van Dyke, Javelin Research president. In other words, payment systems based on near field communications, and others, might take that long to begin getting serious traction.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, June 8, 2012

Facebook App Center Isn't a Store, It's a Discovery or Search Tool

Facebook's new "App Center" might sound like an app store, but it is not. Rather, the App Center is a way to encourage people to use Facebook-affiliated mobile apps, by helping them find useful and entertaining apps.

Facebook's new "App Center" might sound like an app store, but it is not. Rather, the App Center is a way to encourage people to use Facebook-affiliated mobile apps, by helping them find useful and entertaining apps. It's partly a discovery or search tool, partly an incentive for developers to work with Facebook and hence part of Facebook's effort to maintain its platform relevance.

It also is one example of how device and application providers now are orienting their businesses around a “mobile first” strategy.

Facebook says there are more than 4,500 separate applications that integrate with Facebook.

The company also took the opportunity to highlight the role it has played in driving mobile application sales. It has released statistics indicating that Facebook sent users to the Apple App Store 83 million times in May alone, and sent iOS users into installed applications 134 million times during the same month.

The App Center is rolling out immediately in the United States and will be made available to users in other countries over the next few weeks. It is intended to replace the Facebook website’s existing Apps and Games interface.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will Google, Apple, PayPal Ever Want to be Banks?

Will Google, Apple, PayPal and others ever decide there is a reason to become "banks?" The question might seem far fetched, except that once application and device firms decide payments and loyalty are businesses with direct implications for their existing businesses, it isn't so clear what other functions associated with "banks" might then seem reasonable as well.

Rogers Communications in Canada already has applied to become a formal bank. To be sure, that appears to be primarily for the purpose of providing credit, payment and charge card services. In one sense, the move is similar to any other large retail brand creating a branded charge card.

"We have no plans to become a full-service deposit-taking financial institution," Rogers Public Affairs Manager Carly Suppa said. "The license, if granted, would give us the flexibility to pursue a niche credit card opportunity to our customers should this make sense at a future date."

"People have already slowed their use of cash and checks in favor of credit and debit cards. Within five years, half of today’s smart phone users will be using their phones and mobile wallets as their preferred method for payments," argues Peter Olynick, Carlisle & Gallagher's Card & Payments Practice leader.

Keep in mind, he isn't saying Google, Apple, PayPal and many others immediately threaten the core banking function, just the parts of their business associated with payment operations.

A survey of 605 U.S. consumers found high receptivity, at least in principle, to use of mobile wallets for loyalty purposes. The same survey also found consumers conceptually also willing to use entities such as PayPal for core banking functions as well.

Once can be skeptical, without being dismissive, about the degree to which such sentiments might eventually become actual behavior. One might remain skeptical that the core banking function actually is attractive for application and device suppliers, or mobile service providers.

But in many African markets, mobile service providers have already in droves become authorized payment providers. You might not consider that banking so much as money transfer. But bill paying has become a more-important banking feature, at the very least, and money transfer is bleeding over broadly into bill paying, in Africa.

What seems unlikely or improbable today might not always seem outlandish. But a reasonable person might still bet against the likes of Google and Apple becoming banks in the common sense of the term, even if payments will be contested terrain.

Rogers Communications in Canada already has applied to become a formal bank. To be sure, that appears to be primarily for the purpose of providing credit, payment and charge card services. In one sense, the move is similar to any other large retail brand creating a branded charge card.

"We have no plans to become a full-service deposit-taking financial institution," Rogers Public Affairs Manager Carly Suppa said. "The license, if granted, would give us the flexibility to pursue a niche credit card opportunity to our customers should this make sense at a future date."

In other words, Rogers doesn't want to become a full-fledged retail bank. But becoming a credit card issuer does set Rogers up for a smooth transition to becoming a mobile payments provider in the future.

Credit cards present a distinct opportunity for Rogers to expand its reach, as the media, cable and wireless giant also owns the Toronto Blue Jays and has direct relationships with millions of customers, including many who pay bills using credit or direct-deposit accounts. So there is an incremental opportunity to capture some of the current transaction revenue, at the very least.

Beyond that, analysts say the company can build a broader card business by leveraging those relationships to market its brand of cards, especially by reaching out to customers who have good credit standing in its database. That would create a new revenue stream for the broader number of retail transactions for which its customers use credit cards.

"People have already slowed their use of cash and checks in favor of credit and debit cards. Within five years, half of today’s smart phone users will be using their phones and mobile wallets as their preferred method for payments," argues Peter Olynick, Carlisle & Gallagher's Card & Payments Practice leader.

Keep in mind, he isn't saying Google, Apple, PayPal and many others immediately threaten the core banking function, just the parts of their business associated with payment operations.

A survey of 605 U.S. consumers found high receptivity, at least in principle, to use of mobile wallets for loyalty purposes. The same survey also found consumers conceptually also willing to use entities such as PayPal for core banking functions as well.

Once can be skeptical, without being dismissive, about the degree to which such sentiments might eventually become actual behavior. One might remain skeptical that the core banking function actually is attractive for application and device suppliers, or mobile service providers.

But in many African markets, mobile service providers have already in droves become authorized payment providers. You might not consider that banking so much as money transfer. But bill paying has become a more-important banking feature, at the very least, and money transfer is bleeding over broadly into bill paying, in Africa.

What seems unlikely or improbable today might not always seem outlandish. But a reasonable person might still bet against the likes of Google and Apple becoming banks in the common sense of the term, even if payments will be contested terrain.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, June 7, 2012

Sprint Plans to Launch own NFC Mobile Wallet?

Sprint is planning to launch its own NFC mobile wallet as early as this summer, NFC Times reports. Sprint earlier had been the only U.S mobile service provider to support Google Wallet. The obvious question is whether this means Sprint will drop support for Google Wallet.

