If you're the kind of person who has to keep up with Google and search engine optimization, this video is interesting.

It is an authorized Google release of an actual meeting where engineers considered a change in ranking algorithm.

Even relatively subtle changes get intense scrutiny by the ranking teams, Google seems to want to emphasize.

The specific change discussed in this video improves spelling suggestions for searches with more than 10 words and it impacts only 0.1 percent of traffic.

Every change has a dedicated search quality analyst assigned to study the impact. This analyst is not part of the engineering team building the change, but instead offers a separate opinion on whether the change is good for users.

he search team relies heavily on the results of experimental data to make decisions.

During the meeting, we rely on detailed analyst reports including the results of click evaluations and side-by-side experiments. These reports can sometimes be more than 25 pages long.

Launch reports include specific examples to illustrate broader trends in the data.

Rather than manually change one example, our engineers look for algorithmic ways to improve millions of queries.

earch algorithm improvements often rely on and impact many different systems, so engineers with expertise in different areas all need to come together to make the best decision for the user, balancing all the tradeoffs involved (relevance, spam, latency, cost, language impact).

Monday, March 12, 2012

Video of Google Algorithm Change Meeting

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple Could Be Huge in Mobile Commerce, But Will It?

Will Apple, though universally considered one of the most-important potential influences in mobie commerce, decide that the mobile commerce experience is big enough to matter, and is conducive to the creation of devices that are the best possible approach to that problem?

It's an important question. For starters, Apple makes products. To be interesting, an unmet need has to lead to the creation of a device that offers a dramatically better experience.

"Our goals are very simple, to design and make better products," says Sir Jonathan Ive, Apple’s SVP of Industrial Design. "If we can’t make something that is better, we won’t do it."

Apple's approach therefore requires identification of a mobile commerce problem that can be solved by a product. Also, Apple creates consumer products. That doesn't mean those products are not used by people in their business roles. It's just that Apple doesn't do "industrial" products.

It's an important question. For starters, Apple makes products. To be interesting, an unmet need has to lead to the creation of a device that offers a dramatically better experience.

"Our goals are very simple, to design and make better products," says Sir Jonathan Ive, Apple’s SVP of Industrial Design. "If we can’t make something that is better, we won’t do it."

Apple's approach therefore requires identification of a mobile commerce problem that can be solved by a product. Also, Apple creates consumer products. That doesn't mean those products are not used by people in their business roles. It's just that Apple doesn't do "industrial" products.

In many cases, there's a problem which is clear, such as Apple's belief that mobile phones and TVs offer experiences that are terribly sub-optimal.

In a startling number of cases, though, Apple tackles problem people are not aware of, or for which nobody has articulated a need. That's one reason Apple does not do focus groups or other market research to uncover unmet needs.

"It’s unfair to ask people" how well they would like a product they have never seen and do not know they need, he argues.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tablets are Changing Content Consumption Habits

Consumer and business content consumption patterns appear to be changing as tablet and e-reader ownership grow super fast. In fact, one might argue that tablets and e-readers are being adopted faster than any other consumer electronics or communications products of all time.

The share of adults in the United States who own a tablet of some sort nearly doubled from 10 percent to 19 percent between mid-December 2011 and early January 2012. That’s a doubling of mass market adoption in just 30 days, from a significant base.

The ownership of e-readers also surged from 10 percent to 19 percent over the same time period. Tablet ownership doubled in two months

That is an unprecedented growth rate for any consumer electronics device. Tablet ownership also had been on a strong adoption path earlier in 2011 as well, but doubling in 30 days from a base of 10 percent seems never to have occurred before.

And it appears that strong adoption is occurring both in the consumer and business markets.

Fully 51 percent of IT decision-makers surveyed by IDG say they “always” use their iPad at work (and a further 40 percent say they sometimes use it at work), IDG reports after conducting a survey on tablet use for work. Tablet business use

Though iPads seem to be used for a variety of purposes, content consumption seems to be a dominant business application, though significant percentages of business users also say the tablet displaces some amount of smart phone use as well.

Web browsing, reading and news consumption are the top three usage contexts identified by professionals worldwide.

Whether tablet ownership “revives” the print newspaper and magazine market remains to be seen. But it already is pretty clear that tablets and e-readers are changing the function of “reading.”

The survey suggests that tablet computing is transforming patterns of content consumption. iPad-owning IT and business professionals are rapidly migrating away from newspapers and printed books, toward digital alternatives.

Nearly three quarters of iPad owners say that owning an iPad has reduced the frequency with which they purchase newspapers and books. Whether that helps or harms print content providers remains to be seen.

What is very clear, though, is that tablets and e-readers are being adopted faster than any other personal device, period.Historically, 10 percent adoption of a consumer product has been an inflection point: it is the point in an adoption process that represents critical mass, after which adoption accelerates.There are some caveats. Not every innovation succeeds. This chart only shows you what happened with the most-popular consumer electronics services and products.

The point is that it can take quite a significant amount of time, between three and 10 years, for a successful and mass-adopted innovation to reach the crucial 10-percent-of-homes threshold, which seems to be the point at which any innovation really begins to accelerate, in terms of adoption.Tablets not only reached that level in a couple of years, they then exploded, doubling from 10 percent to nearly 20 percent, in literally 30 days. That is unheard of.

Also, it appears that Amazon might be winning its bet that if it sold Amazon Kindles almost at cost, it could grow content sales substantially.

RBC Capital analyst Ross Sandler polled 216 Kindle Fire owners and concluded that Kindle Fire tablets are making Amazon more money than was originally expected. Sandler originally had estimated that each Kindle Fire unit would generate about $136 in content purchases over the useful life of the device. Content purchases on Kindle Fire

But Sandler’s most-recent survey of 216 Kindle Fire owners suggests content revenue might be higher than that.

The survey found that roughly 80 percent of users already have purchased ebooks, with 58 percent of respondents buying more than three e-books within the first two months of owning the tablet.

Averaged out, that’s five e-books per quarter, which nets Amazon $15 per Fire owner per quarter, assuming an average selling price of $10 for ebooks. That further implies revenue from e-books of about $60 a year.

About 41 percent of Fire owners also say they have bought at least three apps. This will put another $9 per Fire owner per quarter into Amazon’s coffers, or $36 a year of net revenue (after splitting gross revenue with content owners).

