George L. Fendler, owner of Central Coast Internet in Hollister, Calif., has a problem. He wants to illustrate the “cost differences between fixed wireless and fiber installations in a rural environment.”

The problem is that “I don't really know what the cost per mile is for a fiber installation,” says Fendler. Lots of people would say that’s a very good question.

How much does it really cost a local telco to build fiber to home plant in rural areas? The answer, of course, is “it depends.” But a 2011 study of rural telco costs for fiber to home build shows that cost is directly related to potential customer density, measured as “locations per plant mile.”

Broadly speaking, when a telco can pass five to 65 locations for every mile of outside plant, the cost per home cost per home ranges between $4,000 and $5,000 per location. When the number of locations drops below five passings per plant mile, costs escalate quickly, up to $19,000 a location.

Friday, November 9, 2012

How Much Does Rural Fiber Really Cost?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

How Much Substitution Will LTE Drive?

Long Term Evolution might be a "future" strategy in most markets. But it is starting to look as though LTE already has become a marketing platform in the U.S. market. Every major mobile operator already is deploying, or trying to figure out how to deploy LTE.

Beyond that, some have been waiting for evidence that fourth generation mobile networks are fast enough to displace some amount of fixed broadband access. Up to this point, the actual amount of such product substitution has been fairly limited, though consumers in Austria have been enthusiastic about relying only on mobile for broadband access.

In Austria, 19 percent of households say they use only mobile broadband, and have no fixed broadband access. In Italy, about 14 percent say they have "cut the cord."

In the United Kingdom, about five percent say they now use only mobile broadband, while six percent report using only mobile broadband in the U.S. market. But those figures probably will jump as fourth generation LTE networks reach ubiquity in some markets.

The reason is that LTE should should in some cases offer users about an order of magnitude faster access than 3G.

And that will entice at least some users to evaluate LTE as a reasonable substitute for fixed broadband, especially lighter users who do not watch lots of streaming video, that do not share a single fixed connection for more than one or two light users, and who might conclude that the cost of a single mobile subscription with LTE offers a reasonable savings compared to buying both mobile service and a fixed network connection.

Verizon Wireless, for example, now plans to complete its LTE rollout by the middle of 2013, two quarters ahead of its previous goal to blanket its 3G footprint with LTE by the end of 2013.

AT&T now appears to be accelerating its own LTE build as well. AT&T and Verizon both have indicated they believe LTE can be a viable "next generation" broadband access network for many users in rural areas, for example.

In that sense, both AT&T and Verizon will themselves try to drive LTE cannibalization of fixed broadband access. So watch for new signs LTE is driving more substitution for fixed broadband service.

Beyond that, some have been waiting for evidence that fourth generation mobile networks are fast enough to displace some amount of fixed broadband access. Up to this point, the actual amount of such product substitution has been fairly limited, though consumers in Austria have been enthusiastic about relying only on mobile for broadband access.

In Austria, 19 percent of households say they use only mobile broadband, and have no fixed broadband access. In Italy, about 14 percent say they have "cut the cord."

In the United Kingdom, about five percent say they now use only mobile broadband, while six percent report using only mobile broadband in the U.S. market. But those figures probably will jump as fourth generation LTE networks reach ubiquity in some markets.

The reason is that LTE should should in some cases offer users about an order of magnitude faster access than 3G.

And that will entice at least some users to evaluate LTE as a reasonable substitute for fixed broadband, especially lighter users who do not watch lots of streaming video, that do not share a single fixed connection for more than one or two light users, and who might conclude that the cost of a single mobile subscription with LTE offers a reasonable savings compared to buying both mobile service and a fixed network connection.

Verizon Wireless, for example, now plans to complete its LTE rollout by the middle of 2013, two quarters ahead of its previous goal to blanket its 3G footprint with LTE by the end of 2013.

AT&T now appears to be accelerating its own LTE build as well. AT&T and Verizon both have indicated they believe LTE can be a viable "next generation" broadband access network for many users in rural areas, for example.

In that sense, both AT&T and Verizon will themselves try to drive LTE cannibalization of fixed broadband access. So watch for new signs LTE is driving more substitution for fixed broadband service.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Revenue Still Start Declining In Central, Eastern Europe in 2015

Mobile service providers in Central and Eastern Europe will hit a peak sometime about 2015, and then start declining, according to analysts at Analysys Mason.

Between 2007 and 2011, operators in Central and Eastern Europe had seen revenue growth of about 4.7 percent on a compound annual basis.

