Telefonica will boost its stake in Telco, the holding company that controls Telecom Italia, to an initial 65 percent with an option to bring the stake to around 70 percent, according to Reuters.

Telefonica already own 46 percent of Telco, representing in turn about 10 percent of Telecom Italia shares. Telefonica says It will boost its stake in the Telecom Italia to nearly 16 percent.

Telefonica is set to acquire its additional shares from the other Telco shareholders, including Italian banks Mediobanca, Intesa Sanpaolo, and insurer Generali.

The move might well be viewed as part of a coming merger wave in the European telecom market.

Tuesday, September 24, 2013

Telefonica to Own Most of Telecom Italia

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

AT&T, Fon Sign Roaming Deal

AT&T and Fon, the Spain-based network of user-contributed Wi-Fi hotspots, now have a Wi-Fi network roaming agreement that allows users of Fon and some AT&T customers Wi-Fi access privileges on both networks.

AT&T customers can download the WiFi International App will gain access to hundreds of thousands of FonSpots internationally.

The AT&T Wi-Fi International App, which is available on iPhone, iPad and Android devices, lets AT&T customers on either the 300 MB ($60 a month) or 800MB ($120 a month) “AT&T Data Global Add-On” package access up to 1 GB of Wi-Fi each month at no additional charge.

Fon members will gain access to AT&T’s Wi-Fi network, including more than 30,000 hotspots at restaurants, hotels, bookstores and retailers throughout the United States.

An observer might be tempted to guess that Fon users will derive more value from the agreement than will AT&T users, for a couple of reasons, beginning with charging models.

Foneros have a couple of ways to gain access to other Fon hotspots, but the cost is free to low. That will not be the case for AT&T customers, who will spend at least $60 a month, and up to $120 a month, to gain access to Fon hotspots in countries where Fon operates.

Those partners include Belgacom (Belgium), BT (UK), Deutsche Telekom (Germany), Hrvatski Telekom (Croatia), KPN (Netherlands), MTC (Russia), Netia (Poland), Oi (Brazil), SFR (France), Softbank (Japan) and ZON (Portugal).

Still, the roaming deal is likely to be most valuable to a rather small but important subset of AT&T users, namely those who travel to Fon-served areas, especially business users.

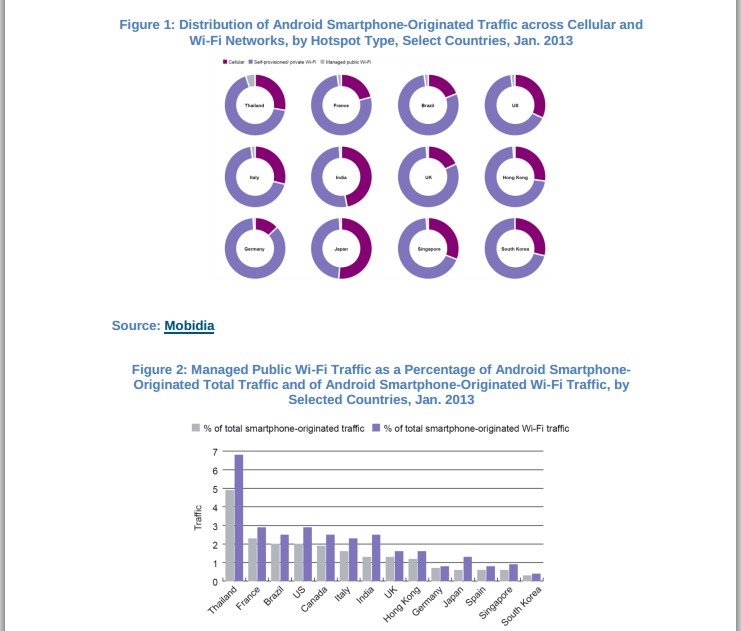

The important nuance about Wi-Fi hotspot use is that the overwhelming percentage of smart phone Wi-Fi use happens on private hotspots, not public hotspots, even though, with very few exceptions, such as Japan, users in most developed countries consume well over 80 percent, and often over 90 percent, of their total mobile data on Wi-Fi networks.

According to researchers at Juniper Research, almost half of all mobile data traffic will be offloaded to Wi-Fi and other local networks in 2013.