Sprint is planning to launch its own NFC mobile wallet as early as this summer, NFC Times reports. Sprint earlier had been the only U.S mobile service provider to support Google Wallet. The obvious question is whether this means Sprint will drop support for Google Wallet.Sprint apparently sees advantages in rolling out its own wallet, which according to the sources is named “Touch.” With a wallet, Sprint could build relationships with banks and other service providers.

“The limitation isn’t the wallet; the limitation is the secure element,” said a source at Sprint, who added the Sprint wallet offers a “legitimate alternative to Isis.” That rather suggests Sprint has to make a choice between its own offering and Google Wallet, as a wallet apparently needs control of the secure element used to authenticate users and credentials.

Some of you will want to shake your heads at the growing number of wallet platforms, not to mention payment systems. Market fragmentation always is quite high at the start of any new business expected to be sizable.

The emergence of more competitors "validates" the market, executives like to say. That might be true, but fragmentation also will slow adoption, to the extent that users have to lock into devices, service providers or exclusive apps.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Happens to Google Revenue as Apple Dumps Google Maps?

Most observers would probably guess that if Apple represents about 40 percent of Google mobile search ad revenue, and Apple stops offering Google Maps in favor of its own map application, that Google revenue will suffer.

Most observers would probably guess that if Apple represents about 40 percent of Google mobile search ad revenue, and Apple stops offering Google Maps in favor of its own map application, that Google revenue will suffer.But Piper Jaffray's Gene Munster predicts that Apple's decision to abandon Google Maps shouldn't have any "material impact" on the revenue Google gets from iOS.

Munster estimates that Google will generate about $4.5 billion in gross mobile revenue in 2012, the lion's share ($4 billion) from search ads and the rest ($500 million) from display.

He believes that iOS is likely to remain the biggest or close to the biggest source of that revenue, generating roughly $1.6 billion. Assuming Google keeps half (after subtracting acquisition costs), iOS would generate about two percent of Google's total revenue in 2012.

You might wonder how that could possibly be. Munster assumes Google Maps still will be available in the Apple app store, and that iOS device users will be able to figure out how to keep using it. Munster says Apple represents about two percent of Google's net revenue overall.

Google might hope Munster is right, but is acting as though the loss could be more significant. Google's recent addition of 3D features to Google Maps probably indicates Google's belief that Apple will try and use the 3D feature to differentiate from Google Maps.

Mobile ads associated with maps or locations are estimated to account for about 25 percent of the roughly $2.5 billion spent on mobile ads in 2012, according to Opus Research, up from 10 percent in 2010. That is reason enough for a battle over map applications.

The reason maps get so much advertising is that geo-location is a fairly serious indicator of purchase intent when a retailer is searched for, within a map app. That obviously has implications if you believe location-based advertising and offers are a big business opportunity.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Global Mobile Advertising Market: $5.3 Billion in 2011

Mobile advertising reached $5.3 billion (€3.8 billion) in 2011. You might call that a good start, but still quite a smallish business, by tier one mobile service provider standards. The reason is simply that an entity booking scores of billions worth of revenue each year would need a market opportunity far bigger than that to become "really interesting."

But mobile advertising is a new and growing business, so most observers think the market eventually will grow to a size that is truly significant for mobile service providers.

Of current revenue, Europe represents 25.9 percent; North America 31.4 percent; Latin America 3.5 percent; Asia-Pacific 35.9 percent; Middle East and Africa 3.2 percent, according to the Interactive Advertising Bureau.

Obviously, mobile service providers in Europe, North America and parts of Asia are likely to reach a "critical mass" of revenue sooner than other regions.

But mobile advertising is a new and growing business, so most observers think the market eventually will grow to a size that is truly significant for mobile service providers.

Of current revenue, Europe represents 25.9 percent; North America 31.4 percent; Latin America 3.5 percent; Asia-Pacific 35.9 percent; Middle East and Africa 3.2 percent, according to the Interactive Advertising Bureau.

Obviously, mobile service providers in Europe, North America and parts of Asia are likely to reach a "critical mass" of revenue sooner than other regions.

2011: Mobile ad spend in $million

| Display | Search | Messaging | Total | |

| Europe | 367 | 900 | 114 | 1,380 |

| North America | 572 | 811 | 295 | 1,677 |

| Latin America | 31 | 74 | 83 | 188 |

| Asia-Pacific | 491 | 1,384 | 41 | 1,916 |

| Middle East & Africa | 44 | 124 | 4 | 172 |

| Global | 1,504 | 3,292 | 536 | 5,333 |

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Will Apple Do After Every Sizable Mobile Service Provider Sells the iPhone?

Apple will face a common supplier issue, namely product saturation, at some point, after every significant (in terms of market share) mobile service provider, in each market, sells the iPhone. Except for T-Mobile, all of the largest four U.S. carriers already sell the iPhone, and regional or prepaid carriers also are starting to get the device.

So Apple will do what any supplier normally does, in such situations. Refresh products so that existing buyers want to buy again. Apple also will continue wooing customers who now buy other devices to buy its own.

As it did with the iPod family of products, Apple will flesh out devices in a range of price segments, to capture more of the addressable market. Apple also will try to get existing and potential buyers to spend for other products Apple makes, such as tablets.

So Apple will do what any supplier normally does, in such situations. Refresh products so that existing buyers want to buy again. Apple also will continue wooing customers who now buy other devices to buy its own.

As it did with the iPod family of products, Apple will flesh out devices in a range of price segments, to capture more of the addressable market. Apple also will try to get existing and potential buyers to spend for other products Apple makes, such as tablets.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...