A sure sign there is weak device demand for Surface. But the growing prevalence of such programs sponsored by mobile service providers and major retailers suggests demand is a bit of a problem for many retailers.

http://feedly.com/k/16c5rT0

Thursday, September 19, 2013

Microsoft Will Buy Your Old Tablets and Smartphones

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

"Mobile Mostly" Content Consumption Trend Grows

With the caveat that what people mean by “mobile” can vary, people in the U.S. market seem to be spending more time consuming content, where time spent with other forms of media is flat. If tablets are included in the “mobile” device category, the fact that 2013 tablet shipments have grown 83 percent, while PC shipments dropped 13 percent, is going to make a difference.

With the caveat that what people mean by “mobile” can vary, people in the U.S. market seem to be spending more time consuming content, where time spent with other forms of media is flat. If tablets are included in the “mobile” device category, the fact that 2013 tablet shipments have grown 83 percent, while PC shipments dropped 13 percent, is going to make a difference.

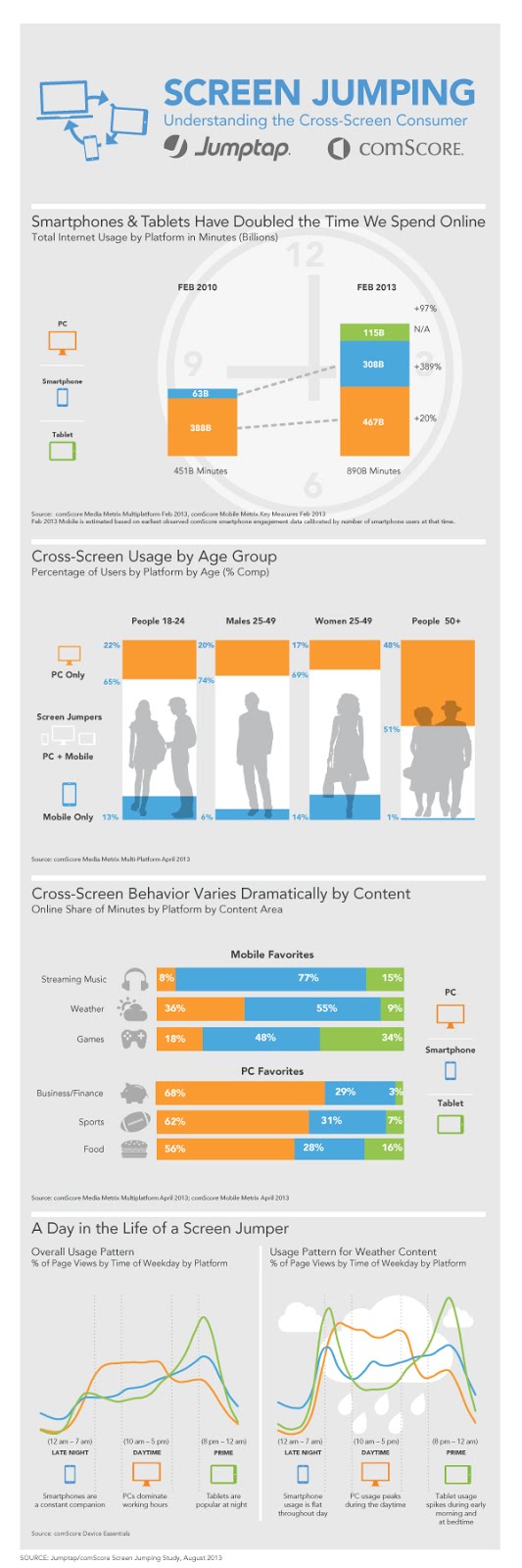

Mobile was the only media type to grow in total U.S. consumer minutes spent per day from 2010 to 2012, according to Business Insider.

Mobile content consumption clearly has grown over the last two years, with time spent using mobile devices for activities such as Internet and app use, gaming, music and other content more than doubling over the past two years.

