Among enterprises, use of SIP trunking has provided an average 33 percent cost savings over legacy access methods, a study conducted by Webtorials, and sponsored by Sonus Networks, has found.

For 73 percent of respondents, “saving money” was among the key drivers for adoption. But roughly half indicated that ability to use “SIP-specific” features also was an adoption driver.

SIP Trunking, by contrast, is still in the early stages of deployment. In fact, roughly two-thirds of the respondents reported either "Significant Use" or "Extensive Use" of VoIP, while only about one-third of the respondents reported either "Significant Use" or "Extensive Use" of SIP Trunks. Among those using SIP Trunks, significant cost savings have been realized, with an average savings on the order of 33%, Sonus Networks reports.

Some 68 percent of respondents indicated their decisions are driven "mostly by cost savings" or "about equally" by cost and capabilities.

VoIP (89 percent), Unified Communications (69 percent) and video conferencing (65 percent) are the most important types of media to be controlled using SIP.

Monday, August 20, 2012

SIP Trunking Saves 33%

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Leading French Mobile Ops are Between a Rock and a Hard Place

French mobile service providers are between a rock and a hard place. Facing significant competitive pressure that is hitting gross revenues, the incumbent mobile service providers also need to reduce costs to maintain profit margins. But they do not have complete freedom where it comes to those cost cuts.

The French Ministry for the Digital Economy has warned French telecom service providers they may make no job cuts as they restructure to meet the competition.

Iliad, which launched its “Free Mobile” service in January 2012 in France, has been wrecking havoc on its competitors France Telecom, SFR and Bouygues Telecom.

Precisely how the French service providers can make cuts, without touching personnel costs, is a key question, since presumably regulators also do not want any slackening of network capital investment.

Small wonder that many mobile service providers are looking to unload other international assets, in part to reduce debt burdens. But one also wonders whether reducing debt loads is part of an effort to slice operating costs as well.

The French Ministry for the Digital Economy has warned French telecom service providers they may make no job cuts as they restructure to meet the competition.

Iliad, which launched its “Free Mobile” service in January 2012 in France, has been wrecking havoc on its competitors France Telecom, SFR and Bouygues Telecom.

Precisely how the French service providers can make cuts, without touching personnel costs, is a key question, since presumably regulators also do not want any slackening of network capital investment.

Small wonder that many mobile service providers are looking to unload other international assets, in part to reduce debt burdens. But one also wonders whether reducing debt loads is part of an effort to slice operating costs as well.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

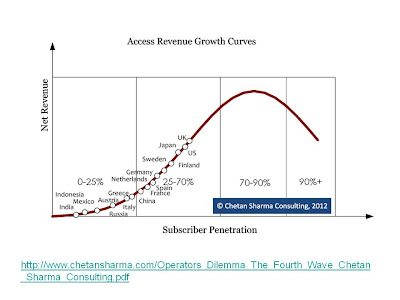

Is Broadband Access One Market, or Many?

It isn't always easy to figure out what a "product" is, for purposes of plotting that "product's" life cycle. Is landline voice "one product," or a series of products that have been offered over the years? Similarly, is "Internet access" one product, or several?

The answer matters, as we can assume any product, including broadband access, will have a product life cycle. But we have to agree on what “the product” is, before we can figure out how to understand the life cycle.

Some might argue that “Internet access” is the product, with successive new generations of products simply reflecting better ways of supplying “Internet access.”

That view would make dial-up, slower speed DSL or cable modem services and now 300 Mbps services products one category. Product managers might not agree, and for good reason. One can plot the rise and fall of "dial-up" Internet access quite distinctly from the adoption of high-speed access services.

The precedent, one might argue, is “voice service.” Over time, the industry has evolved through various types of switching and access technology, but the product category always has been “fixed network voice.”

In a business sense, we can count the number of subscribers served by specific switch technologies, but the business-relevant distinction has remained “total number of lines in service” (access lines in service).