But Analysys Mason now projects that growth has slowed to about a one percent compound annual growth rate. Starting in 2015, revenue will slow at about a negative 0.6 percent CAGR.

Mobile service revenue at constant (2011) exchange rate [Source: Analysys Mason, 2012]

![Figure 1: Mobile service revenue at constant (2011) exchange rate, and index of mobile service revenue by region and Central and Eastern European sub-group, 2009–2017 [Source: Analysys Mason, 2012]](https://lh3.googleusercontent.com/blogger_img_proxy/AEn0k_vb2DvmThari7oa5sk1QH1W2kGAEBp_Zp0hywsrzrDJq8Z-ltSjgtfVWzxUDAEUF1TDRT0ywFwxmBdO5fjpbO6su0qBcmu8Osxm8w6v22YxBrj2UkmxAOHkvj2FIIFyoA=s0-d)

In Western Europe, revenue has been declining for some time.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Consumers Want Tablets for Christmas and Holidays

When consumers were asked whether they would rather receive a tablet computer or a laptop as a holiday gift this year, 59 percent indicated that they would rather receive a tablet, according to a PriceGrabber survey.

Some 71 percent of shoppers also indicated that they believe tablet computers will replace e-readers as gifts this year. Conducted from Oct. 24 to Nov. 1, 2012, the survey includes responses from 1,475 U.S. online shopping consumers.

If so, some current forecasts of tablet adoption, compared to sales of PCs, might have to be revised.

Some 71 percent of shoppers also indicated that they believe tablet computers will replace e-readers as gifts this year. Conducted from Oct. 24 to Nov. 1, 2012, the survey includes responses from 1,475 U.S. online shopping consumers.

If so, some current forecasts of tablet adoption, compared to sales of PCs, might have to be revised.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Austrian Telco Finds You Can't "Go it Alone" in Mobile Payments

It is extremely difficult for any single brand, especially a telecom service provider brand, to launch its own branded mobile payments system, competing, in other words, with MasterCard and Visa.

Isis, the venture owned by At&T, Verizon Wireless and T-Mobile USA, considered that approach but fairly quickly turned to a business model based on marketing, advertising and other e-commerce services other than processing transactions.

But Austria mobile service provider A1 gave it a try. It launched a "paybox NFC" payment system focused on mobile parking fare-collection service, as well as retail point of sale.

The telco, which is one of the few operators worldwide to operate its own bank, still found the task too daunting. A1, which is part of the Telekom Austria Group, had tried to get other Austrian telcos to take part in the paybox NFC payment scheme, but was apparently unsuccessful.

Nor was A1 able to entice a wide range of retailer to embrace the system, either. The closed-loop system also meant consumers would not be able to use the payment service outside of Austria.

The industry is in the early days of the shift to mobile commerce, including mobile payments and mobile wallets, so lots of trials will be held, and lots of approaches will fail. Some competitors still are going to try to take on the likes of Visa and MasterCard. You might say PayPal is among them.

Some will try and take on card issuers. Count Square and others among this group.

But many will simply look elsewhere for opportunities within the mobile commerce business.

Isis, the venture owned by At&T, Verizon Wireless and T-Mobile USA, considered that approach but fairly quickly turned to a business model based on marketing, advertising and other e-commerce services other than processing transactions.

But Austria mobile service provider A1 gave it a try. It launched a "paybox NFC" payment system focused on mobile parking fare-collection service, as well as retail point of sale.

The telco, which is one of the few operators worldwide to operate its own bank, still found the task too daunting. A1, which is part of the Telekom Austria Group, had tried to get other Austrian telcos to take part in the paybox NFC payment scheme, but was apparently unsuccessful.

Nor was A1 able to entice a wide range of retailer to embrace the system, either. The closed-loop system also meant consumers would not be able to use the payment service outside of Austria.

The industry is in the early days of the shift to mobile commerce, including mobile payments and mobile wallets, so lots of trials will be held, and lots of approaches will fail. Some competitors still are going to try to take on the likes of Visa and MasterCard. You might say PayPal is among them.

Some will try and take on card issuers. Count Square and others among this group.

But many will simply look elsewhere for opportunities within the mobile commerce business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, November 8, 2012

U.S. Video Subscription Business is Quite Mature

The U.S. video subscription business, like other network-based products such as voice and messaging, is a mature business, as seen in the number of net new customers the whole business is getting.