In 2013, the amount of time U.S. consumers spend using mobile devices—excluding talk time—will grow 51.9 percent to an average 82 minutes per day, up from just 34 minutes in 2010, according to eMarketer.

Users spent an average of 93 minutes a day on the top mobile activities in the first quarter of 2013, compared to 77 minutes in the same quarter of 2012. That represents growth of about 20 percent a year.

The average consumer spends 40 minutes of their day playing a game on an app and 30 minutes using social media. Watching videos seems to occupy about 10 minutes of time each day.

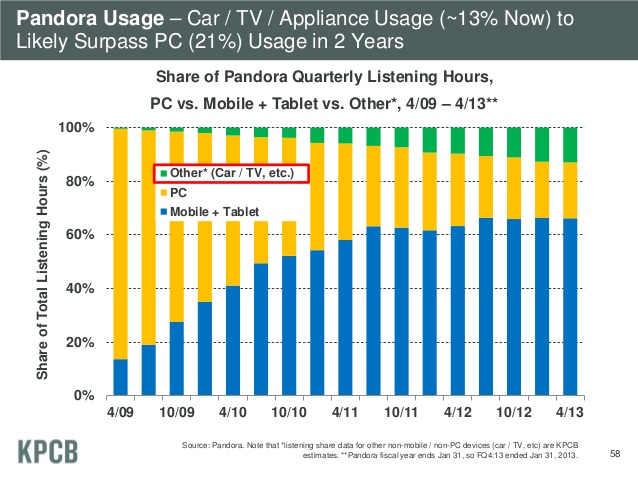

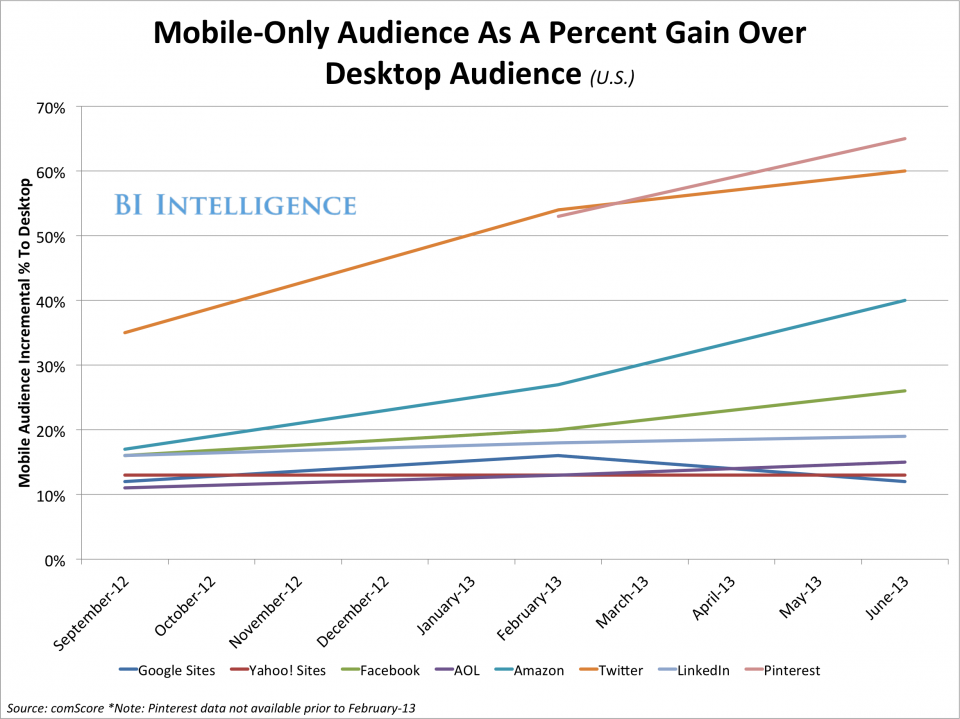

And some content sites are seeing extremely-high rates of growth for “mobile-only” usage. Pinterest, for example, seems to see 40 percent of users accessing content only from a mobile. Pandora, likewise, seems mostly used on mobile devices.

