The best strategy in mobile device or computing device markets tends to change over time, some would argue. In a brand new market, it often makes sense to bundle the experience elements (integrate vertically) to reduce adoption barriers.

You might point to AOL's success, early in the consumer Internet access market, or Apple's historic focus on integrating experience elements for personal computing.

Later, when customers and users are well acquainted with a product, that approach can backfire, and a horizontal, unbundled, or "open" approach often can work better.

And that is the issue both Apple and Microsoft are grappling with, at some level. Some would argue Microsoft is about to pursue a vertical approach in mobile, where it historically has taken a horizontal approach in PCs.

And Apple continues to act consistently with its vertical approach, though many argue it should at least deviate somewhat from its "premium pricing" approach, as it did with the iPod product line.

But some might argue that a horizontal approach is better in a mobile device market that increasingly is well understood and mature. When consumers are comfortable with a technology product, the importance of a unified, consistent experience (provided by a vertical approach) arguably is less important.

Google, by way of contrast, has some "vertical" experiements (Nexus smart phone), but mostly operates horizontally, trying to be relevant on every platform.

Google wants to offer an integrated experience, but doesn't worry so much about "absolute best" experience on every device or platform, all the time. Google wants useful experience on every platform, all the time, and "best" experience on some devices, some of the time.

If Microsoft and Apple are wrong, time will tell. Cross-platform performance, some would argue, now is becoming strategic. Microsoft will pursue that some of the time, Apple some of the time, but neither has a cross-platform strategy all of the time.

For that matter, Google does not have a horizontal approach all of the time, either. But most of what Google offers intentionally is cross platform and horizontal. The vertical efforts are mostly demonstration projects intended to illustrate best of breed use of the platform.

Tuesday, September 17, 2013

In Different Ways, Microsoft and Apple Both Bank on Having the Right Strategy

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Revenue Role Reversal for Fixed, Mobile Networks?

In many ways, mobile service providers might hope Western Europe does not represent the future of the global business. In some ways, fixed network operators might hope Western Europe is a model for the future.

The reason is that fixed network revenue sources seem to be growing, as a percentage of total industry revenues, compared to mobile revenue sources, which seem to be shrinking, as a percentage of total industry revenues.

That doesn’t necessarily mean fixed network revenue is growing; it simply is shrinking more slowly than mobile revenues.

It appears mobile is poised for more serious revenue declines than fixed services. “A key factor is mobile's dependence on legacy non-data services compared with fixed-line or cable,” Analysys Mason says.

Already, about 67 percent of fixed operator revenue (excluding content) in Western Europe came from data in 2012.

In fact, though it will strike many as odd, the Great Recession and continuing economic sluggishness in Europe has produced evidence that European consumers consider their fixed service more essential than their mobile services, something many would assumed would operate in the reverse--with mobile services deemed more important than fixed.

Fixed service revenue seems to have been more stable than mobile revenues. In fact, fixed-line bundles have the best take-up in some of the more economically challenged countries, Analysys Mason notes.

Perhaps the primary reason for that fixed network preference is the value-price relationship, compared to the value-price relationship for mobile Internet access.

Also, with growing availability of Wi-Fi access in public and outside the home areas, it is easier to use “Wi-Fi only” or “Wi-Fi mostly” as the Internet access medium.

Oddly enough, after a long period where global growth was driven by mobile services, there now appears to be an opportunity for at least some new growth in the fixed network space based on providing services to mobile users.

Mobile data traffic increasingly is used at locations where fixed operators can supply most customer needs at lower cost and price. The reason is that most consumed data occurs when people are not “out and about,” but at stationary locations, most commonly the home or office.

Though a decade ago the notion that Wi-Fi hotspot networks could be a substitute for mobile access proved incorrect, some believer there could well be a different business terrain over the next several years.

Potentially, fixed broadband providers could cooperate with public Wi-Fi providers, or use owned assets, to create Wi-Fi access that is a reasonably useful primary Internet access method for some customers.

To counter that threat, mobile operators are adding their own public Wi-Fi networks, in part to offload traffic from the mobile network and in part to provide data services at lower cost.

The important potential new development is the reversal of “growth” prospects for mobile and fixed networks. Or, as some analysts suggest, which segment will decline less.