It isn't getting many new customers, with most of the change consisting of consumers switching service providers. In the third quarter of 2012, U.S. video service providers lost 127,000 customers, overall.

DirectTV gained 67,000 customers. Time Warner Cable lost 140,000; Comcast 117,000 customers. Cablevision shrunk by about 10,000 customers.

Charter shed 73,000 customers. So if those cable operators lost 359,000 customers, while DirecTV gained 67,000, there are 302,000 customers who went someplace other than DirecTV and Dish.

Most of them must have gone to AT&T and Verizon, the two largest U.S. telco providers.

It isn't getting many new customers, with most of the change consisting of consumers switching service providers. In the third quarter of 2012, U.S. video service providers lost 127,000 customers, overall.

DirectTV gained 67,000 customers. Time Warner Cable lost 140,000; Comcast 117,000 customers. Cablevision shrunk by about 10,000 customers.

Charter shed 73,000 customers. So if those cable operators lost 359,000 customers, while DirecTV gained 67,000, there are 302,000 customers who went someplace other than DirecTV and Dish.

Most of them must have gone to AT&T and Verizon, the two largest U.S. telco providers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Soon Will be Primary Internet Access, Everywhere

The use of mobile devices to access the Internet is becoming the medium of choice everywhere around the world, with 69 percent of all Internet users surveyed doing so daily, according to a study of consumers in Europe, Latin America and South Africa conducted by Accenture.

The use of mobile devices to access the Internet is becoming the medium of choice everywhere around the world, with 69 percent of all Internet users surveyed doing so daily, according to a study of consumers in Europe, Latin America and South Africa conducted by Accenture. In addition, consumers are using multiple devices to connect to the web, including smart phones (61 percent), netbooks (37 percent), and tablets (22 percent), the Accenture study suggests.

The study found that emerging economies such as Brazil, South Africa and Russia also have rapidly adopted mobile devices (more than 70 percent, on average) to access the Internet, Accenture says.

Given their affordability, smart phones are more likely than other devices to serve as access gateways to the Internet in these emerging markets. This trend is set to continue, with a higher percentage of respondents in emerging markets expressing their intention to buy a Web-enabled mobile phone in the near future (Brazil, 78 percent; Russia, 73 percent; Mexico, 61 percent; and South Africa, 57 percent) as compared with an average of 46 percent for all countries surveyed.

In developed European economies, mobile Internet is also on the rise. In Germany, adoption of mobile Internet access using smart phones has tripled since 2010 (from 17 to 51 percent), the study found.

In Switzerland, today 67 percent of respondents use Web-enabled mobile phones to go online, compared to 27 percent in 2010. In Austria, the percentage of mobile Internet users has doubled in two years (from 31 to 62 percent).

Information apps, such as train schedules, the weather, or news are the most popular downloaded apps, according to 72 percent of survey respondents, followed closely by entertainment apps (70 percent).

And there is confirmation of the importance of access network quality. Fully 85 percent of the respondents said that the “quality of the network” was the most important factor in selecting a smart phone or tablet. As you would expect, “communications” leads applications used frequently by mobile Internet users. Sending or receiving e-mails through an installed program is the most popular feature among all respondents (70 percent), followed by accessing online communities (62 percent) and instant messaging (61 percent).Respondents in the emerging markets of Mexico and South Africa are the biggest users of mobile email and instant messaging (more than 80 percent of respondents in both countries). Among all respondents, 27 percent use their mobile device for tweeting and blogging, and 46 percent use mobile devices to conduct banking transactions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

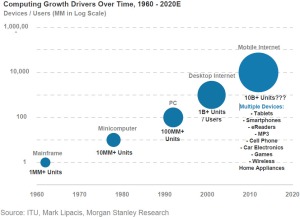

Post PC is Based on Mobile, Untethered, Cloud

You safely can assume we are entering a new era of computing when people do not even agree on a "name" for that era. We have passed through eras dominated by particular types of devices, such as mainframes, minicomputers and personal computers.

You safely can assume we are entering a new era of computing when people do not even agree on a "name" for that era. We have passed through eras dominated by particular types of devices, such as mainframes, minicomputers and personal computers.We now live in a world lead by use of smart phones, tablets and other devices such as MP3 players and game consoles. People seem to agree the coming or emerging era will feature cloud computing rather than locally-based, shrink-wrapped applications, untethered and nomadic or mobile devices.

People seem to agree that the "purpose" of computing appliances has changed. We use some devices mostly for "work," such as a desktop PC at the office. But most of the other devices, though sometimes also used for work, have a broader range of use cases.