Using that analogy, all forms of Internet access represent one product category. But few are likely to accept that definition so readily.

For starters, there is the simple matter of lead applications for various types of Internet access.

The "killer app" for “dial-up Internet access” was email. That isn't exactly true for the early generations of broadband services, which tended to shift the lead apps to visual Web apps.

Now, streaming video and audio seem to be the lead applications, even though a variety of apps are used by most broadband customers. But as we push to speeds routinely above 20 Mbps, it is likely new lead apps will develop.

Also, there is the matter of mobile broadband access, which arguably gets used in different ways than fixed access. Are those examples of two distinct markets, or one market with segments?

The answer might matter since, In many developed markets, the “fixed network Internet access” product is reaching saturation, where every consumer who wants the product already is buying it. To refresh product lines, and earn more revenue, service providers are relying on faster speed services that sell for higher prices.

But the faster-growing segment is mobile broadband. China, for example, has seen fewer fixed broadband subscribers over the past year, instead of growing.

In other words, fixed broadband accounts actually declined, as users apparently decided to spend their money on mobile broadband, rather than fixed broadband.

Chinese Internet users reached 530 million over the past six months, but the broadband subscriber base actually shrank as mobile became the most popular way for users to get online for the first time, a report by the Chinese government suggests.

Of those users, some 380 million were fixed broadband users, down from 396 million in December 2011, and 388 million were mobile internet users, up from 356 million.

So “mobile broadband access” appears to be a substitute and new product, with a different life cycle, than fixed broadband.

The answer matters, as we can assume any product, including broadband access, will have a product life cycle. But we have to agree on what “the product” is, before we can figure out how to understand the life cycle.

Some might argue that “Internet access” is the product, with successive new generations of products simply reflecting better ways of supplying “Internet access.”

That view would make dial-up, slower speed DSL or cable modem services and now 300 Mbps services products one category. Product managers might not agree, and for good reason. One can plot the rise and fall of "dial-up" Internet access quite distinctly from the adoption of high-speed access services.

The precedent, one might argue, is “voice service.” Over time, the industry has evolved through various types of switching and access technology, but the product category always has been “fixed network voice.”

In a business sense, we can count the number of subscribers served by specific switch technologies, but the business-relevant distinction has remained “total number of lines in service” (access lines in service).

Using that analogy, all forms of Internet access represent one product category. But few are likely to accept that definition so readily.

For starters, there is the simple matter of lead applications for various types of Internet access.

The "killer app" for “dial-up Internet access” was email. That isn't exactly true for the early generations of broadband services, which tended to shift the lead apps to visual Web apps.

Now, streaming video and audio seem to be the lead applications, even though a variety of apps are used by most broadband customers. But as we push to speeds routinely above 20 Mbps, it is likely new lead apps will develop.

Also, there is the matter of mobile broadband access, which arguably gets used in different ways than fixed access. Are those examples of two distinct markets, or one market with segments?

The answer might matter since, In many developed markets, the “fixed network Internet access” product is reaching saturation, where every consumer who wants the product already is buying it. To refresh product lines, and earn more revenue, service providers are relying on faster speed services that sell for higher prices.

But the faster-growing segment is mobile broadband. China, for example, has seen fewer fixed broadband subscribers over the past year, instead of growing.

In other words, fixed broadband accounts actually declined, as users apparently decided to spend their money on mobile broadband, rather than fixed broadband.

Chinese Internet users reached 530 million over the past six months, but the broadband subscriber base actually shrank as mobile became the most popular way for users to get online for the first time, a report by the Chinese government suggests.

Of those users, some 380 million were fixed broadband users, down from 396 million in December 2011, and 388 million were mobile internet users, up from 356 million.

So “mobile broadband access” appears to be a substitute and new product, with a different life cycle, than fixed broadband.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Hosted IP PBX Services Will Grow 300% to 2016

U.S. spending on unified communications technologies will increase by an average of 10 percent per year, led by spending on hosted IP telephony services, which will almost triple between 2011 and 2016, estimates InfoTrack.