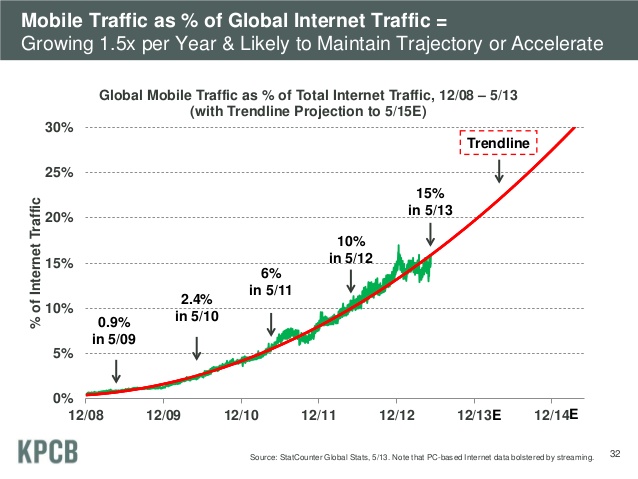

Those trends match the overall growth of mobile Internet consumption, which is growing at faster rates every year since 2008.

Those trends match the overall growth of mobile Internet consumption, which is growing at faster rates every year since 2008. Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Movie Revenue Model is Breaking

Sometimes the decline of a business model is historically inevitable even before the peak of revenues for the model.

Sometimes the decline of a business model is historically inevitable even before the peak of revenues for the model.

Voice revenues for the U.S. telecom business peaked, historically, about 2000. Skype was launched in 2003. The Telecommunications Act of 1996, the biggest change in communications regulation in 60 years, occurred just before the Internet explosion.

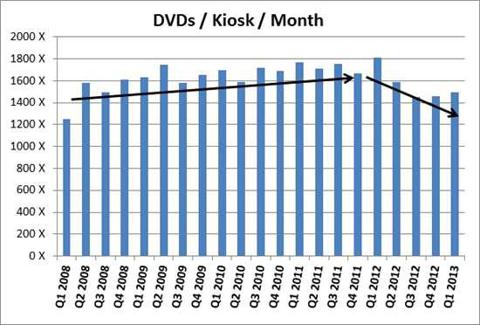

DVD purchases and rentals likewise hit an inflection point about 2000. By about 2010, even Netflix was predicting the decline of the model.

Some think the movie business is headed for a huge change as well, according to Adam Leipzig Adam Leipzig, CEO of Entertainment Media Partners.

“Studios are incredibly profitable now, and studios will continue to be highly profitable for the next three to four years, largely because they have reduced the number of movies they make, and also because they are being much more conservative in the way they manage their finances,” said Leipzig. “In the future though, five or six years down the road, this cycle will come to an end.”

“The studio profitability will go down,” he argues. And content production will change. “I’d argue that the best writing and the best character development is generally happening on Web or TV series. I would include shows from Netflix, as well as cable networks.”

There is a reason. “Studio movies are big economic plays; most summer movies cost $200 million to make, and another $200 million to market,” says Leipzig.

So there is a tendency to “play it safe.” That tends to mean studios want franchises, and that means sequels. The value of a franchise is that it is easier to market. People already know what to expect from a particular movie that is a franchise.

Filmmaker Steven Spielberg says it's becoming harder and harder for even brand-name filmmakers to get their projects into movie theaters.

“The business model within film is broken,” says Amir Malin of Qualia Capital, a private-equity firm.

