That’s a dangerous combination for any industry. But it might also be fair to note that the actual benefits to consumers might be relatively modest, even if such new rules were to become part of the framework of mobile “consumer protection and choice,” as it is certain the matter would be sold.

Presumably, the value of unlocked devices will becomes a bigger actual value to consumers only when Long Term Evolution fourth generation networks are fully established in the U.S. market, for some simple reasons.

Unlike many other countries, subscribers and networks are at the moment split into GSM (AT&T and T-Mobile USA) and CDMA (Verizon Wireless and Sprint) air interface camps. An unlocked CDMA device cannot be used on the AT&T and T-Mobile USA neteworks, while a GSM unlocked device cannot be used on the Verizon or Sprint networks.

So while the idea “sounds nice,” the actual amount of consumer value is much less than most probably would think. That is not to say there is “no” value, only that the actual value might wind up being rather minor.

And some would say it doesn’t make sense to cause potential major damage to obtain a relatively small amount of benefit.

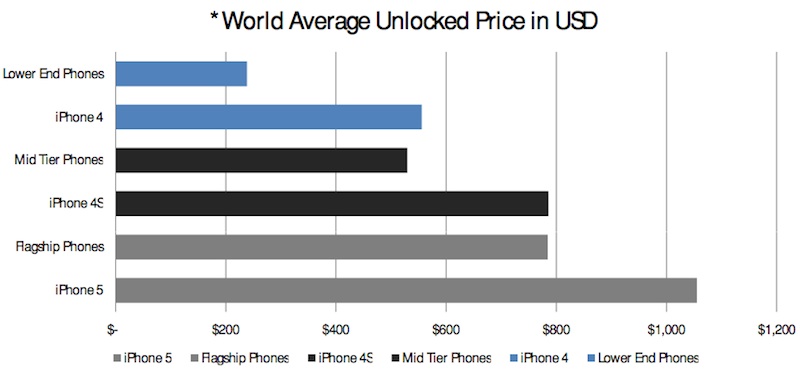

But the value of unlocking might be more subtle than many expect. If unlocked phones are sold at full retail prices, when consumers have the choice of a subsidized device, it seems likely to expect most consumers still will continue to opt for a subsidized device. That is especially true for the popular higher end devices.

Not many consumers are going to prefer shelling out full retail price for the latest Apple iPhone, even if they can, when the alternative is a lower device acquisition price, even at the cost of higher monthly recurring costs than might be possible if subsidies were not offered and available.

Beyond that, unlocking might help some consumers and provider segments, especially users on the “value” end of the market, and some firms that specialize in refurbishing and selling reconditioned devices.

That might be helpful for some businesses, and some U.S. consumers. ReCellular has been said to be one of the largest U.S.-based mobile phone refurbishers, and a mandatory “unlocked” phone regime might help such firms by boosting the value of used devices, at least marginally.

ReCellular resold or recycled 5.2 million mobile devices in 2010. ReCellular sells about 60 percent of its phones in the U.S. market and the rest mostly to dealers in Asia, Africa, Latin America and Eastern Europe.

But one might note that the market for used phones is relatively small. Global sales of used phones total a few hundred million units a year, estimates Andy Castonguay, an analyst at consulting firm Yankee Group. That compares with the 1.6 billion new phones sold world-wide last year.

That is only a proxy for the degree to which U.S. consumers might actually take their unlocked phones and switch to a different service provider.

For one thing, most consumers do not seem to keep any single device all that long. According to one U.S. study, the typical mobile device is used 18 months before being replaced. Whether that would be different in an unlocked device context is unclear.

The point is that people in the U.S. market mostly do not seem to want to keep their devices that long, whether they use one service provider or had a device that enabled easy switching. Keep in mind that the 18-month figure, like all “averages,” hides the differences between some users who will keep any device longer, and some who will replace devices even faster than 18 months.

That is not to say device unlocking would have zero advantages for end users and some businesses. It is harder to say what such rules might do for device innovation or the fortunes of mobile service providers.

Service provider revenues might be lower in an unlocked phone regime, since device sales count as “revenue,” and since unlocked device service plans would likely be lower than current plans that include the subsidy recovery.

And it is hard to see how competition between service providers would be less robust, in a full unlocked device regime, than under the current situation.

Service providers might sell fewer phones in the first place, as retail distribution shifts to third party retailers. Whether that helps or hurts service providers is tough to say, with precision.

On the other hand, service providers might benefit. The cost of phone subsidies might drop, so lower “revenue” might also be balanced by lower operating costs.

But service providers might have less ability to “control” customers or stabilize expected revenues that are “less lumpy” because the current two-year contracts reduce churn.

The point is that although the conventional wisdom is that mandatory phone unlocking will help consumers and harm service providers, it is not clear how big those changes might be. Every action has unintended consequences beyond the reactions service providers will undertake.

![[image]](http://si.wsj.net/public/resources/images/MK-CB244_DATA_NS_20130228184520.jpg)

{kind=link}