Smart phones routinely are used for work and play. Tablets are used in the same way, but lean towards consumption of content, not its creation. MP3 and game consoles obviously are used mostly for entertainment and play.

Computers started out in glass rooms, moved to desktops, and now to pockets and purses. They are embedded in vehicles, industrial and commercial systems of all types.

But it remains difficult to separate out cloud computing from mobile, untethered and other forms of ubiquitous computing as the "defining" characteristic of the new era.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"Post-PC" Affects Device Usage, Design, Sales, Activities, Purpose and Places

PC shipments in Western Europe totaled 13.6 million units in the third quarter of 2012, a 15.4 percent decline compared with the same period in 2011, according to Gartner.

PC shipments in Western Europe totaled 13.6 million units in the third quarter of 2012, a 15.4 percent decline compared with the same period in 2011, according to Gartner."We've witnessed a decline across all PC segments this quarter in Western Europe," said Meike Escherich, principal analyst at Gartner. In the third quarter of 2012, mobile PC shipments declined 15.2 percent while desktop PC shipments decreased 15.7 percent. The professional and consumer PC markets declined 15.8 percent and 15 percent, respectively.

In the third quarter of 2012, the U.K. consumer PC market declined eight percent, while the professional PC market declined six percent. The mobile PC market declined three percent. The biggest problem was the desktop PC market, which fell 13 percent.

In the third quarter of 2012, the French consumer market decreased nearly eight percent due to low back-to-school sales. The French professional market declined 7.4 percent in the third quarter 2012.

PC shipments in Germany dropped 19 percent compared with the same period in 2011.

Germany mobile PC shipments declined 14 percent in the third quarter of 2012, while desktop volumes decreased 13 percent year over year. Consumer dropped 20 percent and professional PC demand declined 18 percent.

So what does it all mean? Computing is shifting from stationary to ubiquitous. Instead of "sitting at a desk," starting and finishing a task, users increasingly start on one device and then finish on other devices, at other times, Forrester Research says.

Ubiquitous computing also incorporates more "context," supplied by accelerometers, gyroscopes and geolocators.

"Post PC" computing also often is more casual. Compared to use of a PC at work, post PC consumption is interstitial: people use computing appliances for short periods of time, in between something else they are doing.

Use of computing appliances also is more often used on the couch and in bed, rather than at a desk or table. And physical interaction is physical (touch and swipe) rather than abstracted through the use of a keyboard and mouse.

The biggest evolution is from computing as "work" to computing as entertainment or play.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, November 7, 2012

Vodafone Spain Learns Important Lesson About Mobile Device Subsidies

Mobile service providers have good reasons for disliking subsidized smart phones, since the practice puts a real drag on operating results.

Mobile service providers have good reasons for disliking subsidized smart phones, since the practice puts a real drag on operating results. For AT&T, the financial impact of iPhone subsidies is clear. AT&T profit margins had grown for five straight years beginning in 2005, but reversed in 2010, apparently related directly to iPhone 4 demand and subsidies, BTIG argues.

BTIG estimates that the iPhone subsidies reduced AT&T margins by at least 10 percent in 2011, for example. To be sure, there also are churn reduction effects, as customers sign two-year contracts to earn the subsidies. But the subsidy costs outweigh the value of the churn benefits.

Vodafone Spain and Telefonica tested the theory that consumers would respond favorably to unsubsidized device prices by ending all device subsidies early in 2012. Both carriers might now agree that device subsidies are required.

Vodafone's Spanish division is bringing back subsidized smart phones, apparently on a "permanent" basis, after losing more than half a million customers in the second quarter of 2012 while competitors Orange and Yoigo gained market share.

A temporary restoration of subsidies was announced by Vodafone in August 2012.

Vodafone Spain and rival Telefonica used Spain as a testing ground for getting rid of the costly subsidies for new customers and ended the policy in April and March respectively.

But both companies lost out to rivals Orange and Yoigo, with Vodafone losing 639,000 customers in the second-quarter, while Telefonica lost 830,000 customers between April and August of 2012.

Meanwhile Orange gained 80,240 customers and Yoigo 58,069 in the second quarter and other operators gained 238,578 customers between them.

Vodafone's Spanish division is bringing back subsidized smart phones, apparently on a "permanent" basis, after losing more than half a million customers in the second quarter of 2012 while competitors Orange and Yoigo gained market share.

