Mexico now has become a focal point for potential market change after Mexican President Enrique Peña Nieto signed into law a new framework for competition in the telecommunications and TV broadcast industries that has the express aim of limiting market power and shifting market share in Mexico’s communications and media businesses.

Mexico now has become a focal point for potential market change after Mexican President Enrique Peña Nieto signed into law a new framework for competition in the telecommunications and TV broadcast industries that has the express aim of limiting market power and shifting market share in Mexico’s communications and media businesses.

In essence, the bill allows for something like the 1984 breakup of the AT&T Bell system, though it isn’t clear that is the preferred method for altering market share in the Mexican markets.

At least initially, regulators are likely to try new network unbundling and interconnection rates that will favor competitors. Just how much share could change is the big question. In the U.S. market and in Western Europe, competition has in many cases reduced the former market leader’s share to as little as 30 percent to 35 percent.

But that required asset divestitures. In the absence of such asset disposals, some of the existing competitors might expect to gain perhaps 10 percent to 15 percent share.

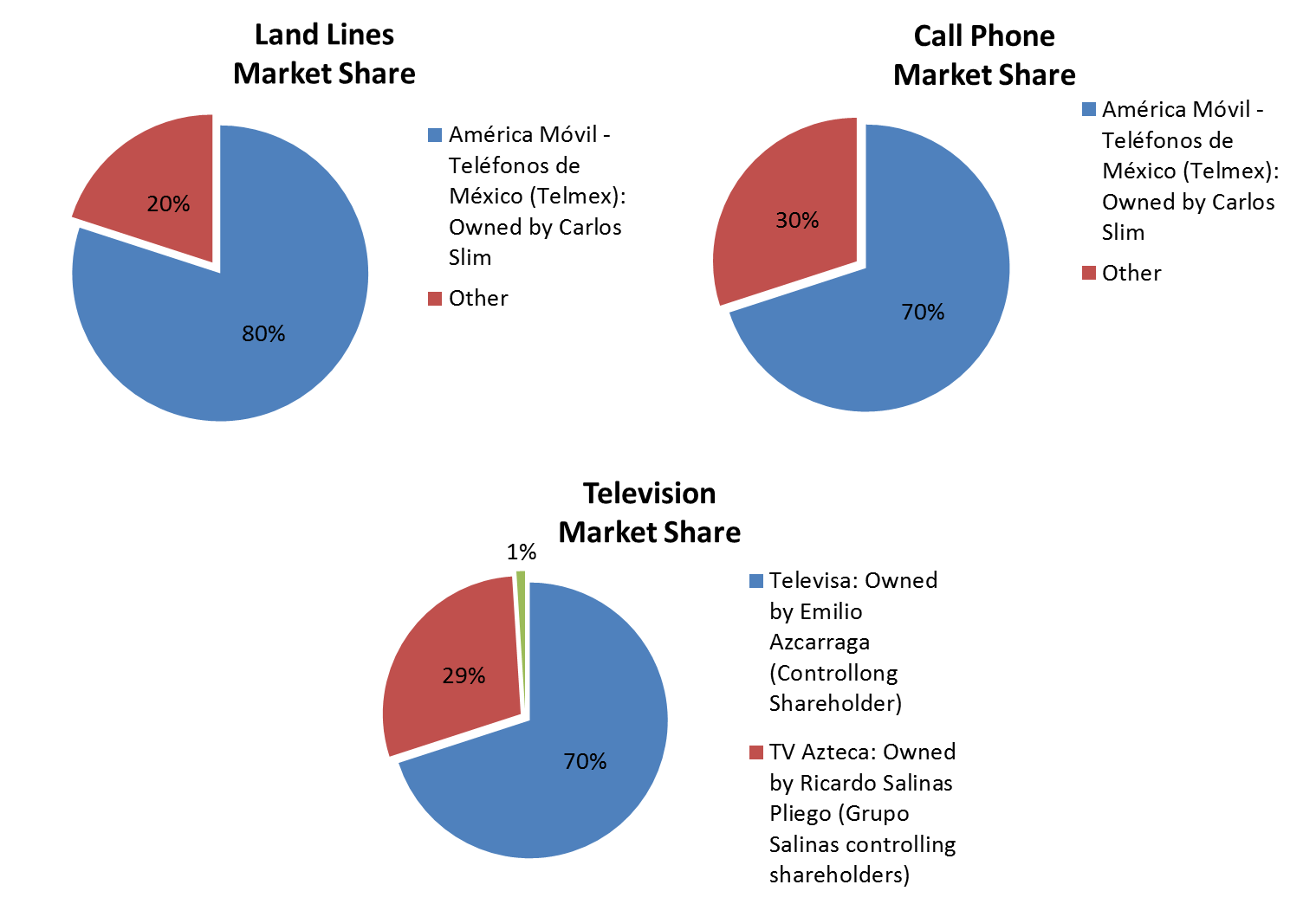

What is clear is that the “problem” is seen to be excessive market control by one company, in this case América Móvil, which has 80 percent share of fixed lines and also 70 percent share of mobile accounts as well.

The new law creates a brand new regulatory body, Ifetel, which will have the ability to apply more restrictive regulations on dominant competitors or force them to sell assets.

But Grupo Televisa likewise controls 70 percent of the broadcast TV market, and also is expected to see new competition, ironically from Carlos Slim, who controls América Móvil.

One way or the other, regulators will take actions to reduce the market share held by the leaders of the fixed line, mobile and TV broadcast industries. That, of course, is the whole point of inducing new competition: the leaders lose market share.

Two new national television networks will be authorized, and existing satellite and cable TV companies will be required to carry those signals at no charge to the new networks.

Aside from changes in interconnection rates to favor attackers, foreign businesses will be permitted to own up to 49 percent (up from zero percent) of radio firms, and can increase their stake to 100 percent (up from 49 percent) in other telecommunications operations.