That implies possible gross sales of about $30 a quarter worth of apps, assuming Amazon’s share of revenue is 30 percent.

Those figures suggest annual Kindle Fire revenue of about $96 a year. Over three years, that suggests $288 of revenue for Amazon, even if users do not buy any video or audio products, which seems unlikely.

The share of adults in the United States who own a tablet of some sort nearly doubled from 10 percent to 19 percent between mid-December 2011 and early January 2012. That’s a doubling of mass market adoption in just 30 days, from a significant base.

The ownership of e-readers also surged from 10 percent to 19 percent over the same time period. Tablet ownership doubled in two months

That is an unprecedented growth rate for any consumer electronics device. Tablet ownership also had been on a strong adoption path earlier in 2011 as well, but doubling in 30 days from a base of 10 percent seems never to have occurred before.

And it appears that strong adoption is occurring both in the consumer and business markets.

Fully 51 percent of IT decision-makers surveyed by IDG say they “always” use their iPad at work (and a further 40 percent say they sometimes use it at work), IDG reports after conducting a survey on tablet use for work. Tablet business use

Though iPads seem to be used for a variety of purposes, content consumption seems to be a dominant business application, though significant percentages of business users also say the tablet displaces some amount of smart phone use as well.

Web browsing, reading and news consumption are the top three usage contexts identified by professionals worldwide.

Whether tablet ownership “revives” the print newspaper and magazine market remains to be seen. But it already is pretty clear that tablets and e-readers are changing the function of “reading.”

The survey suggests that tablet computing is transforming patterns of content consumption. iPad-owning IT and business professionals are rapidly migrating away from newspapers and printed books, toward digital alternatives.

Nearly three quarters of iPad owners say that owning an iPad has reduced the frequency with which they purchase newspapers and books. Whether that helps or harms print content providers remains to be seen.

What is very clear, though, is that tablets and e-readers are being adopted faster than any other personal device, period.Historically, 10 percent adoption of a consumer product has been an inflection point: it is the point in an adoption process that represents critical mass, after which adoption accelerates.There are some caveats. Not every innovation succeeds. This chart only shows you what happened with the most-popular consumer electronics services and products.

The point is that it can take quite a significant amount of time, between three and 10 years, for a successful and mass-adopted innovation to reach the crucial 10-percent-of-homes threshold, which seems to be the point at which any innovation really begins to accelerate, in terms of adoption.Tablets not only reached that level in a couple of years, they then exploded, doubling from 10 percent to nearly 20 percent, in literally 30 days. That is unheard of.

Also, it appears that Amazon might be winning its bet that if it sold Amazon Kindles almost at cost, it could grow content sales substantially.

RBC Capital analyst Ross Sandler polled 216 Kindle Fire owners and concluded that Kindle Fire tablets are making Amazon more money than was originally expected. Sandler originally had estimated that each Kindle Fire unit would generate about $136 in content purchases over the useful life of the device. Content purchases on Kindle Fire

But Sandler’s most-recent survey of 216 Kindle Fire owners suggests content revenue might be higher than that.

The survey found that roughly 80 percent of users already have purchased ebooks, with 58 percent of respondents buying more than three e-books within the first two months of owning the tablet.

Averaged out, that’s five e-books per quarter, which nets Amazon $15 per Fire owner per quarter, assuming an average selling price of $10 for ebooks. That further implies revenue from e-books of about $60 a year.

About 41 percent of Fire owners also say they have bought at least three apps. This will put another $9 per Fire owner per quarter into Amazon’s coffers, or $36 a year of net revenue (after splitting gross revenue with content owners).

That implies possible gross sales of about $30 a quarter worth of apps, assuming Amazon’s share of revenue is 30 percent.

Those figures suggest annual Kindle Fire revenue of about $96 a year. Over three years, that suggests $288 of revenue for Amazon, even if users do not buy any video or audio products, which seems unlikely.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sunday, March 11, 2012

Citi Launches Kindle Fire App for Mobile Banking

Citi is expanding its mobile repertoire with the launch of a Kindle Fire application that lets consumers track, analyze and plan their finances.

Citi is expanding its mobile repertoire with the launch of a Kindle Fire application that lets consumers track, analyze and plan their finances.The Citibank Kindle Fire app lets consumers access their finances no matter where they are.

In addition to the new app, Citi has also rolled out two additional mobile banking capabilities, mobile check deposit and Citibank Popmoney.

Through the Mobile Check Deposit feature, consumers can take photos of the front and back of their check and submit it for verification.

The Popmoney feature lets users send money through the Citi Mobile app to people they have set up as payees on Citibank Online.

There's a broader question bankers themselves, and others in the mobile commerce space, always ask. Namely, what is the return on such investment? The key problem for a bank is that it is not clear whether a bank actually grows its revenue when it invests in the mobile channel.

It might be a key cost of doing business. There should be some benefits in terms of customer satisfaction, stickiness and churn retention. There could be some operating cost implications. But it remains unclear how big those effects might be, in terms of revenue.

The problem is akin to the similar issue telecom service providers face when offering voice over Internet Protocol services that displace older voice services. The problem is that incumbents typically have found they cannibalize the older services with the new, investing heavily in return for less revenue.

Bankers might find something similar is the problem with mobile commerce, banking and payments. Citi Kindle Fire App

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Ails Video on Demand?

According to a new report released by The Diffusion Group (TDG), video-on-demand services provided by PayTV operators should be, but are not, generating significantly higher viewing and advertising revenue. Total VOD use is small, representing only one percent of all U.S. TV viewing.

By some measures, VOD is doing better. Magna Global has estimated that U.S. homes with VOD, a "category that includes both traditional multichannel VOD offerings and over the top services," will hit 70.1 million homes, about 57 percent of all TV homes at the end of 2016.

But note the conflation of traditional VOD and over the top services and apps. Some of us would not classify over-the-stop streaming as VOD, just as time-shifted viewing on a digital video recorder is not VOD, and Netflix streaming is not VOD.

Still, even availability is not the same thing as "usage." Hundreds of TV channels are available on cable, satellite and telco subscription video services. That doesn't mean those channels are viewed by most people. Much as fixed line voice service is available to most homes, but isn't necessarily purchased by all those homes, so too for-fee or ad-supported VOD is available relatively widely, but isn't used much.