The bigger question is how much "out and about" usage might be shifted to Wi-Fi.

NTT in Japan has tested the offload potential of dense Wi-Fi deployments and apparently has concluded that less than 25 percent of mobile data traffic can be offloaded to public Wi-Fi in the long term.

On the other hand, Mobidia already estimates a majority of total smart phone data usage occurs on Wi-Fi, for all of the top-four U.S. mobile operators, with AT&T having the largest percentage of Wi-Fi use, compared to mobile data.

So though Wi-Fi networks consistently accounted for well over 90 percent of the Wi-Fi traffic, according to Mobidia, perhaps three percent of that traffic used a public hotspot.

In other words, use of managed, public hotspots, as would be offered by Wi-Fi network providers (such as Fon) or mobile operators (such as AT&T), consistently accounts for very little traffic across all countries analyzed by Mobidia.

People make use of at-home and at-work connections, mostly. Even when traveling, it is likely most people will be using hotel or other residence-based Wi-Fi for the great bulk of their data consumption.

Still, the value of public hotspot access could be very high for some AT&T users.

The deal also illustrates the Wi-Fi revenue model and value, for a firm such as AT&T. Access to the Fon network requires that mobile users purchase an extra international data service costing $60 a month or $120 a month.

The use of the Fon hotspots provides value by allowing users to offload up to 1 Gb, each month they are roaming, but the revenue is driven by the need to buy the extra international roaming feature.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, September 23, 2013

Australia NBN Making Course Correction to Save $56 Billion

Australia appears to be making a switch of access topology for its planned National Broadband Network from “fiber to the home” to “fiber to the neighborhood.”

With a seven percent incremental rate of return, over a 30 year period, a reasonable observer might simply note that there is little room for error where it comes to the base assumptions.

It appears most of the Australian National Broadband Network company's board members have tendered their resignations, at the request of the Communications Ministry. NBN Company chairwoman Siobhan McKenna and all but one of her board colleagues have offered their resignations to the Communications Ministry.

The reason is that the new national government campaigned, in part, on a promise to get the network built faster, at far lower cost.

The change to a less fiber-intensive network is said to represent a final cost of A$20.4 billion (US$18.4 billion), well below the A$38 billion ($33.8 billion) originally stimated for the fiber to home plan, and far less than the $94 billion critics now say the former network would cost.

Some critics estimate that the Australian National Broadband Network (NBN) will cost A$94 billion dollars, not the A$44 billion its supporters have claimed. At least in part, that is because

The original business plan assumes wholesale revenue will start at $22 per month and then climb to $62 by 2020 or 2021 when the NBN is finished. That is growth of nine percent a year beyond inflation. Other major ISPs might say average prices for Internet access do not climb more than nine percent a year.

So critics say revenue projections are wildly overestimated.

Another assumption is that construction costs will average about $2400 per location. Critics say the actual cost will be closer to $3600. The cost and revenue assumptions also are contingent on completing the project on time, and so far the project has encountered significant delays.

The NBN Co. claims it already is connecting locations for $2200 to $2500. Critics say those are costs for the easiest builds, and will not reflect average cost as the more difficult locations are tackled.

Some supporters argue there will be a learning effect, driving costs down over time. But several contractors have pulled out of their deals with NBN Co. because they cannot do the installs for the prices NBN says it is paying.

NBN Co had expected to have 566,000 active users by June 2013. It managed to sign up just 33,600.

Some have argued the operating risk is high as well. Among the key assumptions of the fiber to home plan are that 30 year incremental rate of return will be seven percent (7.1 percent) on a capital investment of $35.9 billion through 2020, based on wholesale access rates between $20 and $27 a month.

The current forecast calls for about 44 percent take rates in 2015.

Revenues to 2021 are forecast at $23.1 billion, with operating expense expected to be

$26.4 billion.

The latest version of the original business plan does suggest that the actual direct financial return from a fiber to home access network, built on a continental scale, is relatively small, despite its societal and economic importance.