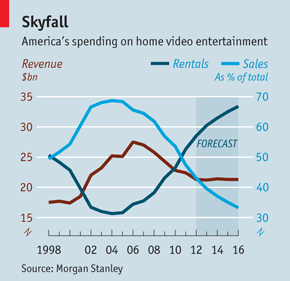

Between 2007 and 2011, pre-tax profits of the five studios controlled by large media conglomerates (Disney, Universal, Paramount, Twentieth Century Fox and Warner Bros) fell by around 40 percent, says Benjamin Swinburne of Morgan Stanley.

Between 2007 and 2011, pre-tax profits of the five studios controlled by large media conglomerates (Disney, Universal, Paramount, Twentieth Century Fox and Warner Bros) fell by around 40 percent, says Benjamin Swinburne of Morgan Stanley.

Swinburne predicts the studios account for less than 10 percent of their parent companies’ profits today, and by 2020 their share will decline to only around five percent.

Some argue consumers are shifting towards in-home consumption, and away from out of home consumption.

That is true, but even in-home consumption spending, in the U.S. market is flat, and down from a 2006 peak.

One might argue those trends augur well for independent producers and new types of outlets. One might also argue that the worsening economics of traditional studio-based movie making will shift attention and spending towards new methods.

That should favor outlets such as Netflix, at least some TV networks and independent producers. If these observers are correct, content innovation already is shifting away from the major studies and towards television-based networks and producers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Apple Sticks to Strategy: No "Junk"

Apple long has had a "premium product" strategy, even if it occasionally has produced lower-cost versions of some products, such as the iPod. But the philosophy of "no junk" remains the watchword at Apple, according to CEO Tim Cook.

Apple long has had a "premium product" strategy, even if it occasionally has produced lower-cost versions of some products, such as the iPod. But the philosophy of "no junk" remains the watchword at Apple, according to CEO Tim Cook.Does that mean Apple never will create a lower-cost iPhone? That might not be the relevant question. The bigger question is whether Apple ever will try to make devices at price points the Chinese mass market will buy. The answer to that seems an emphatic "no."

For better or worse, Apple simply does not presently see any reason to deviate from its strategy, and is willing to lose the smart phone operating system or device market share battles.

Apple is banking on the smart phone market being different than the old PC market, where Apple never escaped a niche. If Apple is correct, the smart phone market will eventually shape up for Apple as being between the pattern of PCs and MP3 players.

Though it was a niche supplier in the PC market, and the dominant provider in the MP3 market, Apple's smart phone business will be somewhere in between. Apple won't dominate in terms of share, but Apple will be relevant.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

New Opposition to EC "Connected Continent" Plan

Virtually nothing in the realm of communications policy is without controversy. So it is that an association of national European regulators has expressed “concern” about the “rush” to get new regulations through the European legislature.

The Body of European Regulators for Electronic Communications (BEREC) says it is concerned that the proposed regulation is being rushed through the European legislature “without proper explanation and full exploration of its potential consequences, given that the proposals represent a shift away from the current approach (based on pro-competitive regulation) towards one that favors market consolidation.”

BEREC also argues the proposed European Union proposals to streamline regulation across the EU will increase risk, undermine national authority and reduce the likelihood of increased investment in next generation network facilities.

To be sure, controversy is normal whenever major changes in telecom regulation are proposed.

Service providers can be expected to object to the eventual end of roaming fees, provisions that will take revenue and profit out of international calling. Regulators might not support more centralization of spectrum policies and regulatory authority.

The “Connected Continent” proposal will upset some policy advocates who will not be pleased with the approach to network neutrality (allowing creation of managed services).

And many will continue to wonder where and how the funds to invest in next generation infrastructure will be found.

The “Connected Continent” plan, created by Vice President for the European Commission Neelie Kroes, might actually depress European service provider investment in next generation infrastructure, according to Strand Consult.

The main problem, perhaps, is that the proposal continues to favor “competition” at the expense of “investment.”

The proposal “will create price wars between operators, which will deliver lower prices for consumers in the short term, but remove incentives for operators to invest long term,” argues John Strand, Strand Consult principal.