By some measures, VOD is doing better. Magna Global has estimated that U.S. homes with VOD, a "category that includes both traditional multichannel VOD offerings and over the top services," will hit 70.1 million homes, about 57 percent of all TV homes at the end of 2016.

But note the conflation of traditional VOD and over the top services and apps. Some of us would not classify over-the-stop streaming as VOD, just as time-shifted viewing on a digital video recorder is not VOD, and Netflix streaming is not VOD.

Still, even availability is not the same thing as "usage." Hundreds of TV channels are available on cable, satellite and telco subscription video services. That doesn't mean those channels are viewed by most people. Much as fixed line voice service is available to most homes, but isn't necessarily purchased by all those homes, so too for-fee or ad-supported VOD is available relatively widely, but isn't used much.

TDG attributes that failure as a reflection of VOD's inadequate advertising support and awkward program guides that limit availability and viewing of ad-supported video-on-demand content. VOD hampered

Some of us might argue that "inattention" not withstanding VOD never has gotten much traction in the U.S. market and that the problem is lack of interest and demand on the part of consumers.

Service provider lack of attention to ad-supported VOD is the problem, TDG argues.

According to Bill Niemeyer, TDG senior analyst, "operators have failed to take advantage of VOD to build subscriber satisfaction, generate ad revenues, and head off competition from over-the-top (OTT) providers like Netflix."

Niemeyer estimates in the fourth quarter 2011, Netflix U.S. subscribers watched 80 percent more streaming video hours than were viewed in the same period on all U.S. PayTV VOD.

Some of us might argue that marginal failures to market and support VOD could be an issue. But there is a reason service providers do not market VOD so intensively. VOD simply does not contribute significant revenue for a service provider.

VOD in recent years has contributed about $2 billion a year worth of revenue for U.S. video entertainment providers. U.S. cable TV companies alone booked about $98 billion in 2011 revenue. That doesn't include the sizable revenue earned by satellite and telco providers as well.

The point is that VOD, as a service, has been a modest success, though it has had three decades to make its case.

Some of us might argue that "inattention" not withstanding VOD never has gotten much traction in the U.S. market and that the problem is lack of interest and demand on the part of consumers.

Service provider lack of attention to ad-supported VOD is the problem, TDG argues.

According to Bill Niemeyer, TDG senior analyst, "operators have failed to take advantage of VOD to build subscriber satisfaction, generate ad revenues, and head off competition from over-the-top (OTT) providers like Netflix."

Niemeyer estimates in the fourth quarter 2011, Netflix U.S. subscribers watched 80 percent more streaming video hours than were viewed in the same period on all U.S. PayTV VOD.

Some of us might argue that marginal failures to market and support VOD could be an issue. But there is a reason service providers do not market VOD so intensively. VOD simply does not contribute significant revenue for a service provider.

VOD in recent years has contributed about $2 billion a year worth of revenue for U.S. video entertainment providers. U.S. cable TV companies alone booked about $98 billion in 2011 revenue. That doesn't include the sizable revenue earned by satellite and telco providers as well.

The point is that VOD, as a service, has been a modest success, though it has had three decades to make its case.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amazon Bets on Buying, Reselling iPads to Boost its Own Business

Amazon is among the best marketers in the mobile commerce space, perhaps the boldest. While most other contestants consider near term return on investment, Amazon frequently goes for the long term opportunity, even at short term risk.

Amazon Trade-In, for example, lowest offers a trade-in program iPad 2s, giving users $236 or more fore units in “good” condition. Apple is selling new iPad 2s for $399.

While other trade-in sites will give sellers cash, Amazon gives customers store credit. In essence, Amazon is simply buying a bit of business. For starters, the reconditioned iPads are in turn sold on Amazon for $360 or more.

By some estimates, Amazon might actually lose $14 after buying, reconditioning and reselling any single iPad. But that isn’t the point. It never is, with Amazon.

Users then buy stuff from Amazon, which begins to earn back that $14 of loss.

There’s a chance, though, that Amazon could get even luckier on you. If you use your trade-in money to buy a device or service that keeps you locked to the company for a long time, Amazon might end up making more money on you over time, especially if the user buys a Kindle, or joins Amazon Prime.

One analysis suggests that after joining Prime, the amount of money that a customer spends at Amazon jumps from $400 per year to $900 per year.

Amazon Trade-In, for example, lowest offers a trade-in program iPad 2s, giving users $236 or more fore units in “good” condition. Apple is selling new iPad 2s for $399.

While other trade-in sites will give sellers cash, Amazon gives customers store credit. In essence, Amazon is simply buying a bit of business. For starters, the reconditioned iPads are in turn sold on Amazon for $360 or more.

By some estimates, Amazon might actually lose $14 after buying, reconditioning and reselling any single iPad. But that isn’t the point. It never is, with Amazon.

Users then buy stuff from Amazon, which begins to earn back that $14 of loss.

There’s a chance, though, that Amazon could get even luckier on you. If you use your trade-in money to buy a device or service that keeps you locked to the company for a long time, Amazon might end up making more money on you over time, especially if the user buys a Kindle, or joins Amazon Prime.

One analysis suggests that after joining Prime, the amount of money that a customer spends at Amazon jumps from $400 per year to $900 per year.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Proof of App Store Value for Devices

It is by now conventional wisdom that the success of a device ecosystem hinges on its application and content richness.

It is by now conventional wisdom that the success of a device ecosystem hinges on its application and content richness. The Apple iPod needs iTunes, Android requires Google Play. A study by GfK supports the notion.

Consumers are less likely to switch device brands the more applications and services they use on the device, GfK finds.

GfK’s report on user experience and loyalty in the digital ecosystem, was undertaken across nine countries including Brazil, China, France, Germany, Japan, Italy, Spain, United Kingdom and the United States.

Some 19 percent of consumers that own both an iPad and an iPhone believe that changing types of smart phone is more difficult than changing bank accounts or gas or electricity providers, in fact.

The study shows that their loyalty to their smart phone brand increases with the number of apps and services used. The research reveals that the tipping point for loyalty is when a consumer uses seven or more services on their device. At that point, consumers see themselves as locked in to a device ecosystem.

Consumers in the United States are the most likely to use seven or more services (61 percent), followed closely by China (56 percent) and Brazil (53 percent). In comparison to this, European countries use fewer services on their smartphone; France and Italy (46 percent), Germany (45 percent), Spain (43 percent) and the UK (42 percent).