A temporary restoration of subsidies was announced by Vodafone in August 2012.

Vodafone Spain and rival Telefonica used Spain as a testing ground for getting rid of the costly subsidies for new customers and ended the policy in April and March respectively.

But both companies lost out to rivals Orange and Yoigo, with Vodafone losing 639,000 customers in the second-quarter, while Telefonica lost 830,000 customers between April and August of 2012.

Meanwhile Orange gained 80,240 customers and Yoigo 58,069 in the second quarter and other operators gained 238,578 customers between them.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Can LTE Replace Fixed Wireless?

AT&T says it will invest $14 billion over three years in new broadband facilities, including $8 billion for mobile and $6 billion for fixed network initiatives. The program would bring "fiber to the node" services to 75 percent of AT&T customer locations.

AT&T says it will invest $14 billion over three years in new broadband facilities, including $8 billion for mobile and $6 billion for fixed network initiatives. The program would bring "fiber to the node" services to 75 percent of AT&T customer locations. Perhaps significantly, AT&T says the investments will provide Long Term Evolution high speed access to 99 percent of AT&T's customer locations.

In other words, one might argue that nearly a quarter of AT&T customers might find that faster broadband access is made possible by LTE mobile networks.

Some now argue that LTE can replace T1 service. Others argue that cable modem service can cannibalize both T1 and DS3 or other high-capacity access services. That might be more true for business customers than consumers, given the higher price-per-bit of LTE access, compared to either telco DSL, fiber to the node, fiber to the home or cable modem high speed access.

In some ways, that is a simple continuation of global trends we have seen since the mid-1990s, when mobile began to represent a greater share of industry revenue.

In 2016, IDATE predicts that the number of LTE subscribers will exceed 900 million, compared to nearly 230 million for fixed ultrafast-broadband using fiber to the home, fiber to the building or high speed digital subscriber line (VDSL).

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

One Way of Looking at "Small Cells"

Even a casual conversation about the definition of a "small cell" will quickly lead to a series of necessary qualifications and a "fuzzy" answer. Pressed for a concise answer, many observers might point out that a "small cell" approach meaningfully could include every radio installation

smaller than a traditional cellular macrocell.

And that's quite a lot of terrain. It includes "carrier" cell sites of 2-kilometer radius, "pico" cells of perhaps 200 meters, but also customer-owned "femto" cells that cover indoor areas of perhaps 50 meters, and use the customer's own "backhaul" or "access," not a carrier-supplied link.

Those are some reasons why the "heterogeneous network" terminology now has become commonplace. Future mobile networks will use a variety of cell types, with different capital investment parameters and coverage areas.

Future networks also might make much more direct use of both carrier-supplied and customer-supplied backhaul. A carrier public Wi-Fi hotspot might use a carrier-supplied access connection, while, on an informal basis, most smart phone customers use their own fixed network connections, with their devices connected to in-home or in-building Wi-Fi, in place of any of the mobile cell site types.

Without making too much of the development, "heterogeneous" implies a mix of carrier and consumer-supplied radio and backhaul network resources; a range of management options and quality of service mechanisms.

One might also say that heterogenous networks and customer offloading to Wi-Fi also represent an unparalleled and new form of asset sharing. Whether by formal contract or simply informal mechanisms, customers are using a mix of carrier and "owned" access to support their "untethered" access requirements.

While some entrepreneurs continue to work at creating whole networks using end user supplied access and radio assets, the heterogeneous network does the same thing, essentially. In a broad sense, users and their devices are supported by a mix of carrier-owned and customer-owned networks, both "mobile" and "fixed," using mobile air interfaces and simple Wi-Fi.

The point is that "small cells" are more than a technology. They are part of a shift to more use of "shared" networks in a real sense.

smaller than a traditional cellular macrocell.

And that's quite a lot of terrain. It includes "carrier" cell sites of 2-kilometer radius, "pico" cells of perhaps 200 meters, but also customer-owned "femto" cells that cover indoor areas of perhaps 50 meters, and use the customer's own "backhaul" or "access," not a carrier-supplied link.

Those are some reasons why the "heterogeneous network" terminology now has become commonplace. Future mobile networks will use a variety of cell types, with different capital investment parameters and coverage areas.

Future networks also might make much more direct use of both carrier-supplied and customer-supplied backhaul. A carrier public Wi-Fi hotspot might use a carrier-supplied access connection, while, on an informal basis, most smart phone customers use their own fixed network connections, with their devices connected to in-home or in-building Wi-Fi, in place of any of the mobile cell site types.

