Trying to figure out how much “damage” Skype and other over the top voice apps have done to international voice is a difficult exercise. Skype gets used where the alternative would have been “no call,” so Skype usage volumes partly represent incremental usage that actually does not cannibalize existing revenue.

Trying to figure out how much “damage” Skype and other over the top voice apps have done to international voice is a difficult exercise. Skype gets used where the alternative would have been “no call,” so Skype usage volumes partly represent incremental usage that actually does not cannibalize existing revenue.

On the other hand, there also are instances where Skype or other over the top apps will be used as a substitute for a long distance call using the public network.

The same sort of issue applies to messaging apps displacing text messaging. Some over the top messaging is activity that would not have happened were text messaging the only alternative.

And some OTT messaging gets used in place of text messaging.

Also, as typically is the case for Internet apps, usage is not the same thing as revenue.

Also, as typically is the case for Internet apps, usage is not the same thing as revenue.

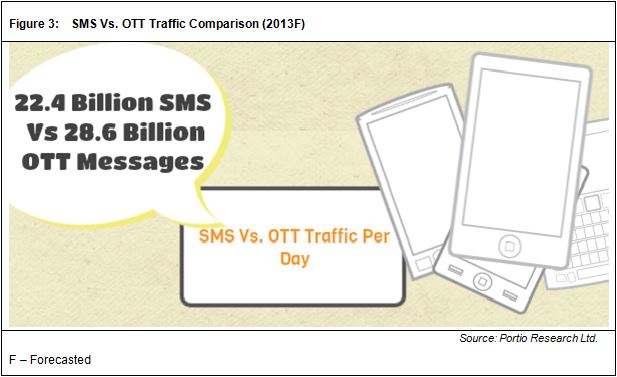

“During 2012 and 2013 we have seen many reports that operators are losing $20 billion to $30 billion in SMS revenue to OTT messaging apps,” said Karl Whitfield, a Director at Portio Research. “We see reports that OTT traffic will be double that of SMS by the end of 2013. This is wrong on both counts.”

It may be true that SMS revenues are levelling off and that OTT is on the rise, but SMS is still generating revenues of $15.3 million per hour, 24/7, that’s a massive $133.8 billion in 2013, Whitfield says.

Over the top apps generate about $3 million an hour, by way of comparison.

Worldwide SMS revenue has gone up year after year since the early 1990s and will continue to be above 2010 levels until 2017, Whitfield said.

In fact, in some markets, SMS and OTT apps are coexisting, serving end users in different ways.

There is a huge uptake of OTT messaging in Japan, particularly with local player LINE, yet the SMS market remains healthy and stable, he says.

The same goes for South Korea, where KakaoTalk is enjoying huge success; here again the SMS market remains stable and is not declining as many predicted.

The same goes for South Korea, where KakaoTalk is enjoying huge success; here again the SMS market remains stable and is not declining as many predicted.

Where SMS has seen a decline, in markets such as Spain and Greece, there has been an overall fall in subscribers and revenues at the same time.

“Our research into mobile messaging completely contradicts what some other industry observers are saying,” said Whitfield.

Karl Whitfield

Global OTT and P2P Messaging Traffic (Billions)

|

2010

|

2011

|

2012

|

2013F

|

2014F

|

2015F

|

2016F

|

2017F

| |

P2P SMS

|

5,812

|

6,546

|

6,623

|

6,687

|

6,654

|

6,522

|

6,304

|

5,931

|

OTT Messaging

|

1,494

|

3,840

|

6,774

|

10,452

|

14,970

|

20,437

|

26,359

|

32,141

|