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

How Do You Sell an Intangible Product?

For most of its 150-year history, the telecom business has had to sell an intangible product, with few proxies for value and few ways to create a "hot" emotional connection with customers. As value as "dial tone" might be, what consumer is emotionally involved with the product?

That changed with the introduction of the Apple iPhone. For the first time in its history, telcos have a physical embodiment of service with which consumers do have emotional connection. The problem, some executives will note, is that the bond is with the third party device, not the service provider or service. That's correct.

Still, for those who have been waiting for some way to create high emotional engagement with an intangible communications service, iPhone is the closest proxy in 150 years. And that matters.

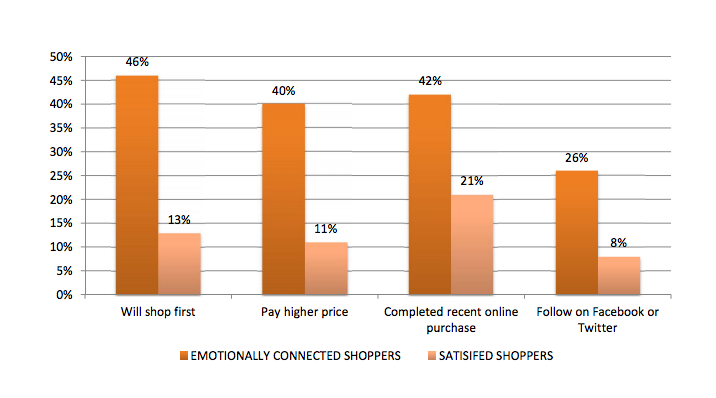

Recent data from Motista illustrated the top emotional drivers behind retail purchases in the fourth quarter of 2011 were more motivated by “fun” and “comfort in life,” reflecting an emotional need they want from their retailers.

The data also compared satisfied consumers to emotionally connected consumers, and forty-six percent of emotionally connected shoppers indicated they always shop a particular retailer first compared to only 13 percent of “satisfied” shoppers. In other words, emotionally connected shoppers are four times more likely to shop a particular retailer first.

Emotional involvement makes a huge difference.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, March 10, 2012

Cloud Computing Gaining Traction in Both Enterprise and Small Business

Both enterprise and smaller businesses are adopting cloud computing apps and services at a higher levels, a couple of new studies suggest. The number of enterprises turning to cloud computing to revamp existing business models will more than double in the next three years, a new study by IBM predicts.

Also, nearly half of the respondents in a recent CIO Economic Impact survey indicated they evaluate cloud options first, over traditional IT approaches, before making any new IT investments.

The survey revealed that while a higher percentage of large organizations (those with revenues

more than $20 billion) are experimenting with cloud, 67 percent of companies with revenues less than $1 billion and 76 percent of those with revenues between $1billiion and 20 billion have adopted cloud at some level.

Those sorts of developments are why some believe the global cloud computing market will

grow 22 percent annually to $241 billion by 2020. That’s a market big enough to be interesting to lots of firms.

The Economist Intelligence Unit surveyed more than 500 business and technology executives worldwide as part of the study.

While 16 percent of the executives surveyed indicate they are already using cloud capabilities, by 2015 35 percent intend to use it to transform their business models. And operating efficiencies will not be driving the move.

While a little more than half of the respondents indicated "improving organizational efficiency" as a top business challenge today, only 31 percent anticipate it will be a top challenge in three years.

Instead the study indicates that their focus is shifting to growth and competitive initiatives. Some 62 percent of survey respondents said increased collaboration with external partners is a key objective for adopting cloud, while

57 percent cited competitive cost advantages through vertical integration as a major motivation.

About 56 percent said the ability to create new delivery channels and markets was an important objective for their cloud initiatives.

Also, small and medium businesses that currently use cloud applications plan to add an average of three new cloud business applications in 2012, according to a survey sponsored by Dell Cloud Business Applications and conducted by Techaisle.

About 70 percent of cloud services as “software as a service” apps and usage of those apps has doubled over the last two years, from an average of two apps to four, with an expectation that a typical user will be running seven apps by the end of 2012.

Customer relationship management has the highest penetration of any cloud application at up to 55 percent, an increase of up to 34 percent from 2010. That is up from 34 percent usage in 2010.

But several other applications were not far behind. Some 54 percent of respondents use cloud-based project management apps. About 49 percent reported using business analytics on a cloud basis.

Some 48 percent use a sales automation tool, the same percentage reporting use of a cloud-based payroll app. Some 43 percent

Dell notes that cloud delivery has lowered costs enough that many smaller organizations now can afford to use CRM apps. Of respondents using CRM, about 25 percent report they are likely to add business intelligence and marketing automation apps within the next 12 months.

Perhaps 50 percent of respondents noted significant challenges in keeping track of different service level agreements, while up to 48 percent complained that explaining their business to each vendor was tedious and time consuming.

As many as 74 percent of respondents use in-house information technology staff to integrate new cloud applications with on-premise technology.

On average, respondents believe they have experienced up to a 38 percent improvement in operational efficiency due to reduced manual processes and up to a 39 percent improvement in employee productivity due to automation of tasks and information.

The survey was conducted with 400 SMBs in the United States that are using at least one cloud-based business application. The survey was conducted online in December 2011 and included both IT and business decision makers.

Also, nearly half of the respondents in a recent CIO Economic Impact survey indicated they evaluate cloud options first, over traditional IT approaches, before making any new IT investments.

The survey revealed that while a higher percentage of large organizations (those with revenues

more than $20 billion) are experimenting with cloud, 67 percent of companies with revenues less than $1 billion and 76 percent of those with revenues between $1billiion and 20 billion have adopted cloud at some level.

Those sorts of developments are why some believe the global cloud computing market will

grow 22 percent annually to $241 billion by 2020. That’s a market big enough to be interesting to lots of firms.

The Economist Intelligence Unit surveyed more than 500 business and technology executives worldwide as part of the study.

While 16 percent of the executives surveyed indicate they are already using cloud capabilities, by 2015 35 percent intend to use it to transform their business models. And operating efficiencies will not be driving the move.

While a little more than half of the respondents indicated "improving organizational efficiency" as a top business challenge today, only 31 percent anticipate it will be a top challenge in three years.

Instead the study indicates that their focus is shifting to growth and competitive initiatives. Some 62 percent of survey respondents said increased collaboration with external partners is a key objective for adopting cloud, while

57 percent cited competitive cost advantages through vertical integration as a major motivation.