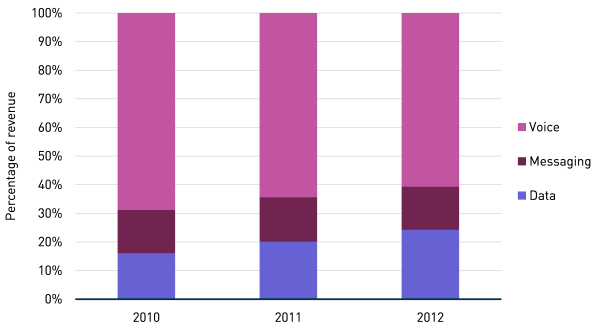

Mobile Service Provider Revenue Sources

Fixed Network Service Provider Revenues

Perhaps significantly, mobile spending is viewed as more discretionary than fixed network spending, by analysts at Analysys Mason.

Recent results from larger operators in Europe already show faster decline in mobile retail revenue than in fixed, and Analysys Mason forecasts that mobile will represent a declining share of total operator retail telecoms revenue during the next five years.

Spain might provide an example. Though overall service provider revenue is projected to decline over the next two years, fiber-based services on the fixed side and wholesale services or business-to-business mobile services are where revenue growth will be found, according to a new analysis by Pyramid Research.

The Spanish communications market generated €22.6bn ($29.0bn) in 2012, which represented an eight percent decline year-on-year.

Due to the prolonged economic recession, expected to last another two years in Spain, communications market service revenue will return to growth in 2015, up 2.3 percent a year.

Fiber to the home revenues will grow at a compound annual growth rate of 58 percent between 2013 and 2018, reaching $3.3bn in 2018,” says Pyramid Research Senior Analyst, Stela Bokun.

Mobile revenue growth will come from the enterprise and wholesale segments.

The key takeaway is that revenue growth will be tough, and that growth might be stronger (or declines less sharp) in the fixed network segment of the business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, September 16, 2013

Over the Top Video Entertainment Suffers Because of Cost Shifting by Participants

Any business ecosystem contains potential for conflict between participants, and the over the top video entertainment ecosystem is not exempt from those issues. In a loosely-coupled ecosystem, there frequently are opportunities to shift costs to other participants, or add complexity to functions provided by other participants.

At the moment, “such cost shifting has temporarily threatened, but not permanently damaged, the ability of over-the-top services to function acceptably,” according to Sandvine.

The quality of experience of an end-user for a given Internet-delivered application or content is affected by numerous choices made by many players through the value chain, including consumers.

End user devices (screen resolution, CPU performance, memory, application and operating system), the network inside consumer homes (wireless or wired, coverage, interference), the connection from their home to the access provider (RF noise, oversubscription ratios), the backbone of the access provider (oversubscription, latency), the transit providers, hosting services providers and original content providers make choices that can affect perceived end user quality.

Since a network’s capital cost is driven heavily by peak capacity, there is significant incentive for all parties to optimize and find efficiencies.

But it also means there is significant incentive to move the cost to another party, and there is ample opportunity to do so, says Sandvine.

With limited exceptions (peak and off-peak pricing, as well as using time-zones to trade-off transport distance versus server load), moving traffic in time is not an option because, with real-time applications, consumers decide when they want to be entertained.

What can be done is to minimize the total number of links between a source and a consumer, moving traffic to lower-cost links, arbitrage on pricing models or use of better video compression, Sandvine suggests.

The larger point is that disputes about how to allocate cost and revenue within the video entertainment ecosystem involve legitimate attempts by participants to maximize their own revenue and minimize their own cost.

That is why access providers so often complain that some app providers are imposing costs on access providers while reaping all the revenue themselves.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Growing Mobile Internet Access Has Implications for ISPs, Device Suppliers

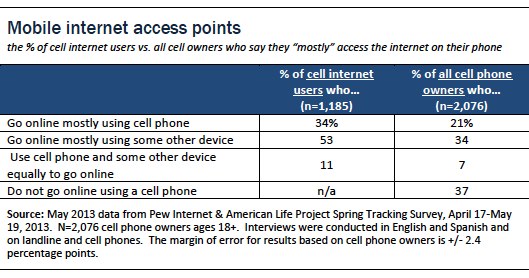

About 63 percent of mobile users appear to access the Internet from their phones. Of those, some 34 percent “mostly” use their phone to access the Internet, as opposed to other devices such as a desktop PC, notebook or tablet computer, according to the Pew Internet & American Life Project.

There are at least two areas in which there are potential implications for the Internet ecosystem and its suppliers, generally positive for mobile app and mobile ISP providers, as well as mobile device suppliers, and at least modestly unhelpful for suppliers of fixed ISP providers and PC suppliers.