Without making too much of the development, "heterogeneous" implies a mix of carrier and consumer-supplied radio and backhaul network resources; a range of management options and quality of service mechanisms.

One might also say that heterogenous networks and customer offloading to Wi-Fi also represent an unparalleled and new form of asset sharing. Whether by formal contract or simply informal mechanisms, customers are using a mix of carrier and "owned" access to support their "untethered" access requirements.

While some entrepreneurs continue to work at creating whole networks using end user supplied access and radio assets, the heterogeneous network does the same thing, essentially. In a broad sense, users and their devices are supported by a mix of carrier-owned and customer-owned networks, both "mobile" and "fixed," using mobile air interfaces and simple Wi-Fi.

The point is that "small cells" are more than a technology. They are part of a shift to more use of "shared" networks in a real sense.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Smart Phones Now Lead Public Wi-Fi Hotspot Activity

Smart phones now are the devices most often used at Wi-Fi hotspots, a study of Wi-Fi usage now finds. Respondents said 40 percent of Wi-Fi hotspot connections were used by smart phones, while 39 percent were notebook PCs. Tablets represent 17 percent of connections.

As you would guess, Wi-Fi is said to be playing an increasingly important role as a feature of a mobile or fixed network high speed Internet access service. That, in fact, is why cable operators and telcos have moved to offer public hotspot networks in their service territories, for example.

As you would guess, Wi-Fi is said to be playing an increasingly important role as a feature of a mobile or fixed network high speed Internet access service. That, in fact, is why cable operators and telcos have moved to offer public hotspot networks in their service territories, for example.

Smartphones overtake laptops as the most popular way to connect to Wi-Fi Hotspots

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Telefonica to Compete with Amazon for Cloud Computing Infrastructure

"Instant Servers" is a cloud-based infrastructure as a service offering that Telefonica hopes will allow it to offer a big branded alternative to other services such as Amazon's Elastic Compute Cloud that offer virtual server services.

That a big global telco thinks cloud computing is a business opportunity is not new. But the move might also illustrate one other aspect of competing with Amazon. A big company, with a "trusted" brand might be helpful, and sometimes essential, for any would-be competitor to firms such as Amazon.

Some familiar with customer opinion surveys might counter that people do not "like" their telco suppliers so well. That is true. But the issue is "trust," not "likability." The point is that potential customers might trust a telco to engineer and operate a reliable, available service, even if those suppliers are not particularly well liked.

Instant Servers promises 99.996 percent availability with a service guarantee that pays customers when those service level agreements are violated.

Telefonica also says its clouds can quadruple in capacity instantly, and without rebooting.

That a big global telco thinks cloud computing is a business opportunity is not new. But the move might also illustrate one other aspect of competing with Amazon. A big company, with a "trusted" brand might be helpful, and sometimes essential, for any would-be competitor to firms such as Amazon.

Some familiar with customer opinion surveys might counter that people do not "like" their telco suppliers so well. That is true. But the issue is "trust," not "likability." The point is that potential customers might trust a telco to engineer and operate a reliable, available service, even if those suppliers are not particularly well liked.

Instant Servers promises 99.996 percent availability with a service guarantee that pays customers when those service level agreements are violated.

Telefonica also says its clouds can quadruple in capacity instantly, and without rebooting.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, November 6, 2012

Will Mobile UC Mostly be a "Consumer Tools" Development

Mobile unified communications is in the early stages of mainstream adoption, so it is tough to predict how it will develop. But there is at least some thinking that consumer tools, not enterprise solutions will be a big factor.

In fact, some question the findings, arguing that survey findings might be overstating the use of "enterprise" unified communications systems and tools.

The native capabilities on virtually any smartphone can provide click-to-call, click-to-join a meeting, access to multiple communications modes (text, email, voice, or video), and a number of other features that either by themselves or through the use of a network-based service like Skype could be called "UC."

The longer term issue is whether consumer tools might wind up representing a huge part of business mobile UC adoption.

In fact, some question the findings, arguing that survey findings might be overstating the use of "enterprise" unified communications systems and tools.

The native capabilities on virtually any smartphone can provide click-to-call, click-to-join a meeting, access to multiple communications modes (text, email, voice, or video), and a number of other features that either by themselves or through the use of a network-based service like Skype could be called "UC."

The longer term issue is whether consumer tools might wind up representing a huge part of business mobile UC adoption.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...