About 56 percent said the ability to create new delivery channels and markets was an important objective for their cloud initiatives.

Also, small and medium businesses that currently use cloud applications plan to add an average of three new cloud business applications in 2012, according to a survey sponsored by Dell Cloud Business Applications and conducted by Techaisle.

About 70 percent of cloud services as “software as a service” apps and usage of those apps has doubled over the last two years, from an average of two apps to four, with an expectation that a typical user will be running seven apps by the end of 2012.

Customer relationship management has the highest penetration of any cloud application at up to 55 percent, an increase of up to 34 percent from 2010. That is up from 34 percent usage in 2010.

But several other applications were not far behind. Some 54 percent of respondents use cloud-based project management apps. About 49 percent reported using business analytics on a cloud basis.

Some 48 percent use a sales automation tool, the same percentage reporting use of a cloud-based payroll app. Some 43 percent

Dell notes that cloud delivery has lowered costs enough that many smaller organizations now can afford to use CRM apps. Of respondents using CRM, about 25 percent report they are likely to add business intelligence and marketing automation apps within the next 12 months.

Perhaps 50 percent of respondents noted significant challenges in keeping track of different service level agreements, while up to 48 percent complained that explaining their business to each vendor was tedious and time consuming.

As many as 74 percent of respondents use in-house information technology staff to integrate new cloud applications with on-premise technology.

On average, respondents believe they have experienced up to a 38 percent improvement in operational efficiency due to reduced manual processes and up to a 39 percent improvement in employee productivity due to automation of tasks and information.

The survey was conducted with 400 SMBs in the United States that are using at least one cloud-based business application. The survey was conducted online in December 2011 and included both IT and business decision makers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Is There A Return for Bankers on Mobile Commerce Investments?

Technology and business disruptions are harsh. Sometimes, there simply is no way a set of industry leaders in one era can survive in the era that comes next. You can see this, as a historical matter, in the canal industry, the railroad industry, the steel industry, the auto industry, mainframe computing, mini-computer and now even the PC business.

The point is that there was virtually no amount of investment or creativity that would have allowed industry leaders in one era to prosper in the succeeding era. The only conceivable survival strategy would have been to abandon the original business, entirely or substantially.

Telecom service providers face precisely that problem with voice services, which historically have provided 70 percent of all revenue. The existential problem is that it might not be possible, under any circumstances, to sustain or revive a business model under intense pressure from a variety of forces.

Some might notice that international long distance calling, among the first segments of the business to feel the gale winds, saw pricing drop from $60 a unit to 10 cents a unit over a few decades. Over time, a wider range of voice products have seen that pressure start to erode revenue and profit margin, ranging from domestic calling to local access to enhanced features.

"Forget about return on investment" is the advice some would give to banks struggling to find a return on mobile payments or mobile commerce investments. At one level, the advice makes sense. Pilot programs, even though it might be hard to figure out how many different types of pilots should be conducted, make sense as a defensive move.

At another level, "forget about ROI" is the key question. Sometimes such questions are existential.

Telcos face other existential problems as well. In many cases, there is no solid business case for building a new fiber-to-home access network, as the incremental revenue simply is insufficient to justify the investment.

The voice function doesn't benefit at all. New broadband access services might bring in more money, as will video entertainment services. But the issue has been that the new revenue really doesn't justify the investment. Some might even question whether the return even meets the cost of capital.

Banks might face the same issue with mobile banking, commerce and payment. It might turn out that the struggles over "return" on investment will never be answered. In other words, there might simply be no real way to earn a return from mobile projects, as such investments only represent incremental channels.

That means more cost, and identical revenue. There is, in other words, no business case to be made. Still, some have tried to quantify the benefits.

Forrester analysts Brad Strothkamp, Alexander Hesse, and Peter Wannemacher have pegged ROI for mobile banking of 15.7 percent, for a hypothetical bank with 500,000 customers.

But note that most of the return comes from the estimated value of reduced costs, retained customers and cross-selling of new products, though that admittedly is minimal.

The Forrester consumer survey relies heavily on reduced service costs to drive the return. When U.S. users of mobile banking were asked how mobile has changed their use of other banking channels, 43 percent said they had made fewer phone calls to their bank’s call center since adopting mobile banking and more than one-third (35%) said they visited branches less often than they did before adopting mobile banking.

The bank with 500,000 retail customers in Forrester’s model could achieve a savings of more than $150,000 by the reduced traffic in branches and call centers. The return, one might argue, would have been better if the hypothetical bank could have closed call centers and branches.

The alternative was simply to harvest the legacy business as long as possible, before cannibalizing the remainder of the business. That is what AT&T essentially did with its long distance business.

There might, in the final analysis, be no way banks actually can win the mobile commerce and mobile banking game. The costs of implementing might never produce any significant new revenue. There could be some cost savings, but supporting more channels will be necessary. It isn't possible to replace any existing channels.

In that sense there also is an analogy to the telecom business adopting voice over Internet Protocol services that cannibalize legacy voice. The only contenders that actually win are the attackers.

They have zero market share and revenue to begin with. If they can create lower-cost business models, the incremental revenue, even when at vastly-lower gross amounts, still is a net win.

Mobile commerce and banking might be that sort of issue for banks. Perhaps the best case scenario is that banks invest capital only to protect what they already have. In the worse case, they invest to no avail. Attackers begin to take market share despite everything banks do to protect themselves.

When business eras change, the impact on industry leaders can be catastrophic. One simply wonders if that is about to happen in the banking business, driven by new payments methods.

Sometimes, there is almost nothing former leaders really can do to save their businesses.

The point is that there was virtually no amount of investment or creativity that would have allowed industry leaders in one era to prosper in the succeeding era. The only conceivable survival strategy would have been to abandon the original business, entirely or substantially.

Telecom service providers face precisely that problem with voice services, which historically have provided 70 percent of all revenue. The existential problem is that it might not be possible, under any circumstances, to sustain or revive a business model under intense pressure from a variety of forces.

Some might notice that international long distance calling, among the first segments of the business to feel the gale winds, saw pricing drop from $60 a unit to 10 cents a unit over a few decades. Over time, a wider range of voice products have seen that pressure start to erode revenue and profit margin, ranging from domestic calling to local access to enhanced features.

