Intel Media has been trying to build a Web-based subscription TV service for several years, and originally had promised to launch late in 2013. But Intel seems not to have gotten traction with the content suppliers it would need to build a service analogous to cable TV.

Intel recently had said it was looking for partners, including Samsung, Amazon, Liberty Media, and Netflix, but a report suggests Intel Media has failed at that effort as well, and is exploring a sale of its assets to Verizon Communications, which already owns part of the Redbox Instant streaming service operated as a joint venture with Redbox.

Qualcomm earlier had launched a mobile video service called MediaFLO, but wound up closing the service and then selling the spectrum to AT&T after abandoning the effort.

MediaFLO did better than Intel, at least in terms of securing content rights. In the U.S. market, for example, MediaFLO offered a set of 14 basic channels:

- 2.FLO (6 am to 10 pm) — Original made-for-mobile reports and concerts

- Adult Swim (10 pm to 6 am)

- ABC Mobile

- CBS Mobile

- CNBC

- Comedy Central

- ESPN Mobile TV

- Fox Mobile

- Fox News Channel

- MTV Mobile

- MSNBC

- NBC 2Go — A mix of MSNBC, NBC, CNBC, and Bravo networks

- Disney Channel

- Nickelodeon

None of these failures is going to stop other entities from trying to create new streaming services. Sooner or later, a bigger crack than Netflix will appear in the dam.

Aereo, the local TV streaming service, launching in Denver on November 4, 2013, already serves nine U.S. markets. Another firm, FilmON, previously "Aerokiller," operates in Western U.S. states, primarily.

And Amazon, Apple and Google already offer video streaming content, if not perhaps on the scale of Netflix. And there is talk that Comcast might itself launch its own branded streaming service as well.

So far, no provider has been able to convince a critical mass of content owners to make their shows available to streaming services on the same basis as presently offered to cable TV, satellite TV and telco TV providers.

And that is to say nothing of new licensing models that might allow customized, individualized or a la carte purchase of single episodes, whole series or single channels.

Sooner or later, it will happen, though most assume it will take some time to reach that point.

It will likely take far greater disruption of the economics of today's subscription video revenues before content owners will be willing to start making changes that enable truly competitive streaming services. We aren't quite there, yet.

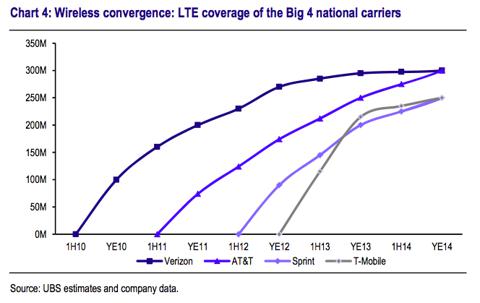

Sprint expects to have Long Term Evolution 4G network coverage of about 100 million pops, using the 2.5-GHz former Clearwire spectrum (120 MHz in most major U.S. markets) by the end of 2014. That probabnly is less coverage than some observers had expected.

Sprint expects to have Long Term Evolution 4G network coverage of about 100 million pops, using the 2.5-GHz former Clearwire spectrum (120 MHz in most major U.S. markets) by the end of 2014. That probabnly is less coverage than some observers had expected.