With a seven percent incremental rate of return, over a 30 year period, a reasonable observer might simply note that there is little room for error where it comes to the base assumptions.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Saturday, September 21, 2013

Rights to Supply TV Series to Support "Binge Viewing" is Part of Long-Term Video Trend

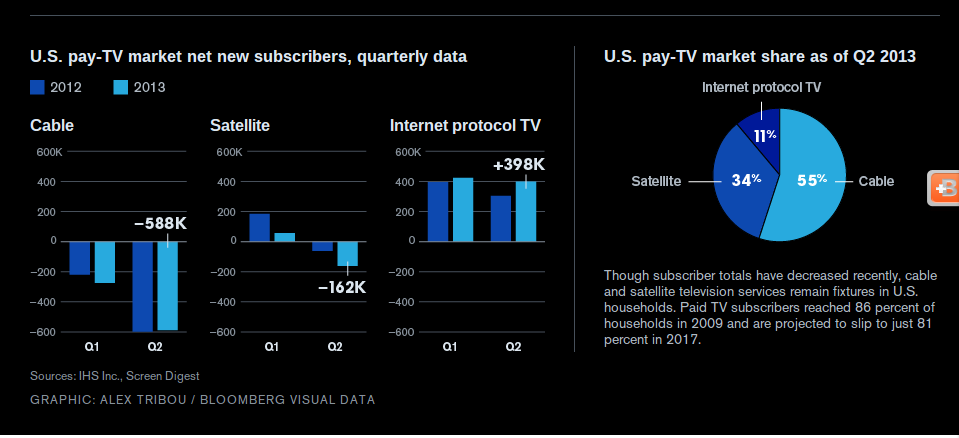

Video consumption has been moving steadily towards on-demand, non-real-time modes for several decades. One might be tempted to say it was the availability of video on demand that has driven the trend, but cable, satellite and telco pay per view and VOD usage rates are relatively low, and always have been, in comparison to other video products and revenue streams.

The U.S. PPV and VOD market is a low single digit billion size market, compared to a U.S. video subscription service (cable, satellite, telco) annual revenue stream in the neighborhood of $90 billion.

In fact, VCR, DVD and Blu-ray players drove the rise of on-demand viewing, using physical media, while Netflix and others are driving the shift to streaming.

The point is that the direction of video entertainment consumption is towards “on demand” modes. YouTube, Hulu, Amazon Prime, Netflix, mobile video, TV Everywhere, even “binge viewing” all are examples of that trend.

Almost by definition, those changing modes of consumption create the possibility that leading providers in the video entertainment business can change their shares of market.

To be sure, the historical record suggests new technology creates new modes of consumption, and consequently new revenue models, virtually always driven by changes in consumer demand.

In the near term, one additional change is consumer appetite for “binge viewing” of TV series content. Where in the past distributors have relied on the pull of a popular series to keep viewers coming back to a network, Netflix has pioneered the concept of binge viewing of multiple episodes at a time, or even a whole year’s worth of episodes over a weekend.

Until now, Comcast and other pay-TV providers have generally offered four or five episodes of a current show on a rolling basis, with an older episode dropping off the on-demand menu as a new one is added. Under the new arrangement, every episode will be available after it airs all season.

Now cable TV operators are trying to get rights to offer TV series content in ways that allow customers to binge view. That is viewed as a way to shift viewer attention and increase the value of a video subscription service, compared to Netflix. Netflix obviously would prefer to keep its exclusive in that regard.

Some content companies, such as 21st Century Fox and NBCUniversal, are more willing to give expanded on-demand rights to their cable, satellite and telco TV distributors. Others such as Walt Disney Co. and CBS Corp.are more reluctant to do so.

Because of the way content release windows are structured, on-demand services get content sooner than Netflix. So Netflix argues, reasonably enough, that TV series exposure on on-demand services will reduce the value and size of the audience when Netflix can show the episodes.

Such skirmishing over “when” one outlet can get access to fresh content has been, and will remain, a key weapon for distributors of every sort.

Content rights also play the key role in shaping competitive potential for some distributors with geographically-limited footprints, especially Verizon Communications. By definition, all fixed network video distributors require video franchises to operate, and hence are geographically bound.

But Verizon, among others, is seeking content rights that allow sales anywhere in the United States, a licensing mode that is quite helpful to well-heeled distributors who face significant geographic limitations.

That is an important dimension of the Verizon Communications effort to provide, for the first time, out-of-home access to live TV feeds. Verizon has not yet gotten such rights, but might someday be able to sell Internet-based video entertainment of the sort it now sells to FiOS TV customers within the geographic footprint of its fixed network.