"Forget about return on investment" is the advice some would give to banks struggling to find a return on mobile payments or mobile commerce investments. At one level, the advice makes sense. Pilot programs, even though it might be hard to figure out how many different types of pilots should be conducted, make sense as a defensive move.

At another level, "forget about ROI" is the key question. Sometimes such questions are existential.

Telcos face other existential problems as well. In many cases, there is no solid business case for building a new fiber-to-home access network, as the incremental revenue simply is insufficient to justify the investment.

The voice function doesn't benefit at all. New broadband access services might bring in more money, as will video entertainment services. But the issue has been that the new revenue really doesn't justify the investment. Some might even question whether the return even meets the cost of capital.

Banks might face the same issue with mobile banking, commerce and payment. It might turn out that the struggles over "return" on investment will never be answered. In other words, there might simply be no real way to earn a return from mobile projects, as such investments only represent incremental channels.

That means more cost, and identical revenue. There is, in other words, no business case to be made. Still, some have tried to quantify the benefits.

Forrester analysts Brad Strothkamp, Alexander Hesse, and Peter Wannemacher have pegged ROI for mobile banking of 15.7 percent, for a hypothetical bank with 500,000 customers.

But note that most of the return comes from the estimated value of reduced costs, retained customers and cross-selling of new products, though that admittedly is minimal.

The Forrester consumer survey relies heavily on reduced service costs to drive the return. When U.S. users of mobile banking were asked how mobile has changed their use of other banking channels, 43 percent said they had made fewer phone calls to their bank’s call center since adopting mobile banking and more than one-third (35%) said they visited branches less often than they did before adopting mobile banking.

The bank with 500,000 retail customers in Forrester’s model could achieve a savings of more than $150,000 by the reduced traffic in branches and call centers. The return, one might argue, would have been better if the hypothetical bank could have closed call centers and branches.

Some 30 percent of U.S. mobile banking users say mobile banking has made them more likely to stay with the bank from which they receive the service. Forrester analysts project that a bank with 500,000 retail customers could save more than $450,000 in annual revenues from reduced attrition, for this reason.

The case for mobile banking increasing cross-sales for a bank is weaker and represents only three percent of the benefits. Forrester’s survey found that 18 percent of mobile banking users say they are more likely to buy more products from the banks they use for mobile banking.

This could bring a bank additional revenue of $20,000 from cross-selling products like credit cards to mobile banking users, the analysts estimate.

Of course, the argument about operating cost savings was made by Verizon when it sought to justify its FiOS fiber to the home network as well. Verizon could not make the business case work based strictly on revenue enhancement, so sought to add in operating cost savings. Many would argue Verizon simply hasn't gained as much as it thought on the opex front.

That, many argue, is why Verizon has halted further FiOS builds and is selling off assets where the business case is even worse than in the big metro areas.

Telecom executives already have had to confront such choices, is the point. Telcos could have fully embraced new technologies that had the practical effect of destroying gross revenue and profit margin in their single most important business. In the international long distance example, providers could have willingly and immediately slashed their own prices, literally destroying most of the existing business. This could bring a bank additional revenue of $20,000 from cross-selling products like credit cards to mobile banking users, the analysts estimate.

Of course, the argument about operating cost savings was made by Verizon when it sought to justify its FiOS fiber to the home network as well. Verizon could not make the business case work based strictly on revenue enhancement, so sought to add in operating cost savings. Many would argue Verizon simply hasn't gained as much as it thought on the opex front.

That, many argue, is why Verizon has halted further FiOS builds and is selling off assets where the business case is even worse than in the big metro areas.

The alternative was simply to harvest the legacy business as long as possible, before cannibalizing the remainder of the business. That is what AT&T essentially did with its long distance business.

There might, in the final analysis, be no way banks actually can win the mobile commerce and mobile banking game. The costs of implementing might never produce any significant new revenue. There could be some cost savings, but supporting more channels will be necessary. It isn't possible to replace any existing channels.

In that sense there also is an analogy to the telecom business adopting voice over Internet Protocol services that cannibalize legacy voice. The only contenders that actually win are the attackers.

They have zero market share and revenue to begin with. If they can create lower-cost business models, the incremental revenue, even when at vastly-lower gross amounts, still is a net win.

Mobile commerce and banking might be that sort of issue for banks. Perhaps the best case scenario is that banks invest capital only to protect what they already have. In the worse case, they invest to no avail. Attackers begin to take market share despite everything banks do to protect themselves.

When business eras change, the impact on industry leaders can be catastrophic. One simply wonders if that is about to happen in the banking business, driven by new payments methods.

Sometimes, there is almost nothing former leaders really can do to save their businesses.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

American Banker Audience Not Sure How Well Banks Will Fare in Mobile Payments

It's just a shapshot, but a recent non-scientific poll conducted by American Banker shows uneasiness on the part of American Banker readers about how well banks are positioned in the developing mobile payments and mobile commerce businesses.

Some 36 percent think others in the ecosystem are gaining the upper hand. Only 15 percent believe banks say "banks still are necessary."

Some 36 percent think others in the ecosystem are gaining the upper hand. Only 15 percent believe banks say "banks still are necessary."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

PayPal Could Threaten Visa, MasterCard

There's a reason PayPal now represents a potentially significant threat to Visa and MasterCard in the transaction clearing business. For starters, PayPal is the only big name contestant that, at least for the moment, has a business model that challenges firms such as Visa and MasterCard.

There's a reason PayPal now represents a potentially significant threat to Visa and MasterCard in the transaction clearing business. For starters, PayPal is the only big name contestant that, at least for the moment, has a business model that challenges firms such as Visa and MasterCard.Whatever else Google, Isis (AT&T, Verizon Wireless, T-Mobile USA), Apple and Amazon might wish to do, for the moment they are focusing on parts of the mobile commerce ecosystem that actually are complementary to the clearing networks.

But PayPal, in principle, can displace the clearing networks. PayPal almost certainly can operate at lower cost than Visa and MasterCard, and in a competitive business, the low-cost provider tends to win, long term.

Also, recent surveys suggest there is a level of trust in the PayPal brand, in terms of end user trust, that concedes nothing to Visa, American Express or MasterCard.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Shopping Shifts

Games, ring tones, songs and other content are prime examples. Over the last couple of years, though, the amount of physical goods purchased directly from a mobile has shifted.