Separately, Infonetics Research predicts the number of seats for hosted business VoIP and unified communications services is on track to more than double between 2012 and 2016. Note that forecast includes both hosted IP telephony and UC.

Among U.S. enterprises, defined as firms with 500 or more employees, spending on hosted IPT will grow at an average rate of 27 percent, which is almost two times faster than the average increase among U.S. SMBs (firms with fewer than 500 employees), InfoTrack says.

But over the next five years, the growth of SMB spending on UC apps will be more than twice the rate of U.S. enterprises, which represents the mirror image of what we project happening in the hosted IPT sector," said Ken Dolsky, Senior Program Director for InfoTrack.

As always, one has to keep the size of the installed base in mind when pondering such forecasts. Other researchers, including Parallels, have estimated that small and medium business hosted IP telephony penetration is still relatively small.

The global market for hosted PBX (hosted IP telephony) services averaged between four percent and seven percent in the largest SMB markets, Parallels noted, as recently as late 2011.

Infonetics Research separately has forecast that the global SMB VoIP services market would grow to $76.1 billion in 2015 with total subscribers of 262 million. Keep in mind that the total global telecom services business accounts for about $2 trillion in annual revenue in 2012.

So hosted IP telephony would represent about four percent of global revenues.

In the United States, it has been estimated that around 500,000 SMBs currently use a hosted PBX service, representing an $800 million market. In a U.S. telecom service business of about $336 billion in annual revenue, hosted IP telephony represents about two-tenths of one percent of total industry revenue.

However, Parallels estimates that the majority of the current in-house PBX systems will migrate to hosted mechanisms over time, representing $3.9 billion potential market for hosted PBX.

US Hosted PBX Market – Source: Parallels SMB Cloud Insights Report, 2011

Separately, Infonetics Research predicts the number of seats for hosted business VoIP and unified communications services is on track to more than double between 2012 and 2016. Note that forecast includes both hosted IP telephony and UC.

Among U.S. enterprises, defined as firms with 500 or more employees, spending on hosted IPT will grow at an average rate of 27 percent, which is almost two times faster than the average increase among U.S. SMBs (firms with fewer than 500 employees), InfoTrack says.

These days, though, estimating the size of the global market for business IP telephony services offered by service providers is a hard question to answer. For starters, IP telephony can include sales of IP private branch exchanges, unified communications solutions and services, hosted IP telephony services, access services such as SIP trunking and fees earned for managing premises business phone systems.

With all of this, the global business IP telephony market will reach $20.8 billion by the year 2018, according to Global Industry Analysts. The problem, of course, is that it is tough to make sense of global estimates, especially without knowing in some detail which specific products are included in that figure.

The global market for hosted PBX (hosted IP telephony) services averaged between four percent and seven percent in the largest SMB markets, Parallels noted, as recently as late 2011.

The global market for hosted PBX (hosted IP telephony) services averaged between four percent and seven percent in the largest SMB markets, Parallels noted, as recently as late 2011.

Infonetics Research separately has forecast that the global SMB VoIP services market would grow to $76.1 billion in 2015 with total subscribers of 262 million. Keep in mind that the total global telecom services business accounts for about $2 trillion in annual revenue in 2012.

So hosted IP telephony would represent about four percent of global revenue.

In the United States, it has been estimated that around 500,000 SMBs currently use a hosted PBX service, representing an $800 million market. In a U.S. telecom service business of about $336 billion in annual revenue, hosted IP telephony represents about two-tenths of one percent of total industry revenue.

In the United States, it has been estimated that around 500,000 SMBs currently use a hosted PBX service, representing an $800 million market. In a U.S. telecom service business of about $336 billion in annual revenue, hosted IP telephony represents about two-tenths of one percent of total industry revenue.