We aren’t there yet, but Verizon is making progress, launching an upgraded version of its FiOS Mobile App that, for the first time, provides out-of-home access to live TV feeds, starting with nine channels: BBC America, BBC World News, EPIX, NFL Network (tablet only), HGTV, DIY, Tennis Channel, Food Network and Travel Channel.

The FiOS Mobile App also delivers select local channels depending on where they currently are in New York, New Jersey, Philadelphia, and Washington, DC.

Verizon’s browser-based FiOS TV Online service now offers 69 live TV channels that are accessible by authenticated customers in the home or on the go.

Verizon FiOS customers have been able to watch live television on their iPads, while connected to their in-home broadband access networks.

So far, no video service provider has permission from all programing networks to stream all standard fixed network service everywhere. Time Warner Cable, Comcast, DIsh, Cablevision, and DirectTV all offer some level of live content that can be watched outside of the home.

Beyond the implications for the way people consume TV services, the coming change will be that fixed network service providers will be able to sell that content to customers anywhere in the United States, so long as they have access to a suitable broadband connection.

That could have important implications for the addressable market available to Verizon, which has a relatively limited U.S. fixed network footprint. AT&T also would benefit, but AT&T has a bigger network footprint.

One reason video service market share for AT&T and Verizon has slowed, though the telcos continue to take market share from cable operators, is that they cannot offer service everywhere.

An out of market capability could accelerate market share gains by telcos.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, September 20, 2013

Will Telco Video Services Go Nationwide, as Mobile Services Have?

There is an important dimension of the Verizon Communications effort to provide, for the first time, out-of-home access to live TV feeds its FiOS customers have paid for as part of their TV services, that has nothing to do with streaming and linear video.

That new dimension is an ability by Verizon or other place-based service providers to escape the bounds of their local operating territories. In other words, Verizon might someday be able to sell Internet-based video entertainment of the sort it now sells to FiOS TV customers within the geographic footprint of its fixed network.

We aren’t there yet, but Verizon is making progress, launching an upgraded version of its FiOS Mobile App that, for the first time, provides out-of-home access to live TV feeds, starting with nine channels: BBC America, BBC World News, EPIX, NFL Network (tablet only), HGTV, DIY, Tennis Channel, Food Network and Travel Channel.

The FiOS Mobile App also delivers select local channels depending on where they currently are in New York, New Jersey, Philadelphia, and Washington, DC.

Verizon’s browser-based FiOS TV Online service now offers 69 live TV channels that are accessible by authenticated customers in the home or on the go.

Verizon FiOS customers have been able to watch live television on their iPads, while connected to their in-home broadband access networks.

So far, no video service provider has permission from all programing networks to stream all standard fixed network service everywhere. Time Warner Cable, Comcast, DIsh, Cablevision, and DirectTV all offer some level of live content that can be watched outside of the home.

Beyond the implications for the way people consume TV services, the coming change will be that fixed network service providers will be able to sell that content to customers anywhere in the United States, so long as they have access to a suitable broadband connection.

That could have important implications for the addressable market available to Verizon, which has a relatively limited U.S. fixed network footprint. AT&T also would benefit, but AT&T has a bigger network footprint.

One reason video service market share for AT&T and Verizon has slowed, though the telcos continue to take market share from cable operators, is that they cannot offer service everywhere.

An out of market capability could accelerate market share gains by telcos.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

How is Home Automation, Security Business Different from a Decade Ago?

What makes the home automation and home security business different from the business that existed a decade ago? The ability to use broadband, and therefore, video, as a part of the security system. What makes the business different from two decades ago?

What makes the home automation and home security business different from the business that existed a decade ago? The ability to use broadband, and therefore, video, as a part of the security system. What makes the business different from two decades ago?

The ability to use a smart phone to control settings, from nearly any location, using only the device in a pocket or purse.

And that explains the new interest being shown in the home security and home automation business by ISPs.

"Already 10 percent to 12 percent of broadband households in the U.K. and France own a home control solution where they can control a device such as a thermostat or security camera via a smart phone smart phone or PC," said Stuart Sikes, president, Parks Associates.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Declining Product Demand Looks Like at Colleges, Hotels

Declining product demand already has hit hotel revenue streams, in the form of vastly-lower telecom revenue from guests. Now it appears we are seeing similar declining demand for entertainment video subscriptions, in an important demographic.