More users are buying physical goods than ever before. Also, in terms of change, the biggest growth is physical goods and the biggest decline is purchasing of ring tones.

There are many potential repercussions. The volume growth could suggest the emergence of a "mobile commerce" behavior and therefore a business opportunity that is distinct both from online commerce and "brick and mortar store" retailing.

Also, since most digital goods are small transactions, while physical goods will range widely in price, the methods of payment are likely to change. In the past, it probably has made most sense, for most people, to use simple billing direct to a mobile service bill for such small purchases.

That won't make sense for the wider range of physical goods people now are buying. But the big trend is the emergence of a distinct mobile commerce business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, March 9, 2012

How Far Could PayPal Go in Virtual Payments?

You might draw a couple of conclusions from PayPal's heightened profile in the retail payments space. You might argue that PayPal, of all the present major contenders, is the only company that has a reasonable chance of disintermediating the Visa and MasterCard payment information networks and brands.

You might also conclude that the walls between e-commerce and "commerce" are starting to blur. In the future, the difference between an "online" and a brick and mortar shopping experience might be less clear.

You might further conclude that the "currency tendered" in a transaction increasingly could take on new forms. Today, no matter what form the transaction takes, the payment is in, in the U.S. market, U.S. currency. In the future, other forms of value might be exchanged.

There are lots of legal and regulatory issues to be settled, to be sure. But some transactions might occur in equivalent virtual stores of value such as points, credits, tokens and other forms of stored value. Not that it will happen soon, or at all, but someday the currencies could extend far beyond "U.S. dollars and cents."

In one sense, that is a linear extrapolation from what PayPal now is doing. Rather than tell consumers which payment method is best for them, PayPal is working to accept all types of payments: plastic card, NFC, the new “empty hands” mode or barcode scanning.

Right now, PayPal is simply trying to let consumers decide how to pay, so long as PayPal is part of the transaction clearing, and so long as the currency, no matter what physical "channel," is U.S. currency. In principle, though, markets could develop that allow other virtual currencies to be used, as well.

You might also conclude that the walls between e-commerce and "commerce" are starting to blur. In the future, the difference between an "online" and a brick and mortar shopping experience might be less clear.

You might further conclude that the "currency tendered" in a transaction increasingly could take on new forms. Today, no matter what form the transaction takes, the payment is in, in the U.S. market, U.S. currency. In the future, other forms of value might be exchanged.

There are lots of legal and regulatory issues to be settled, to be sure. But some transactions might occur in equivalent virtual stores of value such as points, credits, tokens and other forms of stored value. Not that it will happen soon, or at all, but someday the currencies could extend far beyond "U.S. dollars and cents."

In one sense, that is a linear extrapolation from what PayPal now is doing. Rather than tell consumers which payment method is best for them, PayPal is working to accept all types of payments: plastic card, NFC, the new “empty hands” mode or barcode scanning.

Right now, PayPal is simply trying to let consumers decide how to pay, so long as PayPal is part of the transaction clearing, and so long as the currency, no matter what physical "channel," is U.S. currency. In principle, though, markets could develop that allow other virtual currencies to be used, as well.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

E-Reader Use Has Double\d Every Year since 2010

Nearly a third of adults in the United States now read books on a tablet or e-book readers.

Only 13 per cent of respondents who currently don't read books electronically said they are "very likely" or "somewhat likely" to start doing so in the next six months.

Some 77 per cent said they are not likely to do so, with half of the group saying they almost certainly won't.

The Harris Poll results, though, might not be reflective of actual user behavior. Many respondents have in the past suggested they would not use e-readers, but their behavior is not congruent with those sentiments.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Will New iPad Boost Mobile Broadband Subscriptions?

The iPad's impact on mobile broadband could be substantial, according to Kevin Smithen, an analyst at Macquarie Securities USA.

Perhaps 30 percent of purchasers of the new device will use it on carriers’ networks, up from less than 20 percent for prior- generation iPads, Smithen says.

For AT&T and Verizon Wireless, that may mean an extra $45 a month per iPad subscriber, on average, Smithen said.

Such forecasts rely on an assumption that the higher definition display and Long Term Evolution fourth generation network capability will entice new iPad users to watch more entertainment video, and to do so in mobile settings outside of home and workplace settings.

Perhaps 30 percent of purchasers of the new device will use it on carriers’ networks, up from less than 20 percent for prior- generation iPads, Smithen says.

For AT&T and Verizon Wireless, that may mean an extra $45 a month per iPad subscriber, on average, Smithen said.

Such forecasts rely on an assumption that the higher definition display and Long Term Evolution fourth generation network capability will entice new iPad users to watch more entertainment video, and to do so in mobile settings outside of home and workplace settings.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amazon Original Progrramming?

It appears Amazon will mirror Netflix, Hulu, and YouTube in funding original content to add distinctiveness to Amazon streaming video services.

Amazon appears to have tipped its hand that it will be funding original content for the Amazon Prime streaming video service in recent days, but video isn't the only area where Amazon is blurring the lines between its role as a distributor and a new role as publisher.

In its books business, for example, Amazon already has become a publishing entity, not simply a retailer of other publishers' products. Something like that is expected for the Amazon Prime streaming service as well.

In that regard, the streaming services are following a business strategy long used by video networks and distributors alike, namely original programming as a way of creating differentiation and uniqueness for a particular service.

Cable TV networks, for example, long have built on a signature series or two to pull viewers into the channel, while most of the fare is more familiar and not "unique" licensed material. That seems to be the same thinking driving investments by Netflix, Hulu and YouTube in original programming not available elsewhere.

Netflix, for example, is producing an original series to be produced by Media Rights Capital. The drama series "House of Cards" will be executive produced and directed by David Fincher and executive produced by, and starring, Kevin Spacey.

Netflix reprtedly got rights to the series by offering a relatively unusual commitment of two seasons, or 26 episodes. Given that the price tag for a high-end drama is in the $4 million to $6 million an episode range and that a launch of a big original series commands tens of millions of dollars for promotion, the deal is believed involve an investment by Netflix of more than $100 million.

Amazon appears to have tipped its hand that it will be funding original content for the Amazon Prime streaming video service in recent days, but video isn't the only area where Amazon is blurring the lines between its role as a distributor and a new role as publisher.

