You might think "things cost what they cost," and that is true, but what things cost varies from place to place

Recent studies published by ITU reveal that broadband penetration is directly related to its cost, relative to an average family income, as well as to the availability of products and services that accommodate the general population’s purchasing ability.

That also explains why high speed access costs vary rather broadly from country to country. Areas where it costs more to create the infrastructure will tend to be more expensive, at the retail level. Areas where it costs less to create networks will correlate with lower retail costs.

For example, as the annual cost of broadband drops below three percent of a family’s annual income, broadband usage begins to increase dramatically.

For developed countries, this relative cost has already been achieved, but for at least 34 countries worldwide, the cost of broadband remains higher than the average annual family income, the ITU says.

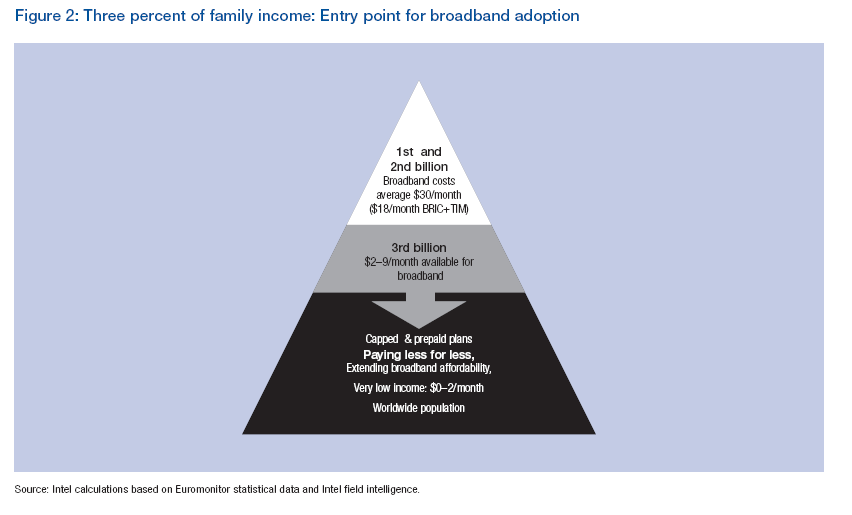

But that’s an important bit of retail pricing advice for would-be ISPs in developing regions: set monthly prices no higher than three percent of median household income.

And prices are falling, globally.Between 2008 and 2009, 125 countries saw reductions in access prices, some by as much as 80 percent, the ITU says. Between 2009 and 2011, for example, prices for fixed broadband have dropped by 52.2 percent on average and mobile broadband prices by 22 percent, globally.

Affordable broadband programs are starting to emerge in countries such as Sri Lanka and India, with service providers offering connectivity solutions starting as low as US$2 per month.

And while it is natural for a seller to want higher prices, for Internet access providers, less is more, in the sense of keeping at or below the “three percent of median household income” rule for retail pricing.

The trade-off is lower average revenue per user, but many more users. So where median high speed access costs in developed regions might run about $30 a month, in the BRIC+TIM areas costs might be $18 a month.

Somewhere between $2 and $9 a month would reach another billion or so households in a number of regions and countries. In the poorest nations, prepaid plans costing less than $2 a month will be needed.

Brazil, Russia, India, China, Turkey, Indonesia, and Mexico (BRIC+TIM countries), for example, could grow their available market by 860 million people by reducing the cost of entry for broadband by about 50 percent..

In 2011, the price of fixed broadband access cost less than two percent of average monthly income in 49 economies in the world, mostly in the industrialized world.

Meanwhile, broadband access cost more than half of average national income in 30 economies. In 19 of the lesser developed countries, the price of broadband exceeds average monthly income.

By 2011, there were 48 developing economies where entry-level broadband access cost less than five percent of average monthly income, up from just 35 countries the year before.

To take the example of Kenya, family income levels mean that only about seven percent of the population can afford a service that offers uncapped monthly broadband access for US$20 per month. A prepaid broadband access service capped at 200 MB of data for US$5, however, could be within the reach of more than 60 percent of the Kenyan population.

Safaricom, the largest Internet service provider in Kenya, launched a segmented prepaid broadband offer in the end of 2009 targeted at different income levels.

There were 589 million fixed broadband subscriptions by the end of 2011 (most of which were located in the developed world), but nearly twice as many mobile broadband subscriptions at 1.09 billion, the ITU says.

Beyond that, since trenches, ducts and dark fiber represent as much as 70 percent of total cost to build a broadband network, the wisdom of using wireless is obvious. Wireless attacks that part of the effort consuming up to 70 percent of capital investment.