It’s hard to ignore the lack of demand that has lead Northwestern University to get out of the business of providing a cable TV entertainment service on campus.

That would follow a general move away from providing in-room telephone service on college and university campuses with student housing that has been underway since the mid-2000s.

Some might say college students prefer to watch TV on devices other than TV screens. Others would say Netflix is the preferred choice for video entertainment, since paying for Internet access tends not be an issue, and access tends to be fast.

The big issue is whether college students are acquiring new habits that will persist after they have graduated. In fact, there already is evidence that earlier generations of students have indeed been less enthusiastic adopters of the subscription TV service habit when they have gotten into the workforce.

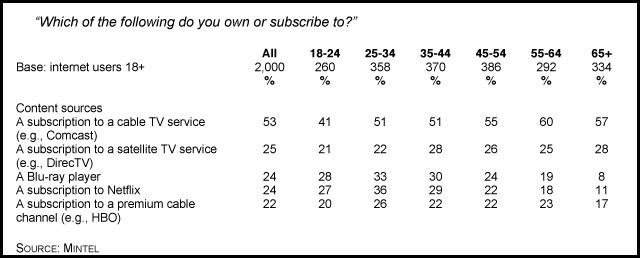

In fact, newly formed households have been buying subscription TV at lower rates than older consumers. While 3.2 million new U.S. households were set up since about 2010, the subscription TV industry (cable, satellite, telco TV) only added 250,000 subscriptions in that same period, according to SNL Kagan.

That is an issue for younger people overall, who seem to be losing their appetite for subscription TV. It has been a standard pattern for some time that older people subscriber at higher rates than younger people.

Some might attribute at least part of that to lower typical incomes for younger age cohorts, and that is a reasonable enough assumption. But evidence is growing that even households with no apparent inability to pay.

For starters, Millennials watch less traditional television than any other demographic, suggesting they find the product less engaging than older people might.

Some 13 percent of 18 to 34 year olds (8.6 million) who already have broadband service are committed to a broadband-only existence, with no plans to buy a subscription TV service.

In addition, many consumers who do buy service are at least considering dropping their entertainment video service (17.9 million 18-34s, as well as 32 million 18-49s).

Perhaps seven percent of potential churn candidates indicate they would consider keeping their TV subscriptions if offered programming streamed live and on demand, anywhere.

More significantly, 58 percent of broadband-only subscribers would consider subscribing to TV for a bundle of networks from their broadband provider, streamed live and on demand.

The study, sponsored by programming channel Pivot, was conducted by Miner & Co. Studio in association with Beagle Insight.

The point is that demand for subscription TV is on the wane, among younger consumers.

To be sure, colleges and universities already had discovered that selling telephone service no longer makes sense, given widespread, virtually ubiquitous use of mobile phones by college students.

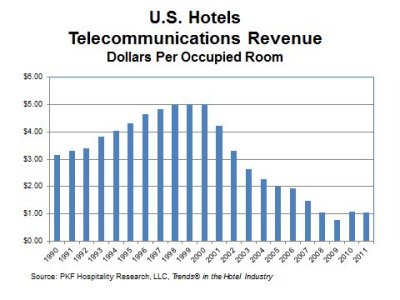

That mirrors similar trends for hotel-supplied telecom services, which also fell dramatically after 2000, which is very close to the peak year for fixed line usage in the U.S. market, as well.

According to PKF Hospitality Research, telecommunications revenue at the average U.S. hotel declined from a peak of $1,274 per available room (PAR) in 2000 to $269 PAR in 2011, a 79 percent decline.

During the 1990s, telecommunications revenues used to account for three percent of total hotel sales. In 2011, that number declined to just 0.6 percent of sales.

In fact, some would argue that telecommunications service in guest rooms now “costs” most hotels money. In 2011, for every dollar of telecommunications revenue earned, the average hotel spent $1.46. In other words, in-room telephone service now is an expense item, not a revenue generator.

Also, as U.S. communications service providers also have discovered, it now is Internet access that is driving revenues, not voice services. An uptick in telecommunications revenue at hotels surveyed by PKF Hospitality Research in 2011 and 2011 suggests Internet access now is lifting revenue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...