In its books business, for example, Amazon already has become a publishing entity, not simply a retailer of other publishers' products. Something like that is expected for the Amazon Prime streaming service as well.

In that regard, the streaming services are following a business strategy long used by video networks and distributors alike, namely original programming as a way of creating differentiation and uniqueness for a particular service.

Cable TV networks, for example, long have built on a signature series or two to pull viewers into the channel, while most of the fare is more familiar and not "unique" licensed material. That seems to be the same thinking driving investments by Netflix, Hulu and YouTube in original programming not available elsewhere.

Netflix, for example, is producing an original series to be produced by Media Rights Capital. The drama series "House of Cards" will be executive produced and directed by David Fincher and executive produced by, and starring, Kevin Spacey.

Netflix reprtedly got rights to the series by offering a relatively unusual commitment of two seasons, or 26 episodes. Given that the price tag for a high-end drama is in the $4 million to $6 million an episode range and that a launch of a big original series commands tens of millions of dollars for promotion, the deal is believed involve an investment by Netflix of more than $100 million.

Such a move is traditional for premium cable networks trying to increase value and add uniqueness to their services, and Netflix clearly is aware that unique content not available elsewhere will be a draw for its streaming service and subscriptions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"He Who Enrolls, Controls," So Mobile Marketing Will Drive Mobile Commerce

A new study by Juniper Research forecasts that near field communications will facilitate transactions valued at $74 billion globally by 2015 as NFC is increasingly used for the payment of goods in-store and as transport tickets.

So is that a big deal? It depends. U.S. retail spending is something on the order of $3.6 trillion to $4.7 trillion a year, by way of comparison, depending on which purchases one wishes to consider, and exclude. Also, it isn't yet clear how fast NFC-enabled mobile payments might take hold. It is conceivable other methods will grow faster.

But there are some reasons why mobile payments could grow faster. It isn't just consumer demand that will drive transaction volume, but retailer business need, that could provide the adoption trigger.

Richard Crone, CEO, Crone Consulting, notes that mobile banking has become "table stakes."

The more important issues might be that "the entity that enrolls the customer, controls the opportunities." To the extent that mobile payments provides other values, mobile payments might simply be a vehicle for a broader effort to create a better relationship with customers.

"Service interaction in every channel is changing because of mobile," Crone says.

Apps are a way for retailers to expand their customer relationship management efforts and user base. To the extent that mobile payments changes unidentified, anonymous prospects into customers a retailer knows quite a lot about, and can reach, through multiple channels, with the right offers, at the right time, in the right place, mobile payments could grow faster than expected.

Mobile apps, for example, have a strategic role to play in the mobile commerce business, says Crone. “The entity that enrolls the customer, controls the opportunities,” says Crone.

“The second rule is that whoever loads the mobile app controls the transaction sales cycle,” says Crone.

So the increasing use of mobile devices as an alternative to credit cards and paper tickets is one of the fastest growing segments of the mobile commerce market, Juniper Research says.

What might not be so clear is the reason for the change, or the specific implementation.

So is that a big deal? It depends. U.S. retail spending is something on the order of $3.6 trillion to $4.7 trillion a year, by way of comparison, depending on which purchases one wishes to consider, and exclude. Also, it isn't yet clear how fast NFC-enabled mobile payments might take hold. It is conceivable other methods will grow faster.

But there are some reasons why mobile payments could grow faster. It isn't just consumer demand that will drive transaction volume, but retailer business need, that could provide the adoption trigger.

Richard Crone, CEO, Crone Consulting, notes that mobile banking has become "table stakes."

The more important issues might be that "the entity that enrolls the customer, controls the opportunities." To the extent that mobile payments provides other values, mobile payments might simply be a vehicle for a broader effort to create a better relationship with customers.

"Service interaction in every channel is changing because of mobile," Crone says.

Apps are a way for retailers to expand their customer relationship management efforts and user base. To the extent that mobile payments changes unidentified, anonymous prospects into customers a retailer knows quite a lot about, and can reach, through multiple channels, with the right offers, at the right time, in the right place, mobile payments could grow faster than expected.

Mobile apps, for example, have a strategic role to play in the mobile commerce business, says Crone. “The entity that enrolls the customer, controls the opportunities,” says Crone.

“The second rule is that whoever loads the mobile app controls the transaction sales cycle,” says Crone.

So the increasing use of mobile devices as an alternative to credit cards and paper tickets is one of the fastest growing segments of the mobile commerce market, Juniper Research says.

What might not be so clear is the reason for the change, or the specific implementation.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Do Users "Need" Mobile Broadband for Their Tablets?

Do users need a mobile broadband connection for their tablets? Not in all cases, especially when that choice means buying yet one more mobile broadband plan, and when a mobile-capable device costs $100 more than a Wi-Fi-only version.

To the extent that tablets mostly get used in locations where there is Wi-Fi available at no incremental charge, namely home and workplace, there is little marginal incentive, in many cases, to pay a more-expensive device and one additional mobile broadband plan.

Some of us would be that will not fundamentally change until more end users have access to "family or multiple device data plans" that allow a single account to share one bucket of data usage. Those plans are coming, but are not generally available, nor is it clear what the pricing will be.

The expectation would be that such a plan will cost significantly less than buying a separate mobile broadband account for each device on the account.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, March 8, 2012

Apple and Google are Going Toe to Toe in Business Combati8

The new iPhoto for iOS does not use Google Maps. That is a "tell." For the moment, Apple provides its own map solution, but uses data licensed privately from Google. Nobody thinks Apple wants to be in that sort of situation.

Also, Apple has been trying to poach Google Maps employees. Google is watching for patterns that could indicate which direction Apple will try to go in creating its own map solutions.

The latest sign that Google and Apple are going to be head to head competitors across a wide range of hardware and applications businesses is the recent Google announcement that it would be producing a full line of consumer devices.

Also, Siri, Apple's voice search app, is another way Apple is trying to displace Google's search engine as the way people find things, much as Facebook essentially also is doing.

Also, Apple has been trying to poach Google Maps employees. Google is watching for patterns that could indicate which direction Apple will try to go in creating its own map solutions.

The latest sign that Google and Apple are going to be head to head competitors across a wide range of hardware and applications businesses is the recent Google announcement that it would be producing a full line of consumer devices.

Also, Siri, Apple's voice search app, is another way Apple is trying to displace Google's search engine as the way people find things, much as Facebook essentially also is doing.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...