Speculation about whether leading application providers will ever want to become Internet access providers in their own right is not new. In fact, as Google has formally become an Internet service provider (Google Fiber, Starbucks Wi-Fi and other smaller tests) and has owned mobile spectrum, plus been a bidder on new spectrum, at least one app provider already has made the leap.

Now Amazon is said to have conducted testing of mobile or wireless network performance, using spectrum controlled by satellite communications company Globalstar. To be sure, companies test all sorts of things from time to time.

So the move does not necessarily mean Amazon has decided to become more active in the ISP business. One might simply note that Amazon is indirectly involved already. It buys capacity from mobile service providers to deliver content to Kindle devices.

As T-Mobile US and SoftBank-owned Sprint make assaults on the existing structure of the mobile market, many would argue an equally big disruption could come from the entry of a major application provider such as Amazon into the mobile or untethered ISP business.

Some say Amazon is testing a new untethered protocol, not Long Term Evolution.

Friday, August 23, 2013

Amazon Weighing its Own Mobile Network?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, August 22, 2013

Google Project Loon (Internet by Balloon) Continues Testing

Project Loon is an effort Google is making to evaluate whether it is possible to provide Internet access using free-floating balloons that will drift with the wind west to east south of the equator.

Project Loon is an effort Google is making to evaluate whether it is possible to provide Internet access using free-floating balloons that will drift with the wind west to east south of the equator.Given a sufficiently large fleet of balloons with a bit of maneuverability, Google wants to understand whether such balloons can be used to provide low-cost Internet access to hundreds of millions, if not a billion people in the southern hemisphere.

Recently, Project Loon says, it has been conducting research flights in California’s Central Valley, testing power systems (solar panel orientation and batteries), envelope design, and radio configuration.

"On our most recent research flight we overflew Fresno, a nearby city, to get statistics on how the presence of lots of other radio signals (signal-noise) in cities affects our ability to transmit Internet," Project Loon says.

"It turns out that providing Internet access to a busy city is hard because there are already many other radio signals around, and the balloons’ antennas pick up a lot of that extra noise," Project Loon staffers say.

This increases the error-rate in decoding the Loon signal, so the signal has to be transmitted multiple times, decreasing the effective bandwidth.

That is just one of the practical issues Project Loon has to overcome. At a completely different level, there is the issue of how nations might react to balloons overflying airspace. Project Loons do not orbit in space, and neither do they fly as high as airliners.

But that might raise some sovereignty issues. Not every national government truly wants its people to have unfettered access to information.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Are Mobile Networks a Viable Substitute for Fixed Networks?

Are mobile networks a viable substitute product for services provided by fixed networks?

As with most big questions, the answers are nuanced. Though some would still point to the utility of emergency calling services, most consumer observers and users have voted with their wallets in favor of the notion that mobile voice is, in fact, a nearly perfect substitute for fixed voice service.

The extent to which mobile works equally as well for business voice is less obvious, but views continue to change.

Perhaps the bigger issue is whether mobile is a viable substitute for wired network broadband services.

And there the notion of “perfect substitute” works less well. Mobile networks require spectrum resources that are more finite than the bandwidth that can be delivered by waveguide networks, and always will be more finite.

In principle, waveguide networks can use spectrum far broader than available to mobile or any other over the air networks.

And each waveguide network can reuse the same bandwidth as that used by its competitors, in the same locations, something that is impossible for mobile and other over the air networks using licensed spectrum.

In developed markets, the contrasts are more stark. In emerging markets, the practical choice is not between a more-limited mobile network and a fiber network, but between a mobile network and no network.

The other crucial difference between fixed and mobile networks lies not just in bandwidth, but in the cost of using that bandwidth.

On a cost-per-bit basis, a wired network will always have an advantage over a mobile network.

A laptop‑based wireless broadband basket (offers within the 500 MB per month range) cost USD 13.04 on average across the OECD in purchasing power parity (PPP) terms, although it reached USD 30 in some countries.