To be sure, using a mobile device for Internet access might well entail use of a fixed connection with Wi-Fi capabilities, as well as the Wi-Fi capabilities of a smart phone. In that case, a preference for mobile device Internet access does not directly and fully represent use of mobile access as opposed to fixed access.

But the growing trend to use mobile devices for Internet apps and services also suggests a significant user population prefers mobile access, and believes a mobile device is a suitable substitute for a PC or notebook computer.

Also, there are some policy implications. The first implication is that, as always, consumers might choose not to buy some products that are made available to them. In other words, differences in purchasing behavior are not always or necessarily caused by “defects” of supply.

People make rational choices about products and services, and they might prefer mobile access to fixed access. Policymakers have to avoid regulating or legislating as though differences in consumer buying are necessarily "problems." They might just be a reflection of consumer choices.

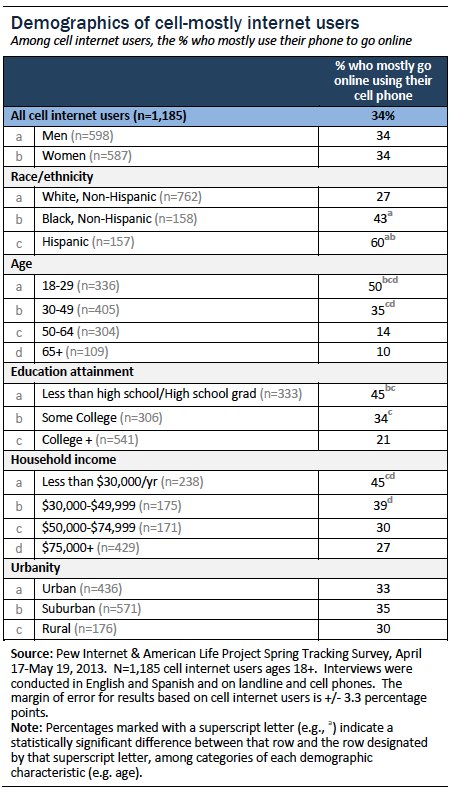

Such mobile-mostly Internet users account for 21 percent of the total mobile phone user population. Young adults, non-whites, and those with relatively low income and education levels are particularly likely to be mobile-mostly users.

That same trend is expected to emerge in many developing nations as well.

Some 53 percent of mobile Internet users say that they mostly go online from a device other than their mobile phone, while 11 percent say that they use both their phone and some other device or devices equally.

Since at least 2011, young adults, non-whites, the less educated, and the less affluent have said that they go online mostly using their cell phone at consistently high rates, Pew researchers say.

Among those who use their phone to go online, 60 percent of Hispanics and 43 percent of African-Americans are mobilel-mostly Internet users, compared with 27 percent of whites, say Pew researchers.

About 50 percent of mobile Internet users ages 18 to 29 mostly use their phone to go online.

Some 45 percent of mobile Internet users with a high school diploma or less mostly use their phone to go online, compared with 21 percent of those with a college degree.

Similarly, 45 percent of mobile Internet users living in households with an annual income of less than $30,000 mostly use their phone to go online, compared with 27 percent of those living in households with an annual income of $75,000 or more.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Sprint Launches "One Up" Device Upgrade Program

One Up is Sprint's new device upgrade program, launching Sept. 20, 2013 and allowing Sprint customers to buy a new phone with no money down, paying for devices in installments over two years.

If a customer terminates service before all the installment payments are made, the customer pays the balance of the device cost the following month.

The move by Sprint means all four of the large national carriers offers such a program.

T-Mobile US calls its program "Jump." AT&T calls its program "Next," while Verizon has "Edge."

If a customer terminates service before all the installment payments are made, the customer pays the balance of the device cost the following month.

After a year, a customer can upgrade to a new phone by trading in the device.

The move by Sprint means all four of the large national carriers offers such a program.

T-Mobile US calls its program "Jump." AT&T calls its program "Next," while Verizon has "Edge."

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Are Apple and Nokia Mirror Images?

The Apple strategy for emerging markets is in some ways the mirror image of what Nokia did.

Where Nokia had enormous strength in the "affordable phone" segments of emerging markets,

Apple seems to eschew that segment, sticking with its "premium, high margin" positioning even as it tries to expand to some demographic segments (wealthier customers) of the Chinese and other markets.