However, Parallels estimates that the majority of the current in-house PBX systems will migrate to hosted mechanisms over time, representing $3.9 billion potential market for hosted PBX.

At the moment, it remains the case that most business IP telephony is supplied by premises-based solutions.

So how big is the business IP telephony? It depends on who you ask, and what the assumptions are.

"In 2011, SMBs represented 46 percent of the U.S. installed base of IPT lines, but accounted for only 30 percent of the spending on UC applications,” InfoTrack says. But over the next five years, the growth of SMB spending on UC apps will be more than twice the rate of U.S. enterprises, which represents the mirror image of what we project happening in the hosted IPT sector," said Ken Dolsky, Senior Program Director for InfoTrack.

As always, one has to keep the size of the installed base in mind when pondering such forecasts. Other researchers, including Parallels, have estimated that small and medium business hosted IP telephony penetration is still relatively small.

The global market for hosted PBX (hosted IP telephony) services averaged between four percent and seven percent in the largest SMB markets, Parallels noted, as recently as late 2011.

Infonetics Research separately has forecast that the global SMB VoIP services market would grow to $76.1 billion in 2015 with total subscribers of 262 million. Keep in mind that the total global telecom services business accounts for about $2 trillion in annual revenue in 2012.

So hosted IP telephony would represent about four percent of global revenues.

In the United States, it has been estimated that around 500,000 SMBs currently use a hosted PBX service, representing an $800 million market. In a U.S. telecom service business of about $336 billion in annual revenue, hosted IP telephony represents about two-tenths of one percent of total industry revenue.

However, Parallels estimates that the majority of the current in-house PBX systems will migrate to hosted mechanisms over time, representing $3.9 billion potential market for hosted PBX.

US Hosted PBX Market – Source: Parallels SMB Cloud Insights Report, 2011

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Mobile Industry Will Reach Milestone Sometime After 2016

Data revenue will grow to 65 percent of total U.S. wireless service revenue as voice declines to 35 percent in 2016, according to Hugues de la Vergne, principal research analyst at Gartner. That might not seem so significant, but keep in mind that, in recent decades, voice has represented at least 70 percent of all industry revenues.

A replacement of voice revenues by data revenues at that level would be a key milestone for an industry that has for some time been grappling with the issue of how to replace lost voice revenue and profit margin.

Growing adoption of smart phones, with the new and significant data plan revenue, will play a key role, of course. Almost by definition, a smart phone activation will come with a boost in monthly revenue, from data access, of $20 to $40 a month.

But different retail packaging likely will play a key role. New shared data plans offered by AT&T and Verizon Wireless are intended to lift overall revenues while creating a usage-based data revenue model, while encouraging users to add tablets to their accounts for mobile broadband access.

What remains unclear is the extent of demand for such plans. Some think the entire industry eventually will move in that direction, as was the case with some earlier packaging innovations, including the mobile industry's abolition of domestic long distance with AT&T's Digital One Rate, or the adoption of family plans for domestic voice and texting.

But that is far from a universal view. T-Mobile USA, for example, has argued that the plans are not advantageous for consumers. And there are many subtleties. Most believe that the new plans primarily will encourage smart phone adoption, and secondarily tablet mobile connections.

Some of us might argue it is possible that the big secondary effect will be to lift personal mobile hotspot service sales, not the additional mobile network connections for tablets. The reason is that a personal mobile hotspot capability solves the same problem as a paid mobile connection for a tablet, and also has additional value.

When the personal hotspot capability is provided by the smart phone, there is no need to carry another device, such as a dongle or discrete hotspot device. Also, the personal hotspot conveniently can connect multiple devices, where a dongle connects only one device.

But that isn’t the only potential way data revenues might grow. As the number of devices with mobile network modems increases, so will the number of instances where it makes sense to have mobile network broadband.

The issue is whether that also will lead to demand for multi-device data rate plans, as Gartner believes.