That is equivalent to $26 per GB of usage. As always, price per GB drops as the size of usage buckets increases. Average expenditure was USD 37.15 for a 10 GB basket. A 5 GB basket for tablets cost USD 24.74 on average, but varied from USD 7.98 (Finland) to USD 61.84 (New Zealand).

Consider that many wired network plans either have no usage limits (Google Fiber and some others) or usage limits as high as 250 GB a month, for prices of perhaps USD 50.

The point is that although mobile Internet access might be roughly comparable for moderate usage scenarios, wired networks win, hands down, for high usage scenarios. And mobile networks are more expensive at low usage levels.

Using the OECD data, one can calculate that the price per gigabyte of usage is about $3.71 to $4.81 for a mobile broadband plan (just a dongle). The wired network might cost $5 to $10 per GB.

As with most big questions, the answers are nuanced. Though some would still point to the utility of emergency calling services, most consumer observers and users have voted with their wallets in favor of the notion that mobile voice is, in fact, a nearly perfect substitute for fixed voice service.

The extent to which mobile works equally as well for business voice is less obvious, but views continue to change.

Perhaps the bigger issue is whether mobile is a viable substitute for wired network broadband services.

And there the notion of “perfect substitute” works less well. Mobile networks require spectrum resources that are more finite than the bandwidth that can be delivered by waveguide networks, and always will be more finite.

In principle, waveguide networks can use spectrum far broader than available to mobile or any other over the air networks.

And each waveguide network can reuse the same bandwidth as that used by its competitors, in the same locations, something that is impossible for mobile and other over the air networks using licensed spectrum.

In developed markets, the contrasts are more stark. In emerging markets, the practical choice is not between a more-limited mobile network and a fiber network, but between a mobile network and no network.

The other crucial difference between fixed and mobile networks lies not just in bandwidth, but in the cost of using that bandwidth.

On a cost-per-bit basis, a wired network will always have an advantage over a mobile network.

A laptop‑based wireless broadband basket (offers within the 500 MB per month range) cost USD 13.04 on average across the OECD in purchasing power parity (PPP) terms, although it reached USD 30 in some countries.

That is equivalent to $26 per GB of usage. As always, price per GB drops as the size of usage buckets increases. Average expenditure was USD 37.15 for a 10 GB basket. A 5 GB basket for tablets cost USD 24.74 on average, but varied from USD 7.98 (Finland) to USD 61.84 (New Zealand).

Consider that many wired network plans either have no usage limits (Google Fiber and some others) or usage limits as high as 250 GB a month, for prices of perhaps USD 50.

The point is that although mobile Internet access might be roughly comparable for moderate usage scenarios, wired networks win, hands down, for high usage scenarios. And mobile networks are more expensive at low usage levels.

Using the OECD data, one can calculate that the price per gigabyte of usage is about $3.71 to $4.81 for a mobile broadband plan (just a dongle). The wired network might cost $5 to $10 per GB.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Why Over the Top TV Won't Necessarily Save You Money

It's too early to say whether most consumers will save money if, one day, they are able to buy TV shows one by one, or at least channel by channel. Logic suggests people should be able to save money.

They might buy fewer channels, since most people actually watch seven to 12 of all the channels they pay for as part of a cable TV, satellite TV or telco TV subscription. In principle, that could offer some savings.

The same logic might apply to purchases of single shows.

And you might think that "cutting out the middleman" (cable TV, satellite TV or telco TV supplier) would offer a further chance to save money on retail purchases of content.

Maybe. Maybe not. Ignore for the moment the issue of whether higher Internet access spending will be one incrementally higher cost to pay, since all that TV consumption will chew through perhaps a gigabyte an hour.

If a person watches TV five hours a day, that's 35 gigabytes a week, and 140 GB a month. If there is more than one viewer in a household, the numbers will likely be higher, since it is quite rare for two or more people to prefer to watch exactly the same content, at exactly the same time, in the same location within a home.

Also, use of digital video recorders also will consume bandwidth at the same rate as watching real-time TV.

DirecTV pays $1 billion a year for Sunday Ticket. DirecTV earns about $725 million a year in Sunday Ticket revenue from about 2.8 million subscribers, Citigroup estimates.