BEREC says it also is concerned that the proposals represent a substantial shift in the balance of power between the Commission, member states and national regulatory authorities,

centralizing authority at the EC.

“These proposals risk undermining the ability of national regulators, whether acting individually or collectively, to take appropriate and proportionate regulatory action in all the relevant markets,” BEREC maintains.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

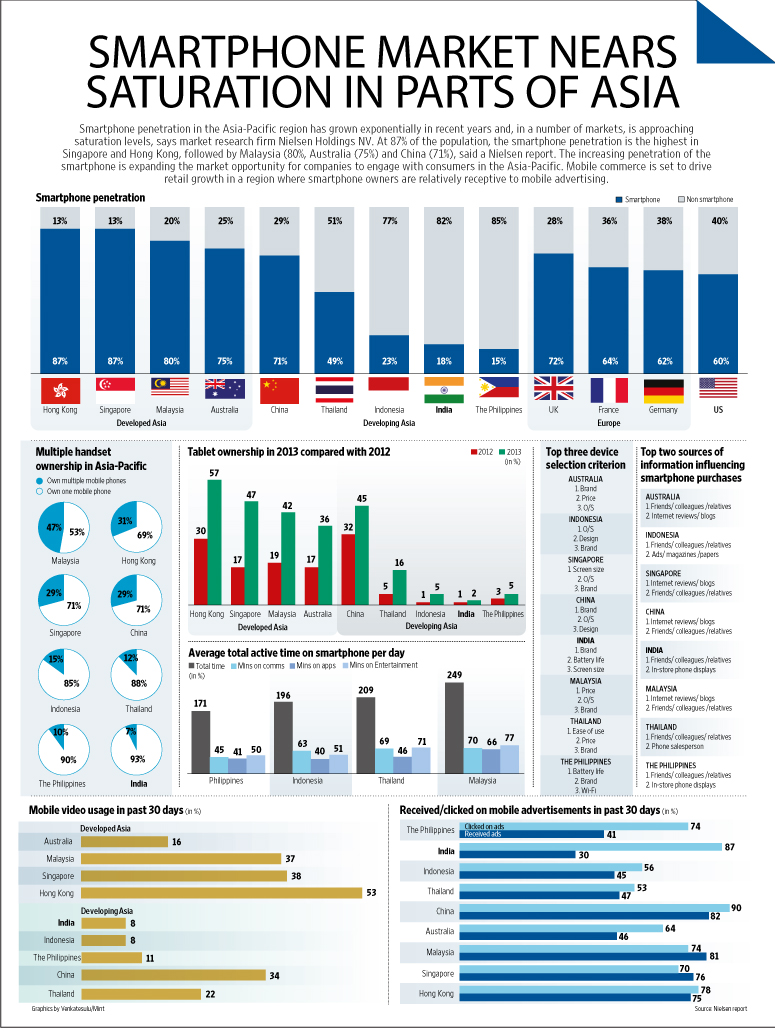

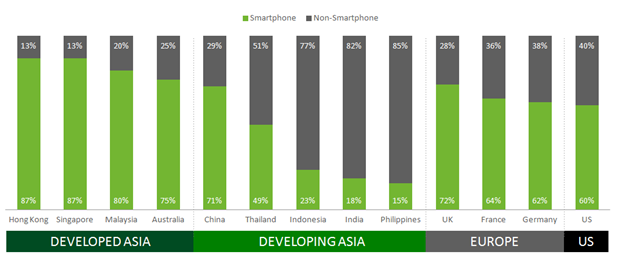

Smart Phone, Tablet Adoption in Asia is Study in Contrasts

Saturation and unmet need both are parts of the smart phone adoption story in Asia. On one hand, 87 percent adoption in in Singapore and Hong Kong, followed by Malaysia (80 percent), Australia (75 percent) and China (71 percent), shows some markets are nearing saturation.

