In 2000, one might still have looked at tele-density figures for Africa and south Asia and still have concluded that not much was happening, in terms of adoption.

But that changed, sometime around 2004, when a growth inflection point was reached, both in terms of income and use of mobile phones.

That change in growth means traditional barriers to Internet use, on the demand side, will fall rapidly over the next couple of decades.

Though rural areas will progress at a slower rate than urban areas, change will be rapid, especially against the background of how much change happened over the last 100 years.

Currently not even half of Africa’s countries are what the World Bank calls “middle income” (defined as at least $1,000 per person a year), by 2025 the bank expects most African countries to have reached that stage.

That’s important. Statistics showing wide disparities in use of the Internet around the world are snapshots in time.

What is equally important is the pace of change. One might have argued, based on statistics from 1990 or 2000, that many in developing regions, nothing much was happening.

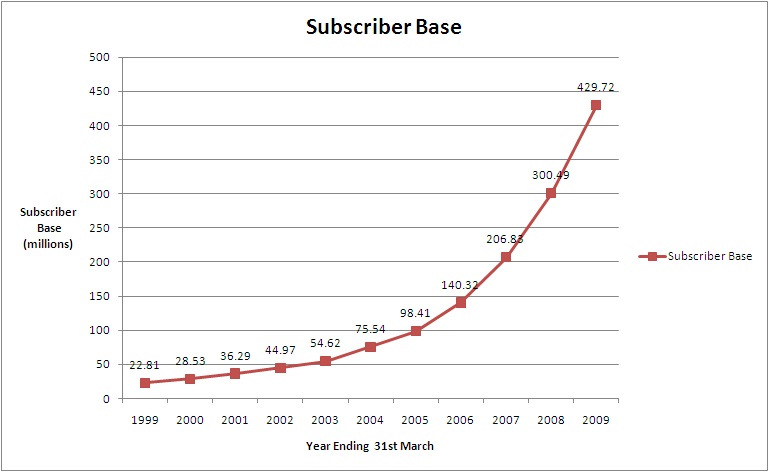

But an inflection point occurred, in India for example, around 2004. Much the same happened in Africa.

Over the past ten years real income per person in Africa has increased by more than 30 percent. In the prior two decades real income per person shrank by nearly 10 percent.

Africa is the world’s fastest-growing continent now.

Over the next decade its gross domestic product is expected to rise by an average of six percent a year. Foreign investment is helping.

Africa has three mobile phones for every four people, the same as India. By 2017 nearly 30 percent of households are expected to have a television set, an almost 500-percent increase over ten years.

In sub-Saharan Africa, secondary-school enrollment grew by 48 percent between 2000 and 2008.

Over the past decade, malaria deaths in some of the worst-affected countries have declined by 30 percent and HIV infections by up to 74 percent.

The point is that the Internet access gap is going to close, and relatively quickly, even in the regions and areas where the gaps are largest. The large mobile service providers likely will be providing most of the supply. But it is not unreasonable to predict that many independent ISPs also will emerge.