Switching to online delivery will not automatically change those economics in a helpful way, either for a provider or a subscriber.

Perhaps the answer to many such questions involves asking what Google might do. But you see the point: content costs alone, irrespective of marketing, network and operations costs, make content an "expensive" item.

And make no mistake, nobody in the content business is dumb. Content distribution changes only when content owners think they can switch, and still make as much, or more money than before.

So only after widespread licensing of content occurs will we be able to ascertain whether linear TV is necessarily more expensive than over the top alternatives. In many cases, some of us would be willing to bet, "saving money" will not be so easy.

They might buy fewer channels, since most people actually watch seven to 12 of all the channels they pay for as part of a cable TV, satellite TV or telco TV subscription. In principle, that could offer some savings.

The same logic might apply to purchases of single shows.

And you might think that "cutting out the middleman" (cable TV, satellite TV or telco TV supplier) would offer a further chance to save money on retail purchases of content.

Maybe. Maybe not. Ignore for the moment the issue of whether higher Internet access spending will be one incrementally higher cost to pay, since all that TV consumption will chew through perhaps a gigabyte an hour.

If a person watches TV five hours a day, that's 35 gigabytes a week, and 140 GB a month. If there is more than one viewer in a household, the numbers will likely be higher, since it is quite rare for two or more people to prefer to watch exactly the same content, at exactly the same time, in the same location within a home.

Also, use of digital video recorders also will consume bandwidth at the same rate as watching real-time TV.

DirecTV pays $1 billion a year for Sunday Ticket. DirecTV earns about $725 million a year in Sunday Ticket revenue from about 2.8 million subscribers, Citigroup estimates.

Switching to online delivery will not automatically change those economics in a helpful way, either for a provider or a subscriber.

Perhaps the answer to many such questions involves asking what Google might do. But you see the point: content costs alone, irrespective of marketing, network and operations costs, make content an "expensive" item.

And make no mistake, nobody in the content business is dumb. Content distribution changes only when content owners think they can switch, and still make as much, or more money than before.

So only after widespread licensing of content occurs will we be able to ascertain whether linear TV is necessarily more expensive than over the top alternatives. In many cases, some of us would be willing to bet, "saving money" will not be so easy.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, August 21, 2013

More Book Reading on Smart Phones than Tablets, Study Finds

People actually spend more time reading books on their phone overall compared to tablet usage, according to Readmill CEO and cofounder Henrik Berggren.

Smart phones are dramatically ahead of tablets when it comes to time spent reading books, according to a new study which tracks usage of the one billion smart devices now active in the world.

According to mobile app researcher Flurry, almost 90 percent of time spent reading books on these devices is done using smartphones.

Smart phones are dramatically ahead of tablets when it comes to time spent reading books, according to a new study which tracks usage of the one billion smart devices now active in the world.

According to mobile app researcher Flurry, almost 90 percent of time spent reading books on these devices is done using smartphones.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