On the other hand, smart phone adoption in the Philippines stands at 15 percent. In India penetration is 18 percent, while in Indonesia penetration is 23 percent, according to Nielsen.

In Southeast Asia, smart phone owners spent on average more than three hours per

day on their smart phones in June 2013, with activities such as chat apps, social networking and entertainment activities like games and multimedia driving the highest levels of engagement, Nielsen says.

Smartphone penetration, Asia, United States, Western Europe

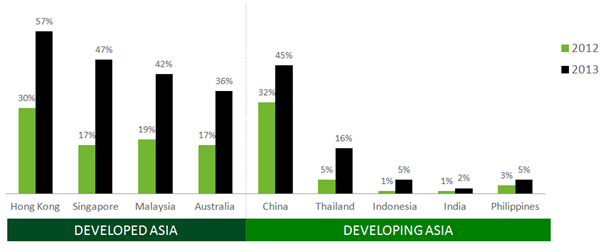

Tablet Penetration, Asia

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What is the Revenue Model for Mobile Apps?

Every Internet or mobile app, operating system or browser, communications or entertainment service available to users without charge has to find a viable business model. For more than a decade, at a high level, the implicit hope, or explicit expectation, was that “advertising” would be the ultimate revenue model.

That implies high end user scale, something it is obvious most apps will not be able to attain. Over the past half decade, though, “commerce” and “transactions” have started to get more traction as a revenue model, and mobile apps are no exception.

Though initially many hoped or expected that apps would create a direct app sales revenue model, that is only partly true. Free apps will account for 91 percent of total mobile app store downloads in 2013, according to Gartner.

"Free apps currently account for about 60 percent and 80 percent of the total available apps in Apple's App Store and Google Play, respectively," said Brian Blau, research director at Gartner.

So what is the revenue model for the 91 percent of “free” apps? In a growing percentage of cases, revenue is generated by “inside the app purchases.”

Gartner estimates that in-app purchases will account for 48 percent of app store revenue by 2017, up from 11 percent in 2012 and 17 percent in 2013.

In other words, mobile apps will be, in most cases, the enabler for a revenue stream (selling things inside the app), not a direct revenue generator.

Mobile app stores will see annual downloads reach 102 billion in 2013, up from 64 billion in 2012, according to Gartner researchers, with total mobile app store revenue in 2013 will reach $26 billion, up from $18 billion in 2012.

As with most other parts of the Internet ecosystem, leadership is, and will be, concentrated. "iOS and Android app stores combined are forecast to account for 90 percent of global downloads in 2017,” said Blau.

Over time, it also is likely that users will stabilize their usage of apps that have the highest value, leading to a lower rate of new app downloads, though the trend might slow only gradually.

Average monthly downloads by iOS users will decline from 4.9 in 2013 to 3.9 in 2017, while average monthly downloads by Android device users will decline from 6.2 in 2013 to 5.8 in 2017, Gartner predicts, as users develop strong preferences for some apps.

What isn’t so clear yet is the relative importance of tangible goods and services, compared to digital content goods, that will be purchased inside mobile apps. What is clear is that the business model for “free” apps will not be driven mostly by advertising, as might be the case for some Internet apps.

Mobile App Store Downloads, Worldwide, 2010-2016 (Millions of Downloads)

2012

|

2013

|

2014

|

2014

|

2016

|

2017

| |

Free Downloads

|

57,331

|

82,876

|

127,704

|

167,054

|

211,313

|

253,914

|

Paid-for Downloads

|

6,654

|

9,186

|

11,105

|

12,574

|

13,488

|

14,778

|

Total Downloads

|

63,985

|

102,062

|

138,809

|

179,628

|

224,801

|

268,692

|

Free Downloads %

|

89.6

|

91.0

|

92.0

|

93.0

|

94.0

|

94.5

|

Source: Gartner (September 2013)

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...