The disagreement about adoption probably will not be decided, one way or the other, for some time. The reason is that the current structure of the shared data plans does not offer significantly better economics for users, compared to what they already can buy.

There are some marginal advantages and inducements to add tablet devices, for example, but the price advantage might not be so obvious to most users, or valuable.

But Gartner believes multi-device rate plans will be a key driving factor in the expansion of U.S. data revenue from $81.4 billion in 2011 to $151.9 billion in 2016.

Voice represents something on the order of 72 percent percent of total mobile service provider revenue, according to ABI Research estimates.

Messaging represents about 21 percent of total revenue, so declining messaging revenue is less a problem than lost voice revenue.

Mobile Internet revenue still is growing, in every market, so there is more time to react to the eventual maturation of that market, which at the moment only represents about six percent of total mobile service provider revenue globally, by ABI Research estimates.

The rate of mobile data revenue growth is important because voice revenues are declining. ABI Research also forecasts annual mobile voice revenues to reach $580 billion in 2010.

From 2011 on, rising subscriber saturation will increasingly erode mobile voice revenues, not just in developed markets but also in a number of emerging markets. By 2014, mobile voice revenues will have contracted by 9.6 percent.

While mobile operators have received a substantial boost from value-added services such as messaging and mobile Internet, competition is squeezing margins for a variety of services and carriers. Total mobile data services should generate $169 million in 2009 and will grow at a compound annual growth rate of nine percent until 2014.

By the end of 2009 the declines in annual average revenue per user (ARPU) will have been felt most severely in Asia-Pacific (-8.7% to $105) and Africa (-7.8% to $134). ARPU in 2009 in North America will have contracted, but only by -0.6% to $526).

All that means mobile service providers will have to work to resist voice revenue erosion while simultaneously growing data revenues.

A replacement of voice revenues by data revenues at that level would be a key milestone for an industry that has for some time been grappling with the issue of how to replace lost voice revenue and profit margin.

Growing adoption of smart phones, with the new and significant data plan revenue, will play a key role, of course. Almost by definition, a smart phone activation will come with a boost in monthly revenue, from data access, of $20 to $40 a month.

But different retail packaging likely will play a key role. New shared data plans offered by AT&T and Verizon Wireless are intended to lift overall revenues while creating a usage-based data revenue model, while encouraging users to add tablets to their accounts for mobile broadband access.

What remains unclear is the extent of demand for such plans. Some think the entire industry eventually will move in that direction, as was the case with some earlier packaging innovations, including the mobile industry's abolition of domestic long distance with AT&T's Digital One Rate, or the adoption of family plans for domestic voice and texting.

But that is far from a universal view. T-Mobile USA, for example, has argued that the plans are not advantageous for consumers. And there are many subtleties. Most believe that the new plans primarily will encourage smart phone adoption, and secondarily tablet mobile connections.

Some of us might argue it is possible that the big secondary effect will be to lift personal mobile hotspot service sales, not the additional mobile network connections for tablets. The reason is that a personal mobile hotspot capability solves the same problem as a paid mobile connection for a tablet, and also has additional value.

When the personal hotspot capability is provided by the smart phone, there is no need to carry another device, such as a dongle or discrete hotspot device. Also, the personal hotspot conveniently can connect multiple devices, where a dongle connects only one device.

But that isn’t the only potential way data revenues might grow. As the number of devices with mobile network modems increases, so will the number of instances where it makes sense to have mobile network broadband.

The issue is whether that also will lead to demand for multi-device data rate plans, as Gartner believes.

The disagreement about adoption probably will not be decided, one way or the other, for some time. The reason is that the current structure of the shared data plans does not offer significantly better economics for users, compared to what they already can buy.

There are some marginal advantages and inducements to add tablet devices, for example, but the price advantage might not be so obvious to most users, or valuable.