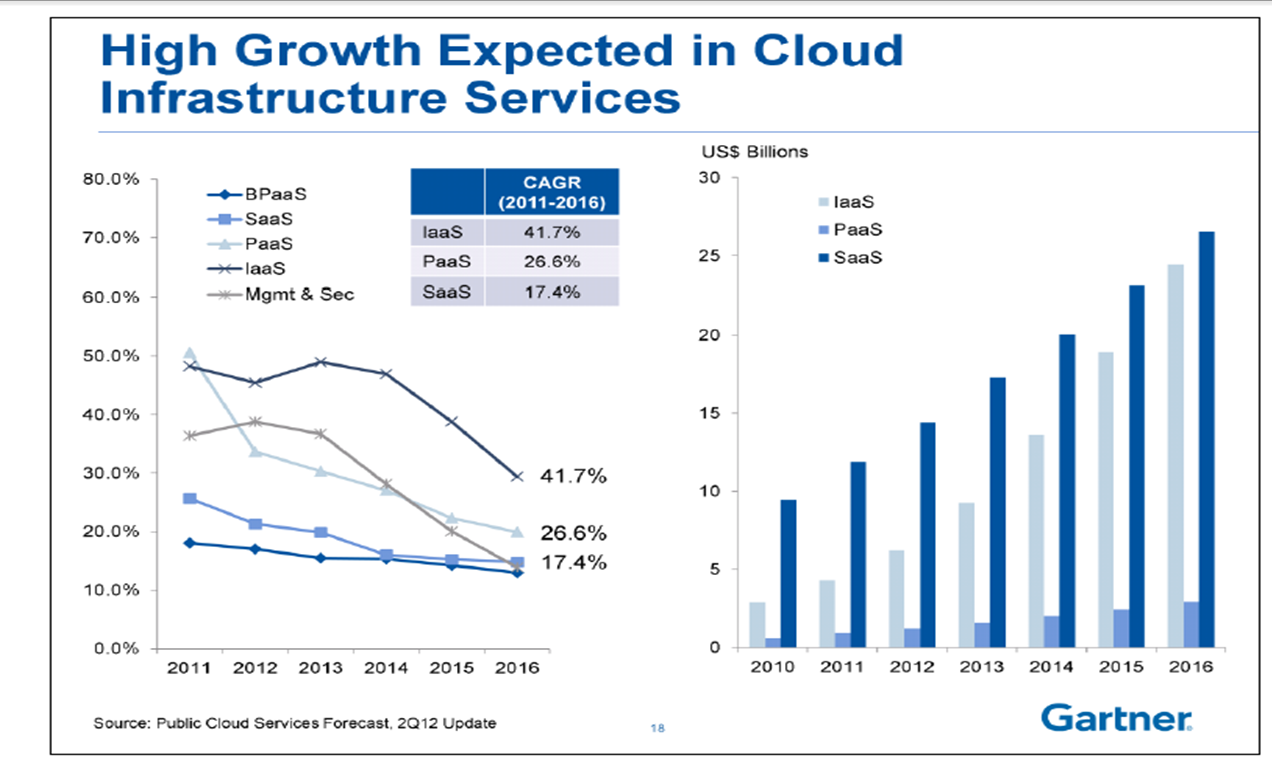

Amazon is 5X Bigger Than All Other Cloud Vendors Combined

AWS is simply dominant, at the moment, in cloud computing, you might conclude from a Gartner analysis that shows Amazon's AWS is five times bigger, in terms of the utilized compute capacity, of the other 14 cloud providers Gartner looked at.

AWS is simply dominant, at the moment, in cloud computing, you might conclude from a Gartner analysis that shows Amazon's AWS is five times bigger, in terms of the utilized compute capacity, of the other 14 cloud providers Gartner looked at. Telcos and telco-related entities probably still will be found most often in the infrastructure as a service part of the business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Czech 4G Auctions Coming in November 2013

The Czech telecoms regulator has restarted the country’s 4G spectrum auction process, after a halt because of concern about excessive prices. The previous licensing process was cancelled when the bid amounts massively exceeded the reserve prices.

The CTU concluded that if the licensees had to pay such high prices, they would have less capital available to actually build out the networks, and furthermore would be under pressure to keep prices high.

The spectrum auction will begin by mid-November after a previous attempted sale was aborted in March.

As has been the pattern elsewhere, regulators indicate their belief that a minimum of four national suppliers are necessary.

The CTU intends to reserve a large block of spectrum for a potential newcomer to the market, which already includes Telefonica, T-Mobile and Vodafone.

The three incumbents also are worried that the new entrant might be able to acquire spectrum at a discount. But it might be reasonable to assume that the fourth entrant will have a tough time competing against the three incumbents. In most Eastern and Central European markets, the three top providers have substantial market share.

In Hungary, Vodafone, the smallest of the three mobile providers, has 23 percent share. T-Mobile, the leader, has 46 percent. Telenor has 31 percent share.

In Croatia, T-Mobile has a roughly equivalent market share, while VIPnet has almost that much share. The point is simply that the established providers are entrenched. But most mobile markets are concentrated.

Whether, over the long term, that can change is the question. Many would argue the capital intensity and maturation of mobile markets makes the prospects for new disruptors difficult.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...