Some argue Apple is going the same way with smart phones that it chose to go with PCs, allowing Android to capture market share, with Apple eventually being relegated to a niche role.

Others believe Apple will succeed. But that is the point, some might say. We are talking about a pricing strategy.

Those arguments essentially avoid the question that is at the heart of all debates about whether Apple can keep its magic without Steve Jobs. Here we are, talking about pricing strategy. We aren't talking about reinvention of whole markets.

That might come, some would say. Others might say it might not even come, but Apple will find its way forward, anyhow. Some of us cannot avoid the sense that Apple will revert to the mean.

Most of us would agree with a general rule that nobody is "irreplaceable." But some of us might agree there are exceptions to every rule. Steve Jobs was that exception.

Where Nokia had enormous strength in the "affordable phone" segments of emerging markets,

Apple seems to eschew that segment, sticking with its "premium, high margin" positioning even as it tries to expand to some demographic segments (wealthier customers) of the Chinese and other markets.

Some argue Apple is going the same way with smart phones that it chose to go with PCs, allowing Android to capture market share, with Apple eventually being relegated to a niche role.

Others believe Apple will succeed. But that is the point, some might say. We are talking about a pricing strategy.

Those arguments essentially avoid the question that is at the heart of all debates about whether Apple can keep its magic without Steve Jobs. Here we are, talking about pricing strategy. We aren't talking about reinvention of whole markets.

That might come, some would say. Others might say it might not even come, but Apple will find its way forward, anyhow. Some of us cannot avoid the sense that Apple will revert to the mean.

Most of us would agree with a general rule that nobody is "irreplaceable." But some of us might agree there are exceptions to every rule. Steve Jobs was that exception.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, September 14, 2013

Expected Europe Consolidation Wave Causes EE to Rethink Sales

In anticipation of an expected major consolidation wave in Europe, carriers have to make decisions about whether they are buyers or sellers. In some cases, planned asset sales have been put on hold.

That is true for U.K.'s EE, which faces likely entry by AT&T into the $313 billion market, plus a Liberty Global-owned Virgin Media and a Vodafone with lots of new capital to deploy.

Deutsche Telekom and Orange of France apparently have slowed an effort to sell their 50-50 U.K. wireless venture known as EE.

In part, that is because of an expectation that the competitive situation could change in a major way, and soon, causing firms to rethink their strategies. Keeping EE intact might be useful for Orange and Deutsche Telekom in case they need to go on a buying spree of their own.

There are clear signs of change. America Movil wants to buy KPN. Vodafone is said to be eyeing Fastweb in Italy. There is speculation that AT&T might try to buy all of Vodafone when the Verizon transaction is completed.

Vodafone is said to be weighing a purchase of Liberty Global, which only recently swallowed Virgin Media.

Telefonica is buying E-Plus in Germany.

The point is that major carriers might soon find themselves in an "eat” or “be eaten” situation.

AT&T could pay about 80 billion pounds ($124 billion) for what’s left of Vodafone, according to Robin Bienenstock, an analyst at Sanford C. Bernstein, basing her estimate on a valuation of six times earnings before interest, tax, depreciation and amortization.

AT&T has examined takeover candidates including Vodafone, U.K. mobile carrier EE (a joint venture between Deutsche Telekom and Orange), as well as parts of Spain’s Telefonica.

That might strike some as odd, given the declining amount of revenue being earned by European mobile service providers. But AT&T seems to be thinking, as does SoftBank’s Sprint, about ways to boost revenue by emphasizing fourth generation Long Term Evolution services.

Whether Vodafone is a buyer or seller, a huge rearrangement of assets now is conceivable, essentially forcing all the major players to weigh moves of their own.

The upshot could be an accelerated transformation of Europe's troubled telecom industry.

Across the European Union, there are far more than 100 mobile and fixed-line operators, owned by a jumble of more than 40 groups, according to consulting firm IDATE. That compares with just four big mobile operators in the U.S., where the cable-television and broadband business is consolidating, too. As a result, revenue and profit at many European telecoms has been falling in a stagnant economy.

The biggest turning point in the European landscape has been Telefónica SA's agreement this summer to buy the German mobile unit of Dutch telecom Royal KPN NV in a €8.55 billion ($11.4 billion) deal.

"This is the starting gun ," said Robin Bienenstock, an analyst for Bernstein Research. "The chessboard is going to reform really, really rapidly." The potential mergers could make mobile service provider operations bigger, wed fixed line networks and mobile networks and reduce the number of leading contestants in many markets.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...