But Gartner believes multi-device rate plans will be a key driving factor in the expansion of U.S. data revenue from $81.4 billion in 2011 to $151.9 billion in 2016.

Voice represents something on the order of 72 percent percent of total mobile service provider revenue, according to ABI Research estimates.

Messaging represents about 21 percent of total revenue, so declining messaging revenue is less a problem than lost voice revenue.

Mobile Internet revenue still is growing, in every market, so there is more time to react to the eventual maturation of that market, which at the moment only represents about six percent of total mobile service provider revenue globally, by ABI Research estimates.

The rate of mobile data revenue growth is important because voice revenues are declining. ABI Research also forecasts annual mobile voice revenues to reach $580 billion in 2010.

From 2011 on, rising subscriber saturation will increasingly erode mobile voice revenues, not just in developed markets but also in a number of emerging markets. By 2014, mobile voice revenues will have contracted by 9.6 percent.

While mobile operators have received a substantial boost from value-added services such as messaging and mobile Internet, competition is squeezing margins for a variety of services and carriers. Total mobile data services should generate $169 million in 2009 and will grow at a compound annual growth rate of nine percent until 2014.

By the end of 2009 the declines in annual average revenue per user (ARPU) will have been felt most severely in Asia-Pacific (-8.7% to $105) and Africa (-7.8% to $134). ARPU in 2009 in North America will have contracted, but only by -0.6% to $526).

All that means mobile service providers will have to work to resist voice revenue erosion while simultaneously growing data revenues.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Dunkin Donuts Launches Own Mobile Payment App

Dunkin’ Donuts has launched its first-ever mobile application for payment and gifting for iPhone, iPod touch and Android smartphones. With the new Dunkin’ App, paying for food, beverages, and merchandise at Dunkin’ Donuts restaurants throughout the U.S. is as simple and speedy as scanning a smart phone using a mobile Dunkin' Donuts Card in-store or at the drive-through, according to Mobile Commerce.

The "mGift" feature also allows users to send virtual gift cards using text message, email, and Facebook Connect.

The "mGift" feature also allows users to send virtual gift cards using text message, email, and Facebook Connect.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Consumers Not So Hot on Network Connected Tablets, Apparently

According to Engadget, AT&T has ended its subsidies for tablets sold with mobile data plans. You can make your own decisions about why the program is ending, but there might be a parallel with the earlier carrier experiments with subsidized netbooks.

You might argue the value-price relationship is not perceived as adequate. You might argue that with pervasive Wi-Fi, people don't quite so often "need" a network-provided data plan. You might argue people prefer devices other than the ones AT&T had been offering.

You can argue all of those could be reasons for lukewarm customer interest. You might also argue that AT&T doesn't want to incur the financing cost.

Whatever your choice of reasons, there still does not seem to be a big move by consumers to pay for tablet mobile connections, even though some predict that will happen. Wi-Fi-only devices typically outsell units equipped for 3G access, for example.

The ratio of Wi-Fi-only tablets tablet sales with carrier network connections, for example, is highly skewed to Wi-Fi-only devices.

You might argue the value-price relationship is not perceived as adequate. You might argue that with pervasive Wi-Fi, people don't quite so often "need" a network-provided data plan. You might argue people prefer devices other than the ones AT&T had been offering.

You can argue all of those could be reasons for lukewarm customer interest. You might also argue that AT&T doesn't want to incur the financing cost.

Whatever your choice of reasons, there still does not seem to be a big move by consumers to pay for tablet mobile connections, even though some predict that will happen. Wi-Fi-only devices typically outsell units equipped for 3G access, for example.

The ratio of Wi-Fi-only tablets tablet sales with carrier network connections, for example, is highly skewed to Wi-Fi-only devices.

Consumers appear to avoid getting tablet mobile service plans, preferring to run tablets on Wi-Fi networks.

With nearly 50 million tablets in the U.S. market, carrier-networked devices constitute roughly eight percent of the total.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...